20%+ APY on Stablecoins, Morpho's Hidden Catalyst, and more...

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

In this letter, we bring you the best bottom-up analysis of onchain trends, along with top-down market analysis, helping you find top yield opportunities and position for trends before they happen

1. Stablecoin Flows, and stablecoin-specific flows

2. ETF and exchange flows

3. Stablecoin flows per chain

4. Perps and DEX Volumes Analysis

5. TVL gainers - for protocols above $100M

6. DeFi token price gainers & their catalysts

Key Takeaways

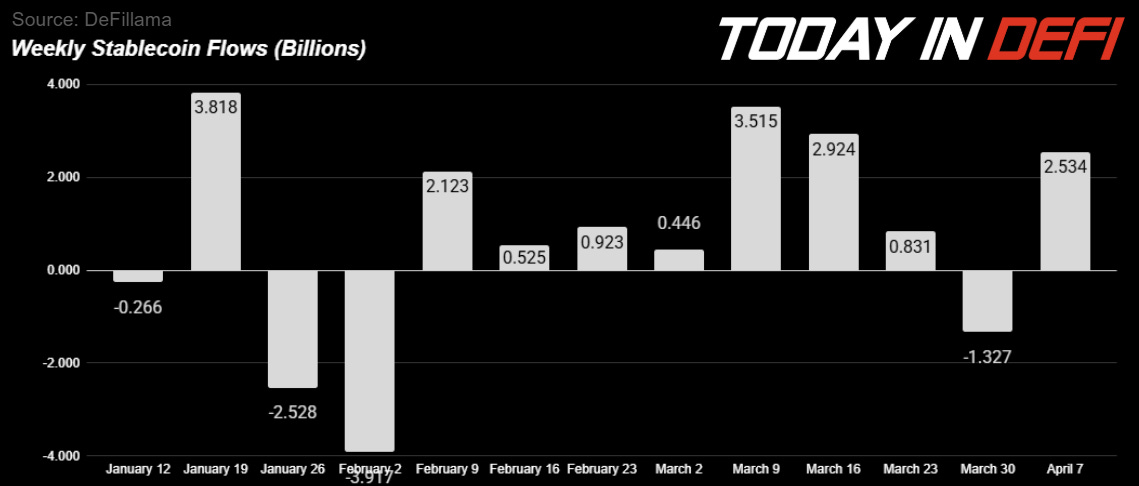

Stablecoin inflows hit +$2.534B (+0.8%)— the third largest weekly inflow since January. Last week’s dip was a pause. The staircase is still climbing.

Reservoir’s wsrUSD is offering up to 20% looping APY on Morpho (Monad). A CDP stablecoin that nearly doubled in TVL in one month — the yield infrastructure behind it is the reason why.

Ethereum leads on stablecoin inflows amongst all chains this week, boosted by low-risk RWA yields from protocols like Ondo, Grove, and Securitize, which have TVLs above $1b grew more than 15% in the past 7 days.

Facilitating growing ETF and institutional staking demand, boosted by regulatory clarity around crypto staking, benefited Liquid Collective, as the protocol grew $165M (23%) TVL last week.

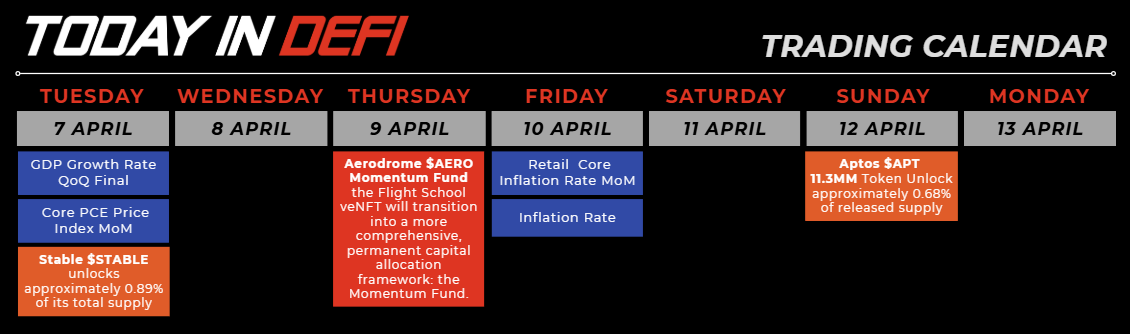

Trading Calendar 🗓️

The dominant driver wasn't crypto-native. Trump's ultimatum to Iran — threatening to strike infrastructure if no deal was reached by early April — pushed oil above $112 and triggered the kind of geopolitical risk-off that hits crypto fast and hard. BTC dipped toward the mid-$65k area before recovering as ceasefire talks entered the conversation.

