Aave & Uniswap Strengthen Against a Softening Macro - Onchain Outlook

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Headlines:

- Aave speeds up emergency response proposal

- Pendle expands aave fixed-yield integration

- Kamino launches one-click debt swap

- AlphaPing addresses mainstreet withdrawal concerns

- Synthetix’s sunsets sUSD after collapse

- Somnia launches frax-powered stablecoin

- Oku Trade adds tokenized stocks trading

- Morpho integrates with BitGo custody

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

Key Takeaways:

1. Macro reversed to risk-off; onchain sentiment improving.

The risk-on rally from last week took a break — the Fed turned hawkish (the dot plot now implies a hike, the dollar hit a multi-month high). The Iran deal also hit stumbling blocks. But onchain didn’t follow it down: stablecoin supply turned positive for the first time in five weeks, and leverage is slowly rebuilding.

2. Institutional flows led the chains again.

Real growth ran on settlement and payment rails with X-Layer as the standout (+8.14%): it’s ~93% USDG, with OKX paying up to ~4.1% APY to hold it. Plasma told the same story from the consumer side — its Thiel-backed neobank card launched June 17, routing idle balances into USDe and pushing it up ~31% on the chain in a week (a quiet tailwind for Ethena).

3. The TVL gains were real and built on infrastructure.

Every major gain this week came against falling prices, so the deposits are a genuine inflow, not price inflation. The two anchors: Aave’s TVL is climbing fast on a securities-finance proposal and institutional partnerships, and Uniswap’s V4 just crossed V3 in volume for the first time — a structural turn with clear advantages for tokenized RWAs.

1A. Traditional Macro

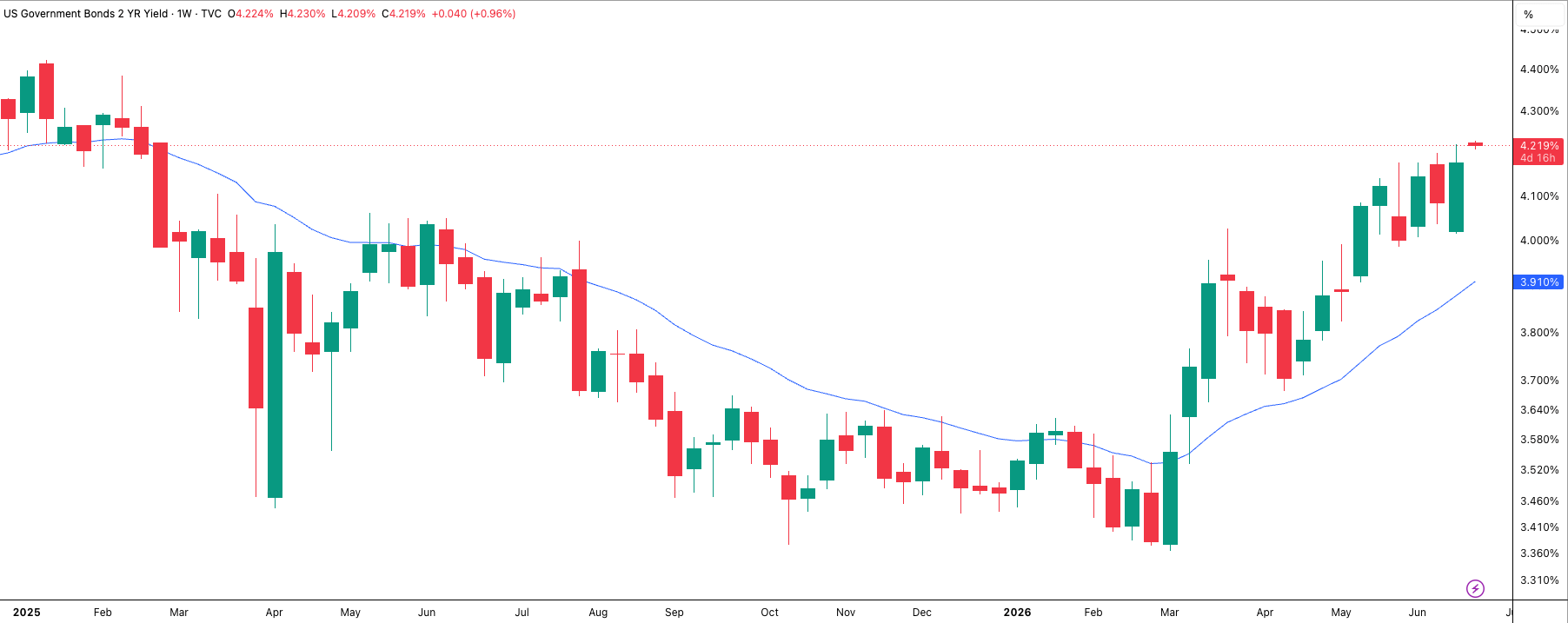

US 2Y yield

US 2Y yield: 4.219%, +0.96% WoW. TIGHTENING — the clearest signal of the week. The 2-year broke to new highs for the move and remains above its 20-week average. This is the direct echo of the Fed’s hawkish turn: when the committee removes its easing bias and the dots shift toward a hike, the 2-year — the most policy-sensitive part of the curve — reprices upward. Last week’s “rates easing = relief” has fully reversed.

DXY

DXY: 100.905, up on the week to a multi-month (year-to-date) high. HEADWIND. The dollar firmed as the safe-haven bid returned with the renewed geopolitical uncertainty, and as a hawkish Fed supports the currency. A stronger dollar is a background drag on crypto and risk assets.

The week’s macro headwind came from the Fed.