The relief came late April 7 when a two-week ceasefire was announced — Iran agreed to reopen the strait, negotiations are set for Islamabad, and markets exhaled.

What To Watch This Week

Tue, Apr 7 — GDP Final + Core PCE. Two macro prints in one day. Core PCE is the one that matters — a higher number means rate cuts stay off the table, pressure on risk assets continues.

Tue, Apr 7 — $STABLE Unlock. 0.89% supply hit. Watch for early sell pressure.

Thu, Apr 9 — Aerodrome Momentum Fund. Flight School veNFT converts into a permanent capital allocation framework. Structural upgrade for AERO ahead of the VELO merger — the most important DeFi-native event of the week.

Fri, Apr 10 — CPI. The print that moves markets. Soft = Fed dovishness opens up. Hot = more of the same sideways pain. Everything this week points here.

Sun, Apr 12 — $APT Unlock. 11.3M tokens, 0.68% of supply. Already seeing -$97M stablecoin outflows this week — supply increase on top of capital leaving is a bad combination for APT holders.

1. Stablecoin Flows - Inflows are Back!

This week delivered +$2.534B (0.8%), the third-largest single weekly inflow in the entire dataset going back to January. Coming in the middle of a macro equity shock.

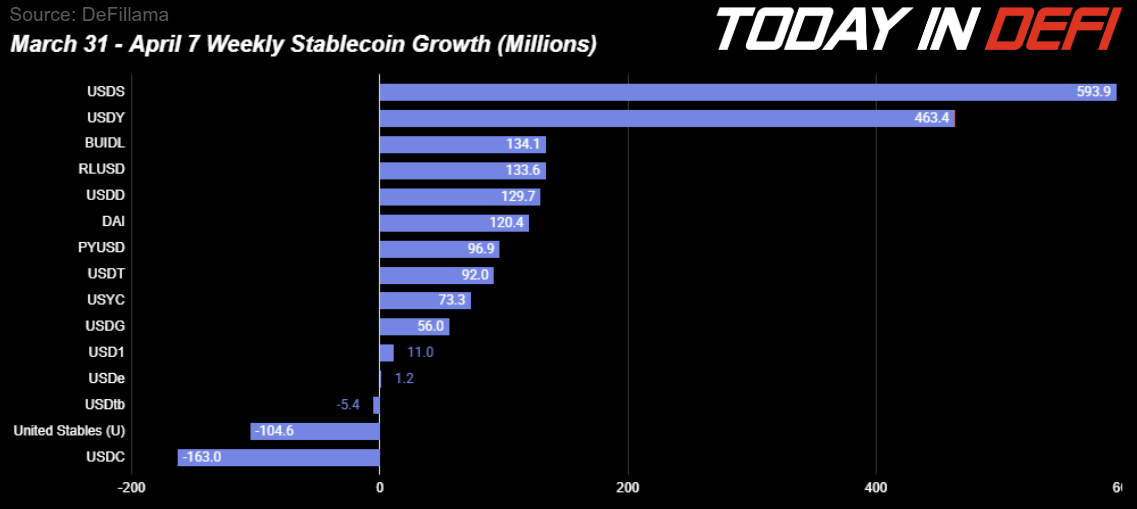

USDS led with +$593.9M. Sky Money has been losing ground to RWA competitors for several weeks, so this reversal is worth noting. The most likely explanation is yield dynamics, when market volatility spikes, crypto-native yields tend to rise sharply and temporarily outpace the relatively stable 4-5% T-bill floor.

In those windows, capital rotates back into instruments like sUSDS. Sky’s continued rate adjustments appear to be working.

USDY came in second at +$463.4M. The Ondo and Franklin Templeton partnership announced last week is still driving institutional interest into USDY’s product. The T-bill yield floor of 4.3–4.8% continues to make this an attractive place to park dollars for risk-averse allocators who still want to stay on-chain.

BUIDL (+$134.1M), RLUSD (+$133.6M), and USYC (+$73.3M) confirm that the on-chain T-bill space is not a one-horse race. BlackRock, Ripple, and Hashnote are all absorbing meaningful flows every week now. The RWA stablecoin segment as a whole is maturing.

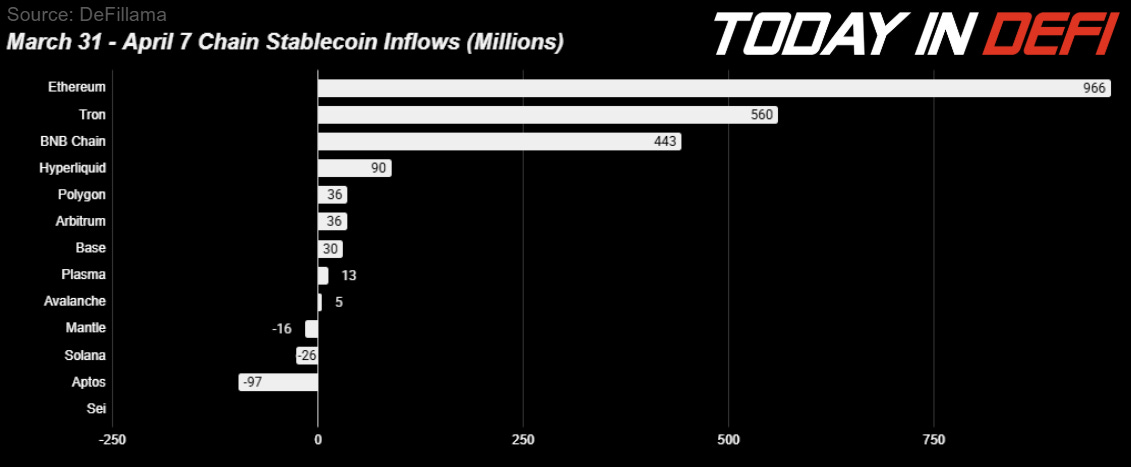

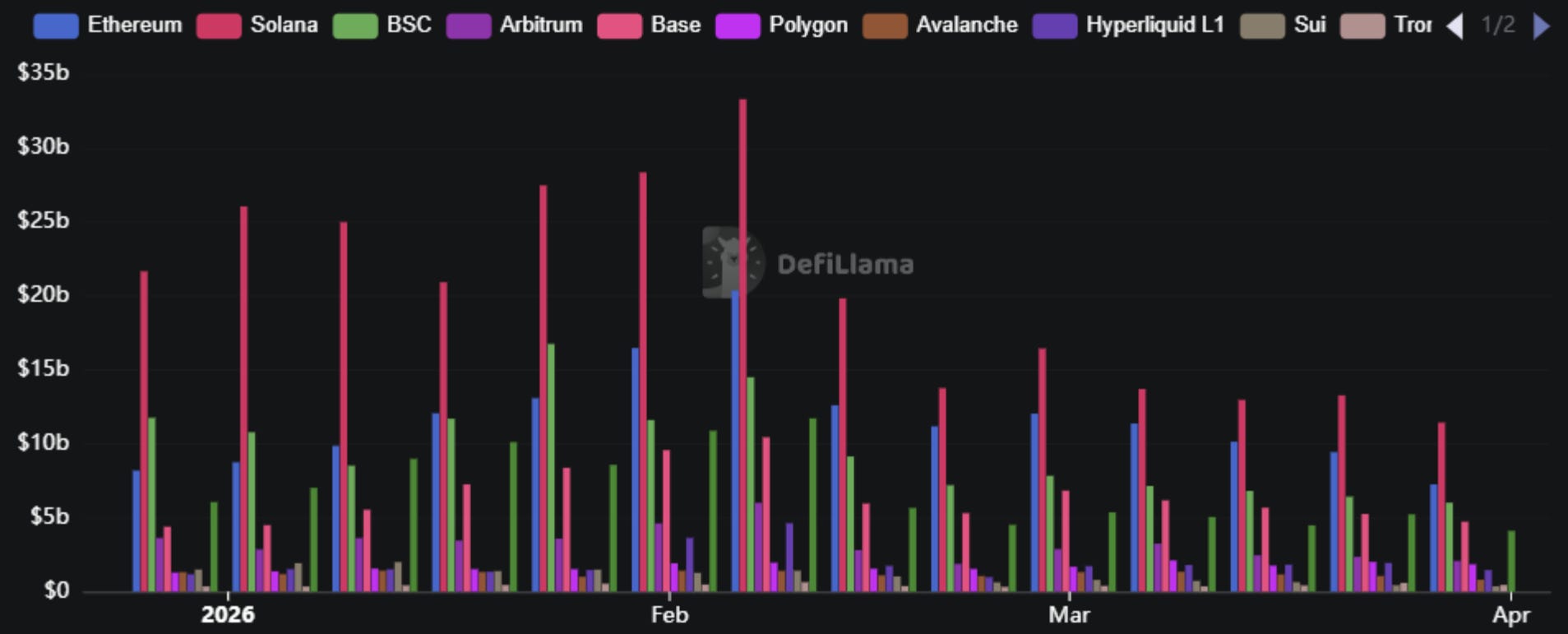

2. Stablecoin Flows Per Chain✅

Ethereum pulled in +$966M, nearly double the second-place finisher.