At Kevin Warsh’s first meeting as Chair (June 16–17), the FOMC held rates at 3.50–3.75%, but the projections turned hawkish: the median dot now implies a hike in 2026 rather than the cut penciled in back in March, the easing bias was dropped, and the inflation forecast was raised, with 17 of 18 officials seeing risks to the upside. Stocks fell and yields rose on the day — the move that pushed the 2Y to new highs and firmed the dollar to a multi-month high.

The US-Iran deal kept progressing — just not smoothly.

The memorandum was signed on June 17, and the first round of talks in Switzerland closed on June 22 with a road map toward a final deal within 60 days and a communication line to keep the Strait of Hormuz open, which mediators called “encouraging progress.” The path was bumpy — talks briefly stalled after Trump threatened to resume bombing and impose strait tolls, and Iran-Israel friction in Lebanon continued — but the ceasefire held and vessels can transit the strait toll-free for 60 days.

Composite: 2 clear headwinds (rates, dollar), and a still-weak crypto-vs-equities read. A decisive shift back from last week’s risk-favorable lineup — every lever that helped last week either reversed or stalled.

1B. Crypto Capital On-Ramp

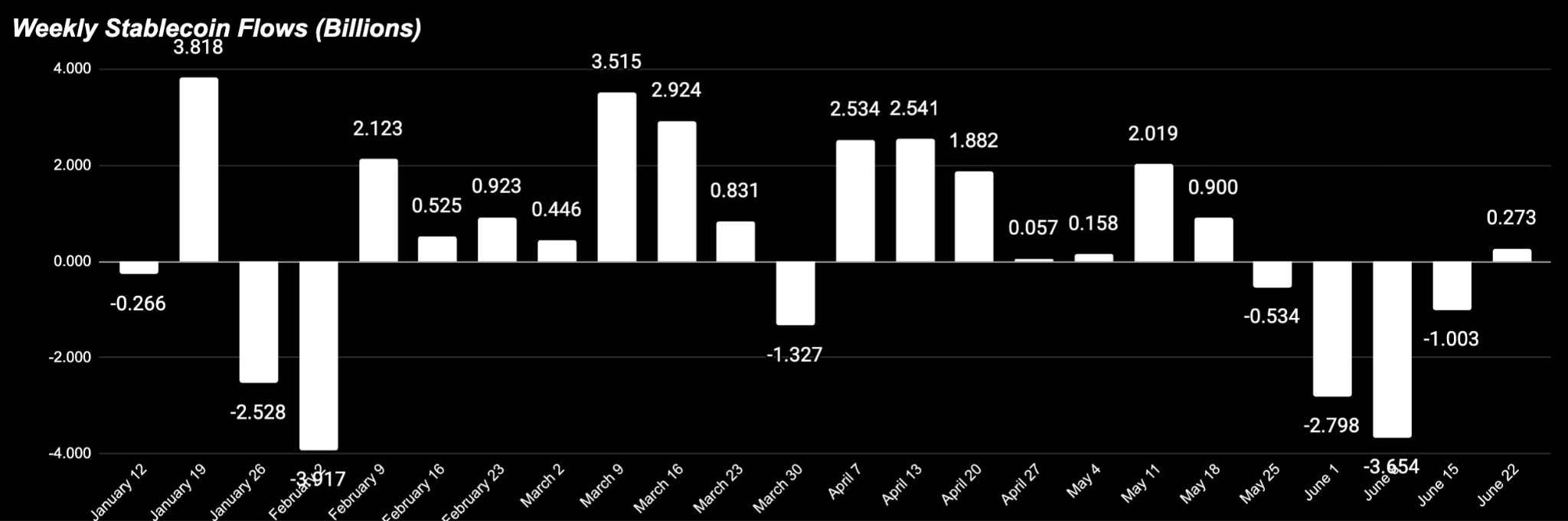

Total stablecoin supply 7d change

Total stablecoin supply — the bright spot. +$0.273B (+0.09%) is the first positive weekly print in five weeks (the prior four: −0.534, −2.798, −3.654, −-1.003). The bleed didn’t just decelerate; it turned marginally positive. It’s tiny, so “flat-to-slightly-positive” is the right framing — but directionally it’s the one place onchain is firmer than macro.