What has been driving Ethereum’s inflows?

RWA and low-risk yields are still driving the majority of inflows, like Grove, Ondo, and Securitize.

Liquid Collective, an institutional staking protocol, gained $165M TVL (+23.88%), driven by ETF demand and regulatory clarity around staking

Cap money gained around $30M TVL boosted by their Homestead points boost campaign that will last untill April, rewarding minting cUSD (their stablecoin).

Re.xyz raised its cap on Fluid, opening capacity that was previously a bottleneck for depositors. And StakeDAO is growing fast following its latest Morpho integration, with LP loop strategies attracting liquidity looking for compounded yield on top of base emissions.

YieldBasis added some fresh ETH inflows to Ethereum’s TVL as well, with the 25M cap filled within minutes after the hybrid vault launch

Tron’s +$560M is its own story. Tron operates almost entirely as a dollar-transfer rail for emerging markets and CEX-adjacent flows. The growth here is mostly boosted by USDD’s expansion on Tron is reinforcing this.

BNB Chain at +$443M continues to be underappreciated. The Binance ecosystem — PancakeSwap volume, USDD incentives, CEX-to-chain flows — is generating consistent stablecoin accumulation that rarely gets the narrative attention it deserves. BSC is not exciting. It is, however, working.

Hyperliquid’s +$90M is arguably the most interesting data point in this section on a per-protocol basis. This is a perpetuals DEX pulling in $90M in stablecoin inflows in a single week. That means traders are not just using Hyperliquid to trade and withdraw — they’re keeping capital there, staying positioned, treating it as a destination. That behavioral shift matters for how we think about Hyperliquid’s long-term TVL trajectory.

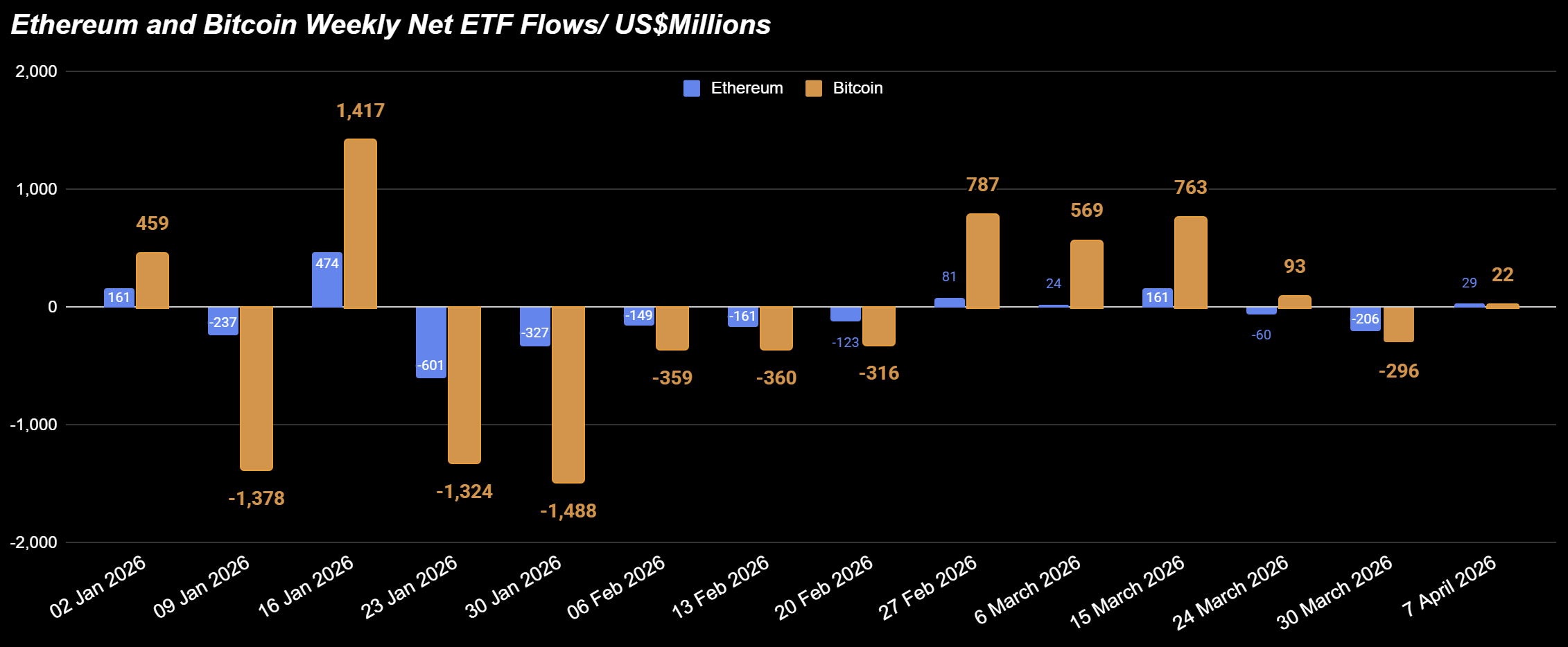

3. ETF Flows

The most recent week (April 7) tells a quiet but concerning story. Bitcoin ETFs pulled in just $22M and Ethereum $29M — technically inflows, but barely. After three consecutive strong weeks ($787M, $569M, $763M for BTC through late February to mid-March), the institutional buying momentum has clearly cooled.