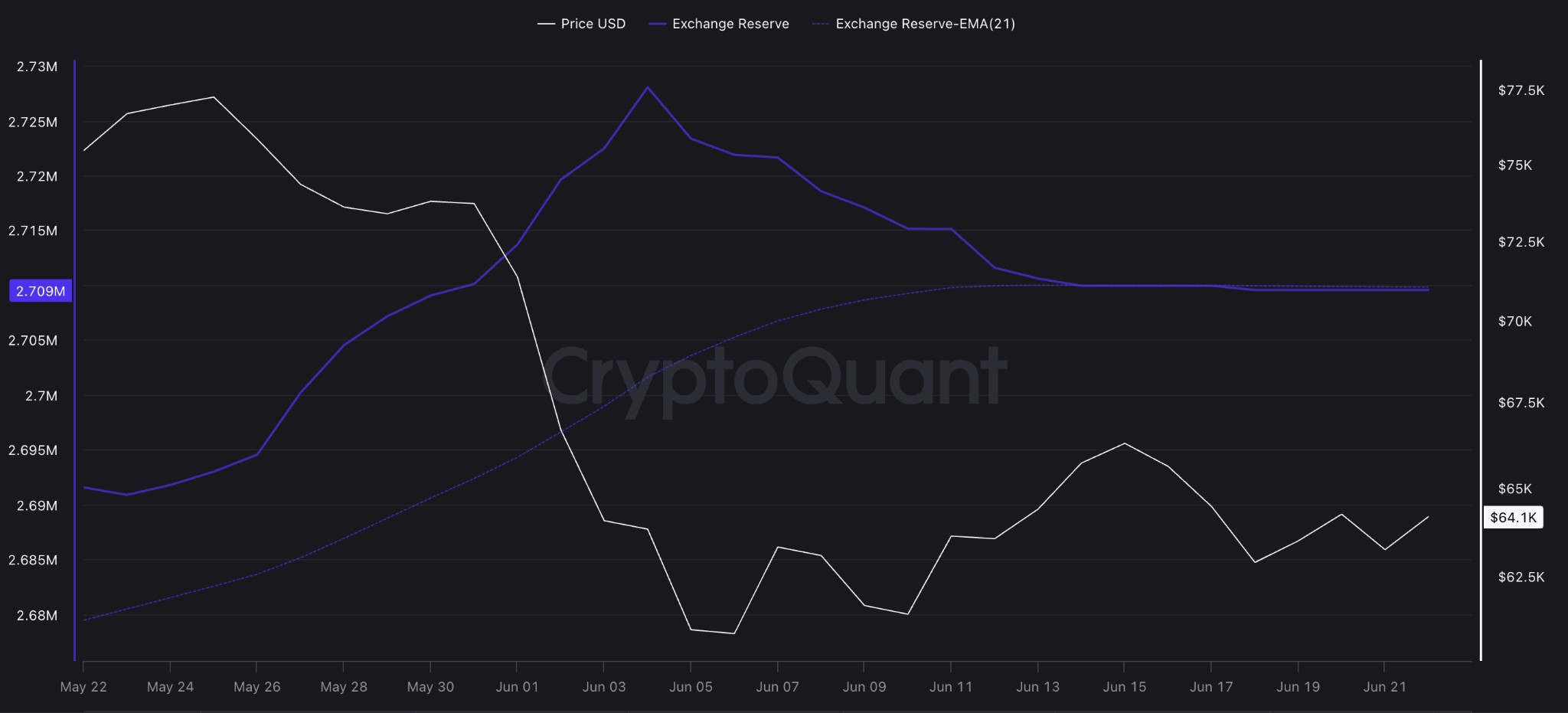

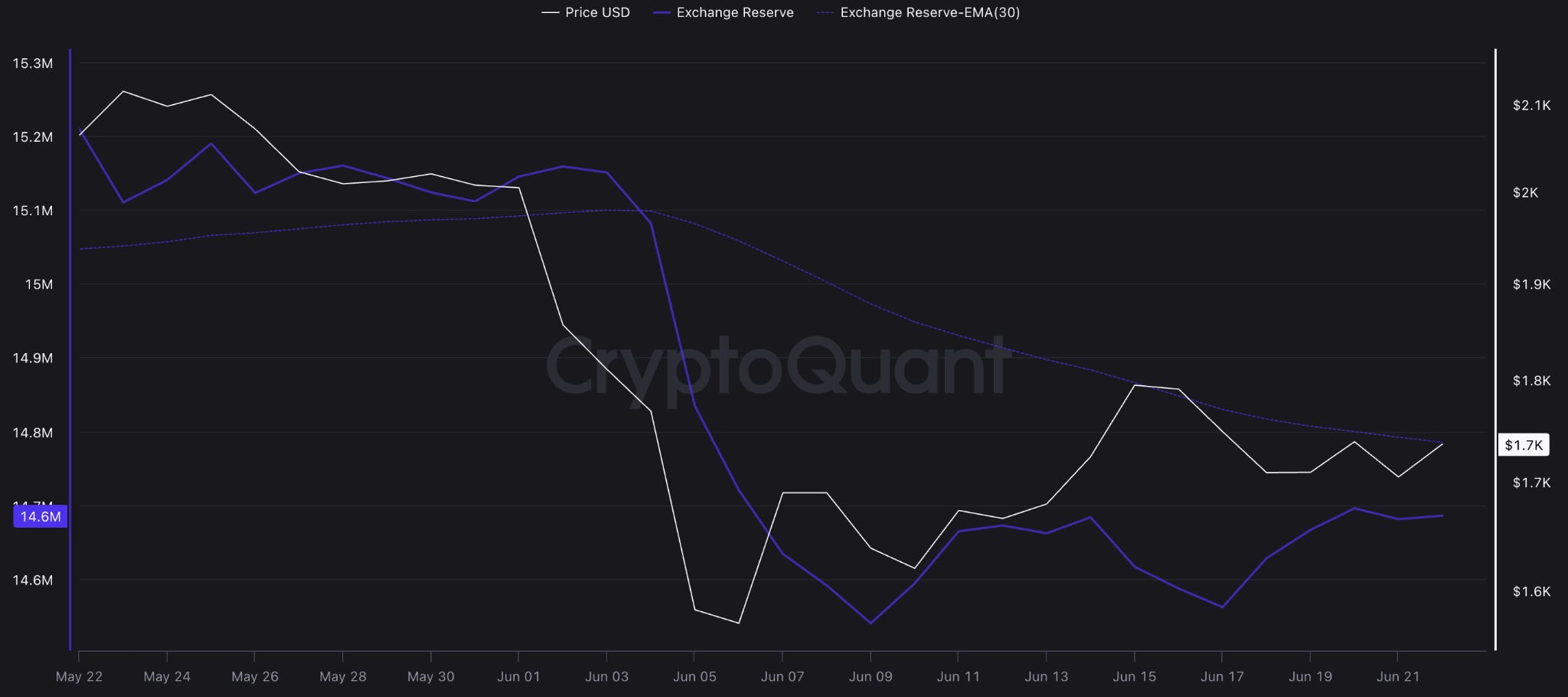

BTC and ETH Exchange Reserves

Mixed and slightly soft. Bitcoin exchange reserves have flattened — the accumulation signal from earlier in June has stalled, with coins neither leaving nor arriving in size.

Ethereum reserves ticked up, meaning some coins moved back onto exchanges while prices stalled, (a mild distribution lean) as price hovered. Neither chain is showing the clean accumulation we saw last week.

ETF flows

ETF flows — confirmed, and this counters last week. Bitcoin −$227.5M, Ethereum −$10M, Solana +$7M for Jun 15–21. Net clearly negative, BTC-driven, and you’re right it’s the sixth straight week of outflows. Last week we called the outflows “easing/possibly exhausting” — this week says they haven’t. The only positive is the small SOL inflow. Bearish.

1C. Week-Ahead Catalysts

⭐ Core PCE — Thursday, June 25. The Fed’s preferred inflation gauge, inside the Personal Income and Outlays report. An important number of the week. The Fed just raised its 2026 inflation forecast and flagged risks to the upside, so a hot print would harden the case for a hike and push yields and the dollar higher still; a soft print would take some pressure off a tape that’s already leaning hawkish.

⭐ US-Iran talks, the Strait, and the Lebanon ceasefire. The major swing factor for oil and risk. Watch three things:

whether the Switzerland talks hold or break down,

whether the Strait of Hormuz dispute resolves toward “open” (US position) or “closed” (Iran’s position),

and whether the Israel-Hezbollah ceasefire sticks — Israeli strikes on Lebanon are the thing most likely to blow up the agreement. Oil’s path is the cleanest real-time read on which way this is going.

Section 2 — Onchain Risk Regime

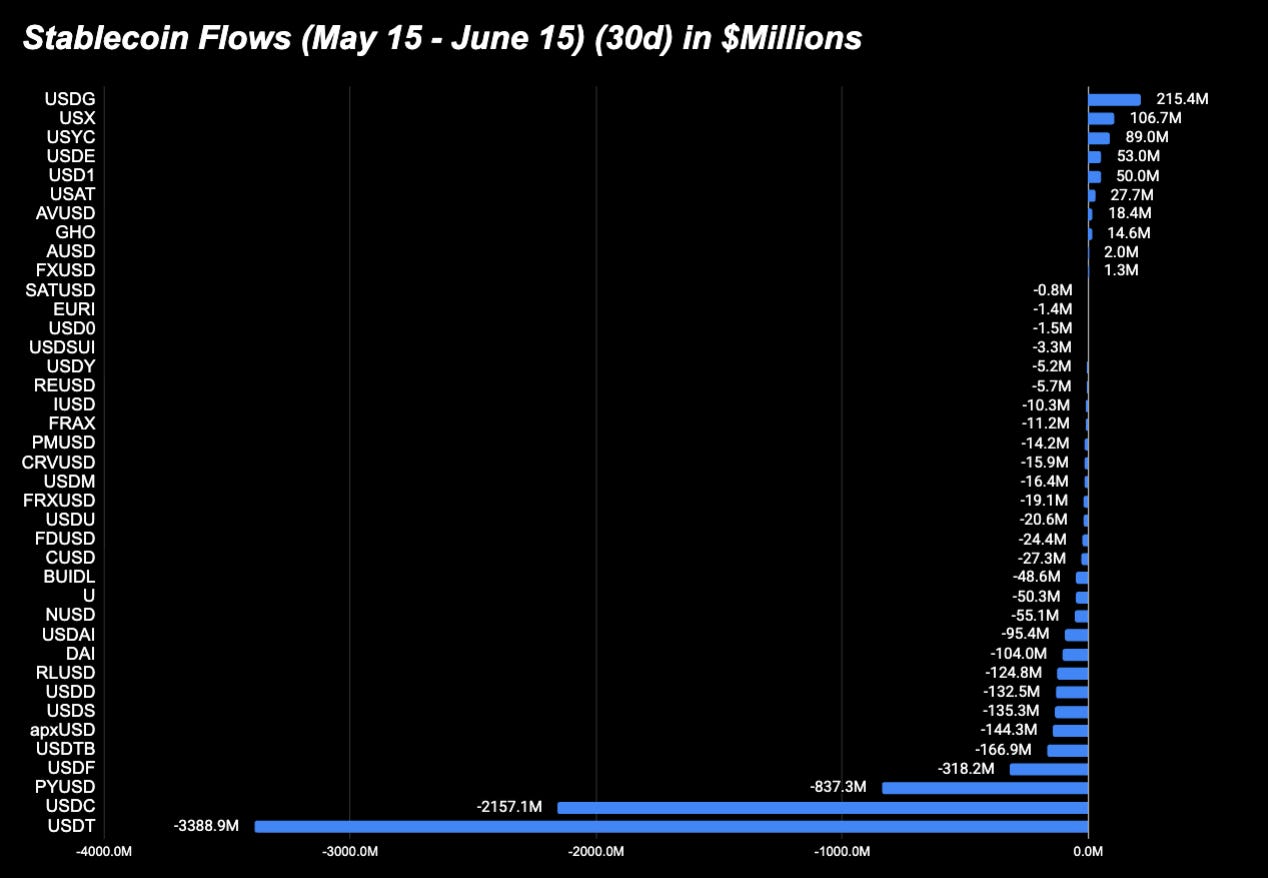

Individual Stablecoins Flows

capital rotating out of transactional dollars and into yield-bearing and tokenized-Treasury ones. This week that signal got muddier, because the two biggest movers were issuer-specific swings rather than a theme.