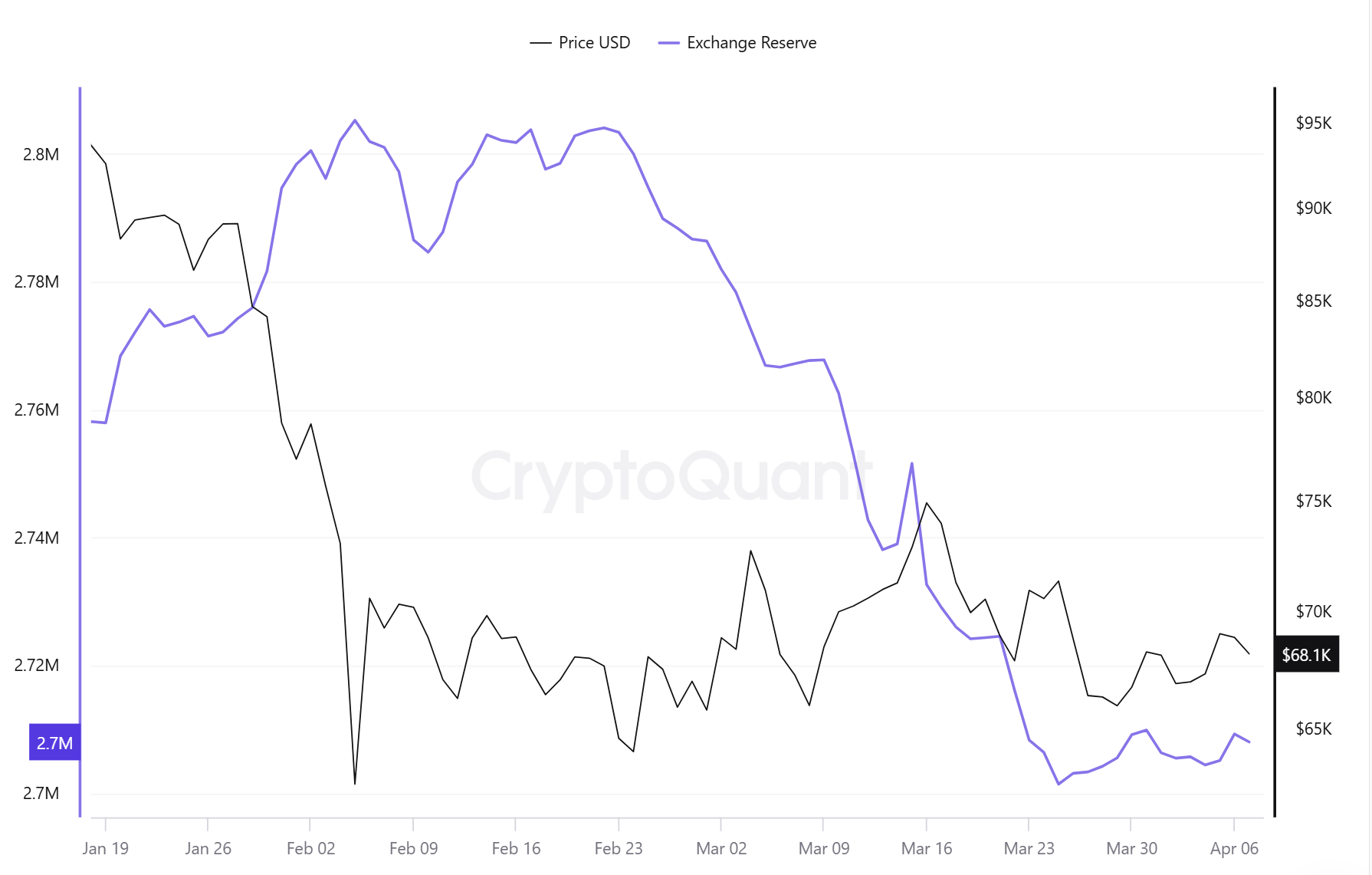

Bitcoin Exchange Reserves

Exchange reserves saw a slight uptick in the past week, with a small amount of BTC moving back onto exchanges around the April 6 period. Nothing dramatic, but worth noting — in the context of rangebound price action and geopolitical uncertainty, some holders are quietly positioning to sell into any strength.

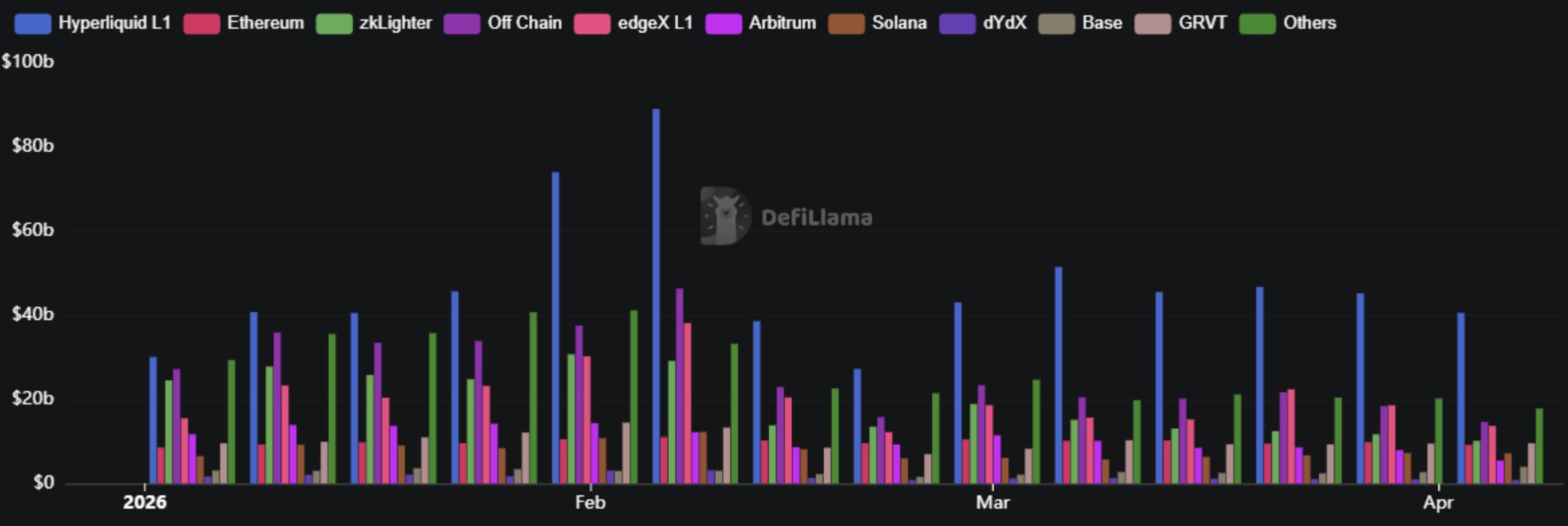

4. Perps and DEX Volumes Analysis

Apart from Hyperliquid’s obvious dominance, zkLighter (the green bar) has been growing visibly since February and is now a consistent third or fourth presence in the chart. This is Lighter’s perp infrastructure — and it connects directly to why LIT token was up 32.3% this week.

Solana is still #1 by weekly volume, and it's not close. But context matters here — Solana's dominance in spot DEX volume is a story about trading activity, not capital retention.

Base’s high DEX volume is quite impossible to ignore. $4.442B weekly from a relatively young L2 — and its 30-day number of $21.589B almost puts it ahead of BSC ($26B) on that timeframe. Sometimes, Base 24H DEX volume outperformed BSC’s volume.