The gainers: USD1 led the entire table, up +$405.9M (+9.25%) — but USD1 is World Liberty Financial’s transactional dollar, not a yield product, but it’s famous for the 5% APR Binance campaign that has been running for months now. Behind it, the tokenized-yield and institutional names did grow: USDG +$174.5M (+6.73%), USYC +$58.7M (+1.95%), and DAI +$56.5M (+1.28%).

The losers: the biggest decliner was USDS, down −$293.0M (−3.47%) — and USDS is Sky’s yield-bearing dollar, which cuts directly against any clean yield-rotation story. USDT, the largest transactional dollar, kept bleeding (−$223.7M), while USDC was essentially flat (+0.05%).

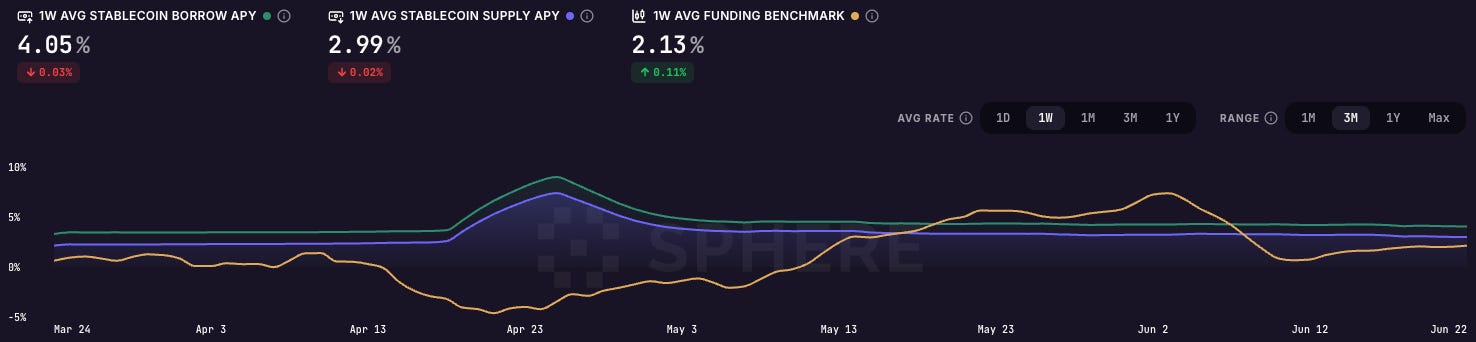

Aave / Sphere Rates

Borrow 4.05% (−0.03%), supply 2.99% (−0.02%), funding 2.13% (+0.11%). Borrow/supply soft and calm; funding rose for a second week running (1.73% → 2.13%) and is now approaching the supply yield but still below borrow.

Leverage demand is slowly rebuilding off the lows, but not greedy yet (funding < supply < borrow). A mild risk-on undercurrent — worth noting as a small tension against the risk-off macro.

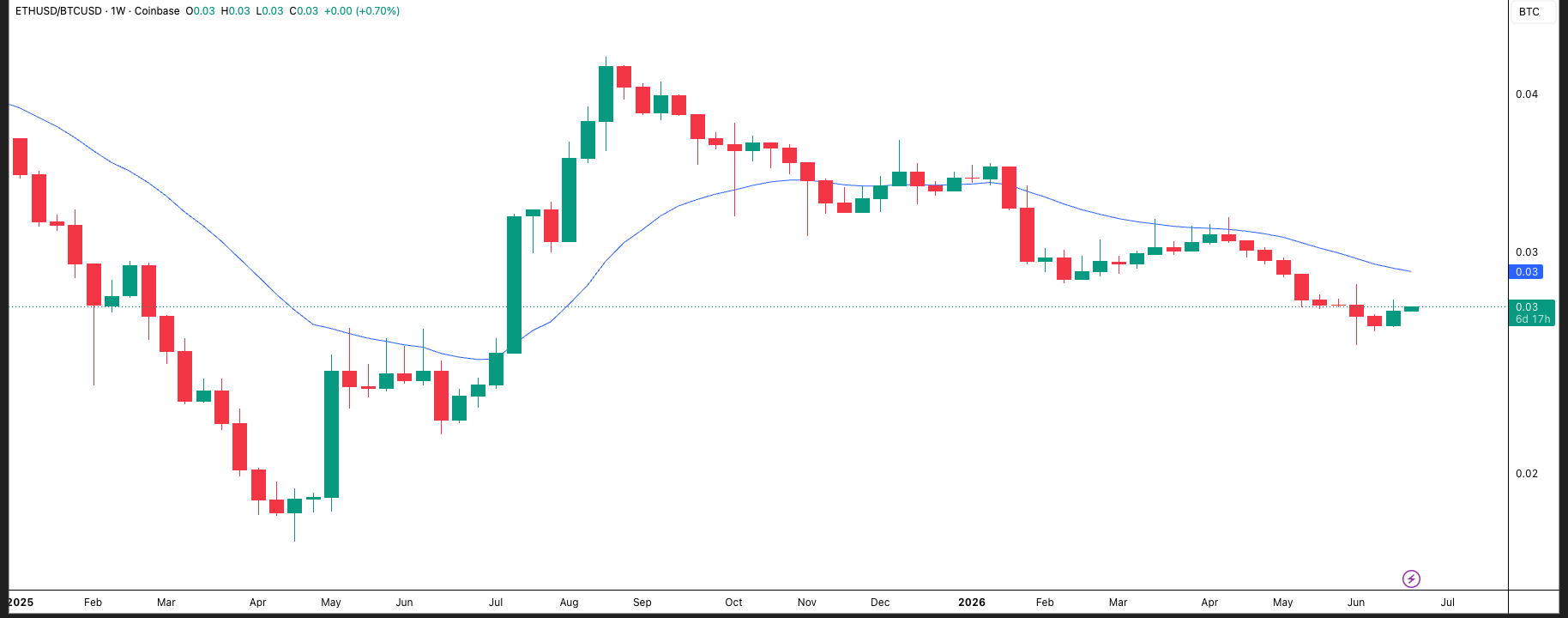

ETHBTC vs 20W MA

ETHBTC is forming a second consecutive green weekly candle (+0.90%) after nine straight red weeks — ETH starting to outperform Bitcoin at the margin for the first time in 9 weeks. The catch: it’s still trading below its 20-week moving average, so this is early relief, not a confirmed regime shift. A turn worth tracking, but it needs another week or two of follow-through before it means anything structural.

Onchain regime STABILIZING.

Against a deteriorating macro backdrop, the onchain signals lean quietly constructive — leverage is rebuilding (funding up two weeks running), ETH is showing its first relative strength in months, and the dollar base steadied. The caveats keep it from being a clean risk-on call: the stablecoin composition was noisy this week rather than a clear rotation, and exchange flows softened.

Section 3 — Chain Comparison

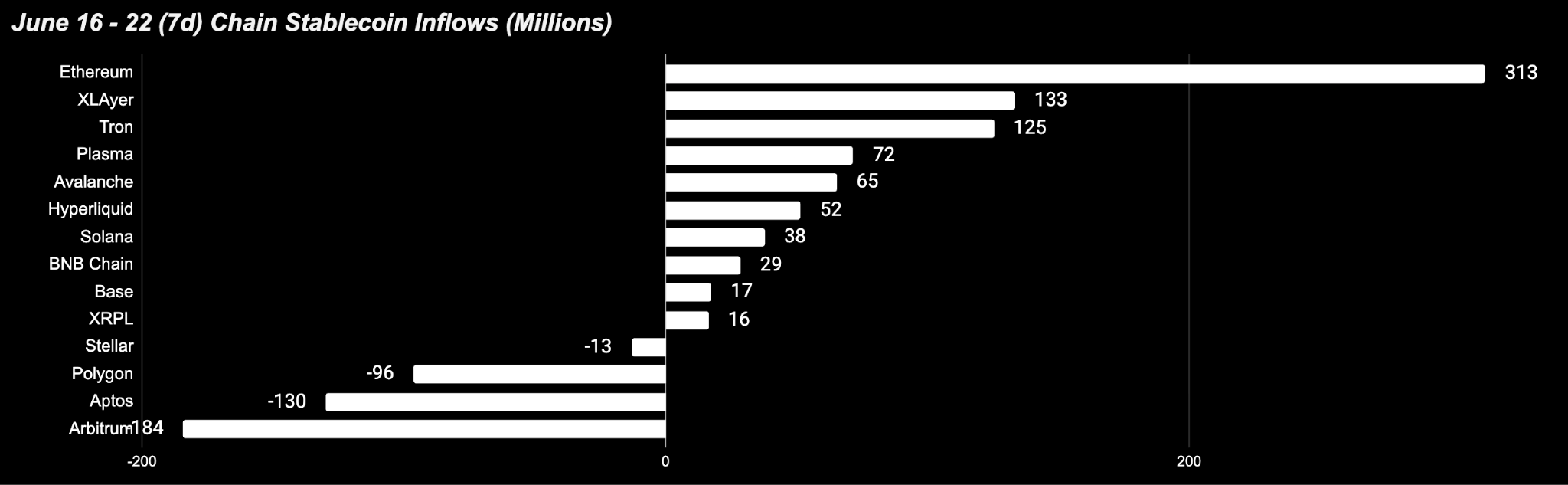

3A. Stablecoin flows by chain

Dual catalyst in action: Roughly 93% of supply is USDG, held under OKX's Exchange OS framework, which pays as much as 4.1% in annual yield. The chain functions, in effect, as OKX's settlement and yield vehicle for the Global Dollar.

A 310% rise in DEX volume traced to a promotional World Cup prediction market; the supply growth beneath it is structural. The concentration is the risk — with one issuer accounting for nearly all supply, a reallocation of USDG would drain the chain's liquidity.

Plasma One’s June 17 neobank launch — Peter Thiel-backed, Visa card, up to 5% yield — produced an immediate supply response. USDe surged +30.9% in a single week. With 5,000 weekly active users from private beta and the highest fee-per-volume ratio among purpose-built chains, the consumer demand signal is real, though unit economics at scale require validation.

Plasma is a purpose-built stablecoin Layer 1 with zero-fee USDT transfers and full EVM compatibility, launched September 2025. USDT dominates at $926.75M (82.1%); USDe at $153.43M (13.6%) is recovering from a March peak of $394M. The June 17 Plasma One neobank launch drove a same-day DEX volume peak of $42.15M and a +86.1% weekly volume surge.

RLUSD accounts for 93.8% of supply, positioning ahead of settlement activity rather than reflecting it: Mastercard included RLUSD in its June 3 settlement expansion, though no partner has disclosed live volume.

More notable is OpenEden's TBILL at 5.5% of supply, an early sign that institutional real-world-asset issuance on XRPL is broadening beyond Ripple.

The presence of TBILL at 5.5% is a forward signal: institutional RWA issuance beyond Ripple itself has begun on XRPL. OpenEden’s deployment suggests the chain is beginning to attract yield-seeking institutional allocators, not just stablecoin settlement flows.