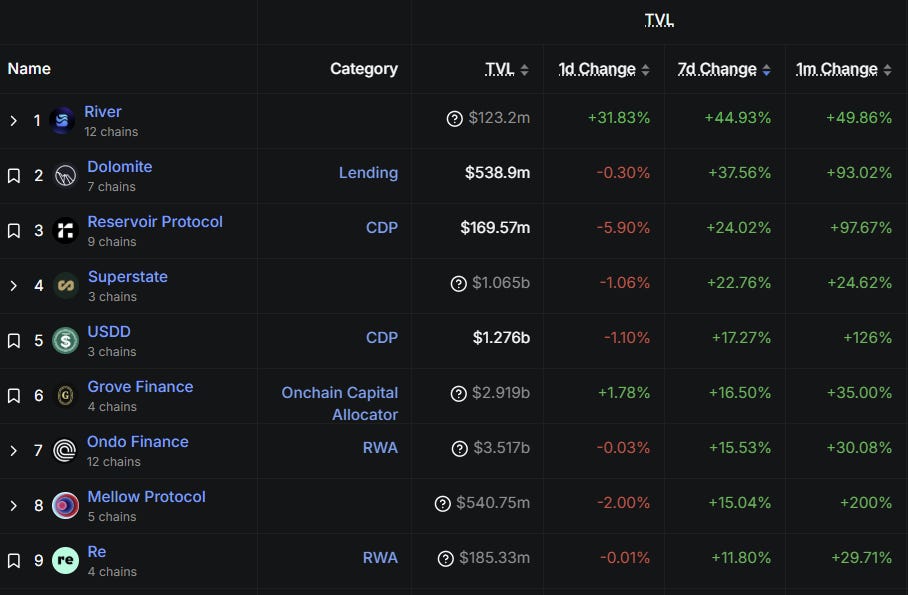

5. TVL gainers - for protocols above $100M

#2 Dolomite - Dolomite’s growth is not driven by pure lending/borrowing activities on the protocol, but rather WLFI, the DeFi project associated with the Trump family, deposited approximately 890M WLFI tokens (worth $295M) + 97.5M USDC + 17,700 WETH into Dolomite's treasury multisig, then borrowed 110M USD1 stablecoin against those positions, pushing lending yields for USD1 on Dolomite over 20% APR.

Please note⚠️ the lending APR for USD1 on Dolomite is very high, but carries the risk of bad debt due to the concentrated borrowers from the WLFI team and poor WLFI liquidity.

#3 Reservoir Protocol - CDP stablecoin protocol nearly doubling in 1 month (+97.67%). Reservoir’s main yield-bearing stablecoin (wsrUSD) has been gaining traction in the past month, thanks to low borrowing yields on top of incentives for borrowers on Morpho (Monad), offering up to 20% Looping APY.

Risk: Borrow rates on Morpho are variable; past 90% utilization can spike above your srUSD yield, turning the loan negative overnight.

#4 Superstate - managed to cross the $1B milestone this week. Their tokenized fund products, USTB and USCC, are drawing institutional capital that wants on-chain yield without crypto volatility exposure.

#5 USDD - Already covered in stablecoin flows. The TVL growth here mirrors the supply expansion — Morpho collateral integration for sUSDD, enabling 15%+ Stablecoin looping APY + CEX incentives for over 8% on Binance and Gate.io, all led towards USDD’s rising demand.

#7 Ondo Finance - Still growing post the Franklin Templeton announcement. At $3.517B, Ondo is the largest RWA protocol by TVL and continues to attract flows. The institutional pipeline is not exhausted.

#8 Mellow Protocol Lido’s EarnUSD and EarnETH vaults (5% APR) are continuing to drive structured yield demand. +200% monthly is a staggering number. Mellow is becoming the default curated vault layer for ETH and stablecoin yield in the Lido ecosystem.