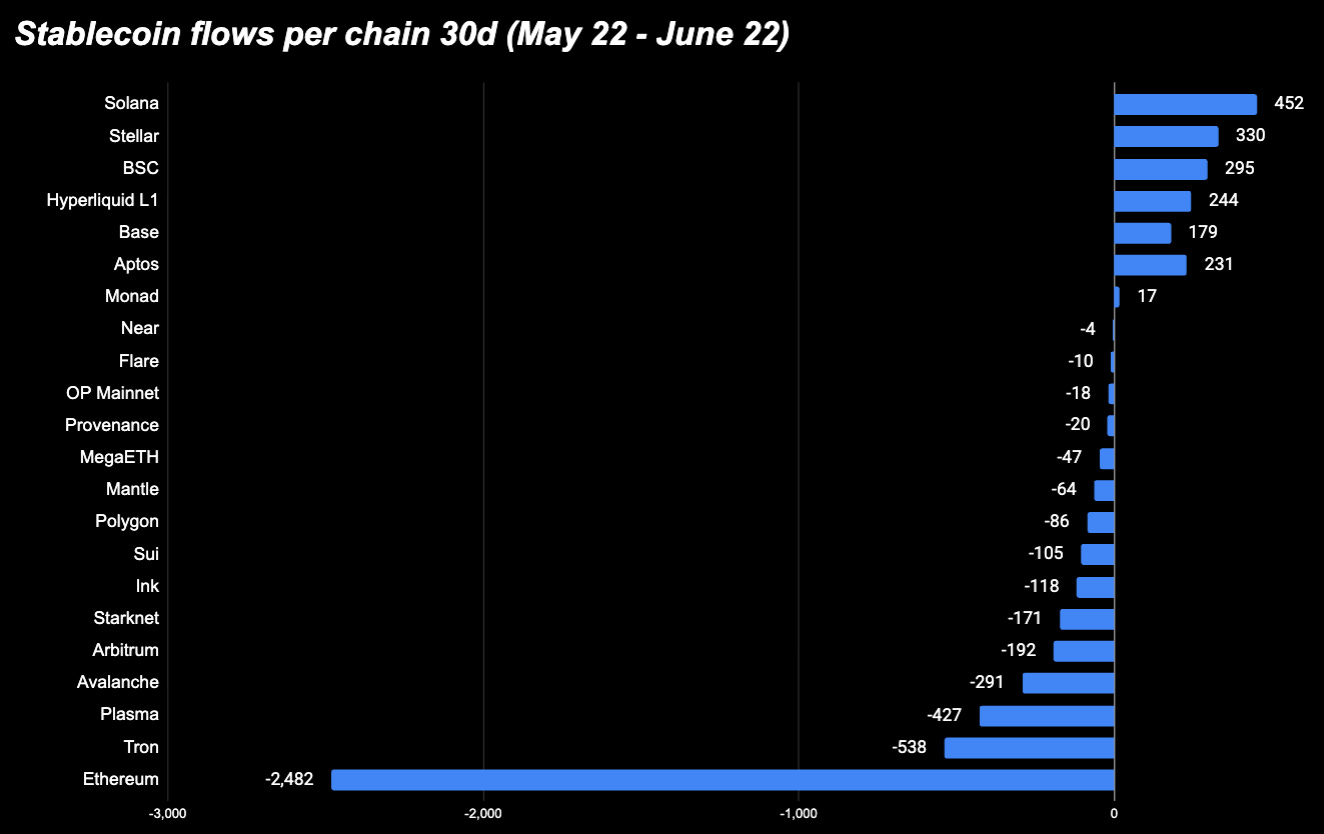

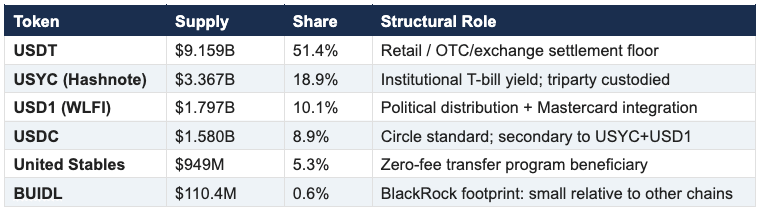

A marginal weekly gain obscures the largest 30-day outflow in the dataset. The capital is not moving to Ethereum's own layer-2s but to Hyperliquid and Solana; Circle transferred $4.4 billion of USDC to Coinbase via HyperEVM and minted roughly $1 billion on Solana. Ethereum remains the dominant custody chain, but no longer the default venue for growth.

The most stratified institutional base of any chain in the set: USYC and USD1 together, at about $5.2 billion, now exceed its entire USDC supply. The week's growth came from institutional collateral minting rather than retail activity, with DEX volume down 15%. Hashnote's USYC triparty fee waiver expires June 30; at $3.37 billion, a partial reallocation would rank as the quarter's largest single-chain stablecoin move.

Hyperliquid’s stablecoin supply has overtaken Arbitrum's, a structural crossover, even as the 30-day figure declines on the unwind of post-AQA governance enthusiasm ahead of October's yield activation.

The defining characteristic is leverage: seven-day derivatives volume runs at 7.3 times the stablecoin base, far above any other chain. The network operates as a leverage engine rather than a custody layer.