Source: DeFillama

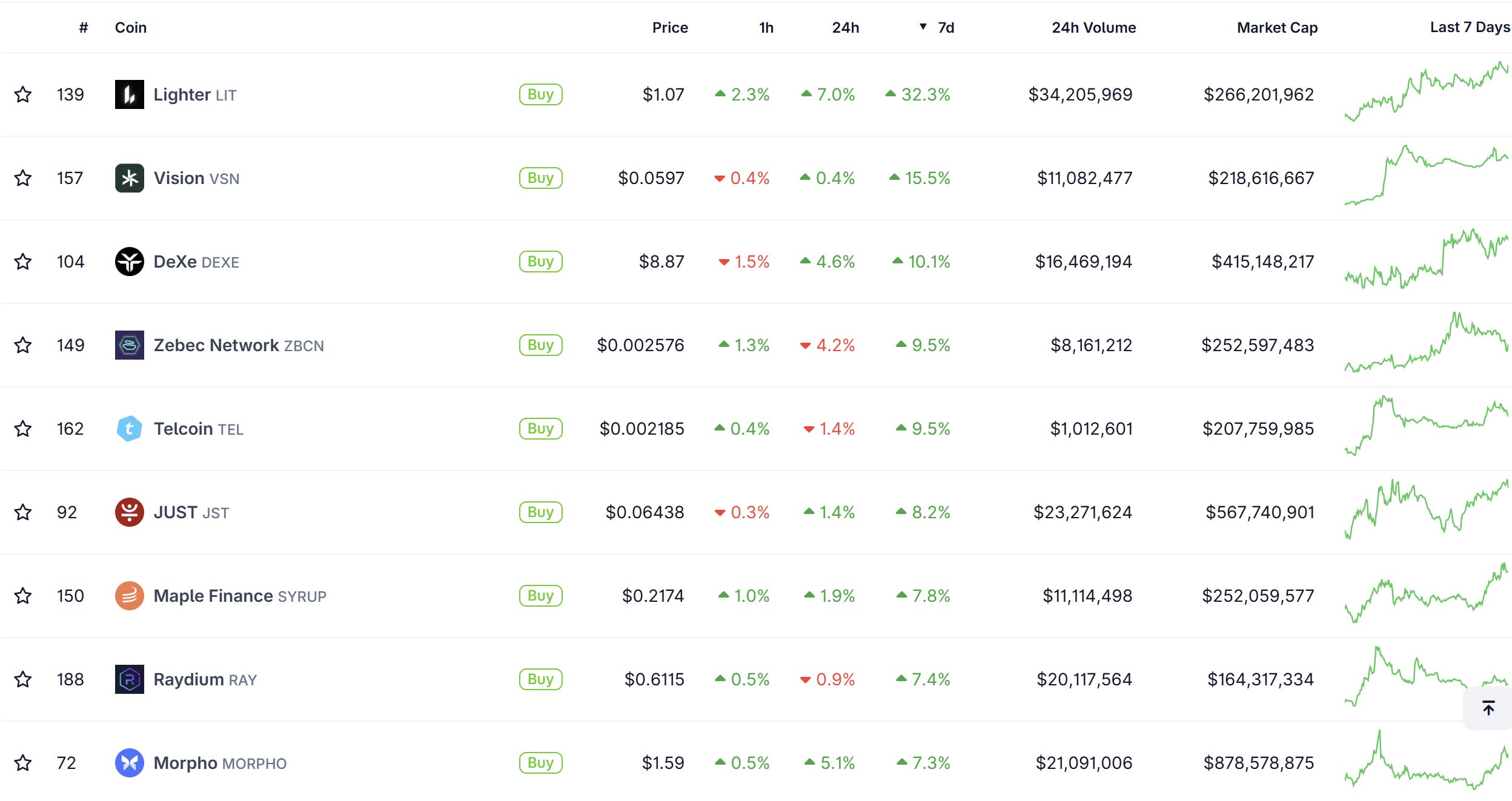

6. DeFi token price gainers & their catalysts

$LIT Lighter’s outperformed the entire DeFi category by a huge margin after it’s intergation with Telegram, allowing users to trade directly from their platform. Combined with visibly growing perps volume and a closing gap on Aster and Hyperliquid. Many didn’t notice - but Lighter is also running buybacks funded by 100% of the protocol revenue. Since TGE to this date, 4% of the LIT supply has been bought back and staked.

$DEXE DEXE’s token price has been up in the last few weeks, benefiting from Tally’s shutdown, which is also a governance tooling demand.

$SYRUP (Maple Finance) — Maple is now an agent for Spark, which is in charge of managing Spark’s private credit portfolio. This leads to speculation that Maple will be the next star for Sky Money’s manager for their private credit portfolio. March alone saw $440M in net new deposits, with syrupUSDC and syrupUSDT both hitting new supply ATHs.

$MORPHO is the most structurally important token catalyst of the week, even if the price move was quieter. The next major catalyst is their upcoming fixed-rate lending product, which is a big deal because every institutional credit market in the world — mortgages, corporate bonds, private credit — runs on fixed rates.

Supporting that narrative: the Ethereum Foundation added another 3,400 ETH into Morpho Vaults, and tokenized stock indexes (SPXY, deSPXA) are now launching lending markets on Morpho — expanding RWA collateral into equities for the first time.

Squeezing ~21.6% APR from a Peg:

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.