3B. Structural Shifts- DEX Volumes

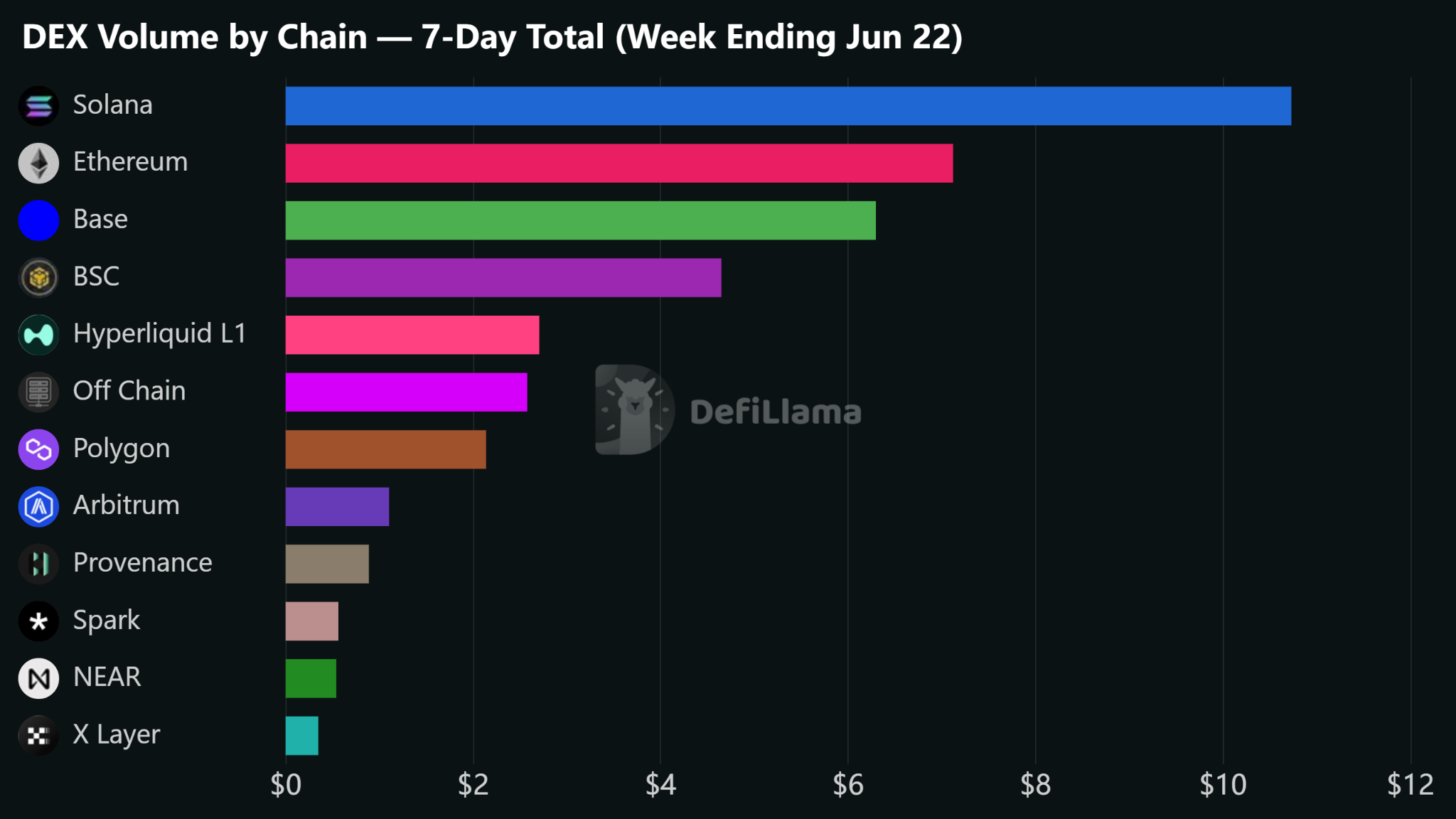

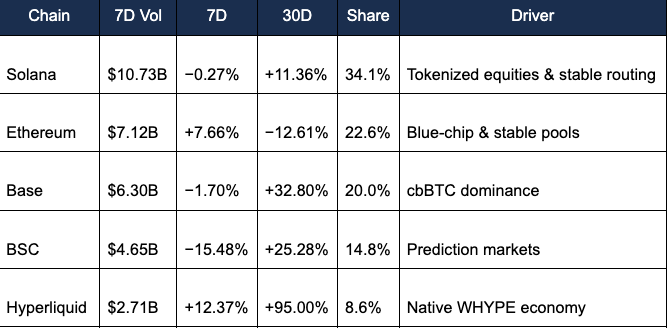

Aggregate seven-day DEX volume across the five largest ecosystems reached about $31.51 billion. The headline suggests consolidation, but the composition is diverging: Solana is converting tokenized real-world assets into native liquidity, Ethereum is separating into a two-tier routing structure, and the remaining chains are specializing.

Solana

Tokenized equities have matured into core liquidity. The S&P 500 token (SPYX/USDC) is now the second-largest pair on Orca at 20.8% of venue volume, and equities account for more than 22% of the venue’s flow, up from near zero two months ago. Manifest operates as an institutional stablecoin settlement hub. Speculative launch activity on PumpSwap remains profitable but no longer defines the chain.

Ethereum

The market has split into two venues. Uniswap V4 has become the institutional stablecoin routing layer, with stablecoin-to-stablecoin pairs near 72% of its volume, while Uniswap V3 retains blue-chips and tokenized gold (XAUT, PAXG), reflecting steady hard-asset demand. Two parallel economies now operate on the same chain.

Base

Aerodrome handles about 47% of Base volume and is concentrated in cbBTC pairs, tying activity to Bitcoin sentiment. Beneath that, Uniswap V4 has grown to 2.75 times the size of V3, and an EURC-denominated FX layer is emerging.

BSC

Volume fell 15% as Binance incentive campaigns wound down, but prediction-market venues (OPINION, Predict Fun) expanded against the trend, indicating non-speculative demand building underneath.

Hyperliquid

The chain leads all majors on 30-day growth at 95%, though the activity is largely self-referential: HYPE and WHYPE pairs dominate both the spot orderbook and Project X, with WHYPE serving as the network’s base unit of account, comparable to ETH on Ethereum.

Section 4 — Project & Protocol Discovery

4A. Token Price Movers - Observations, not trade ideas.

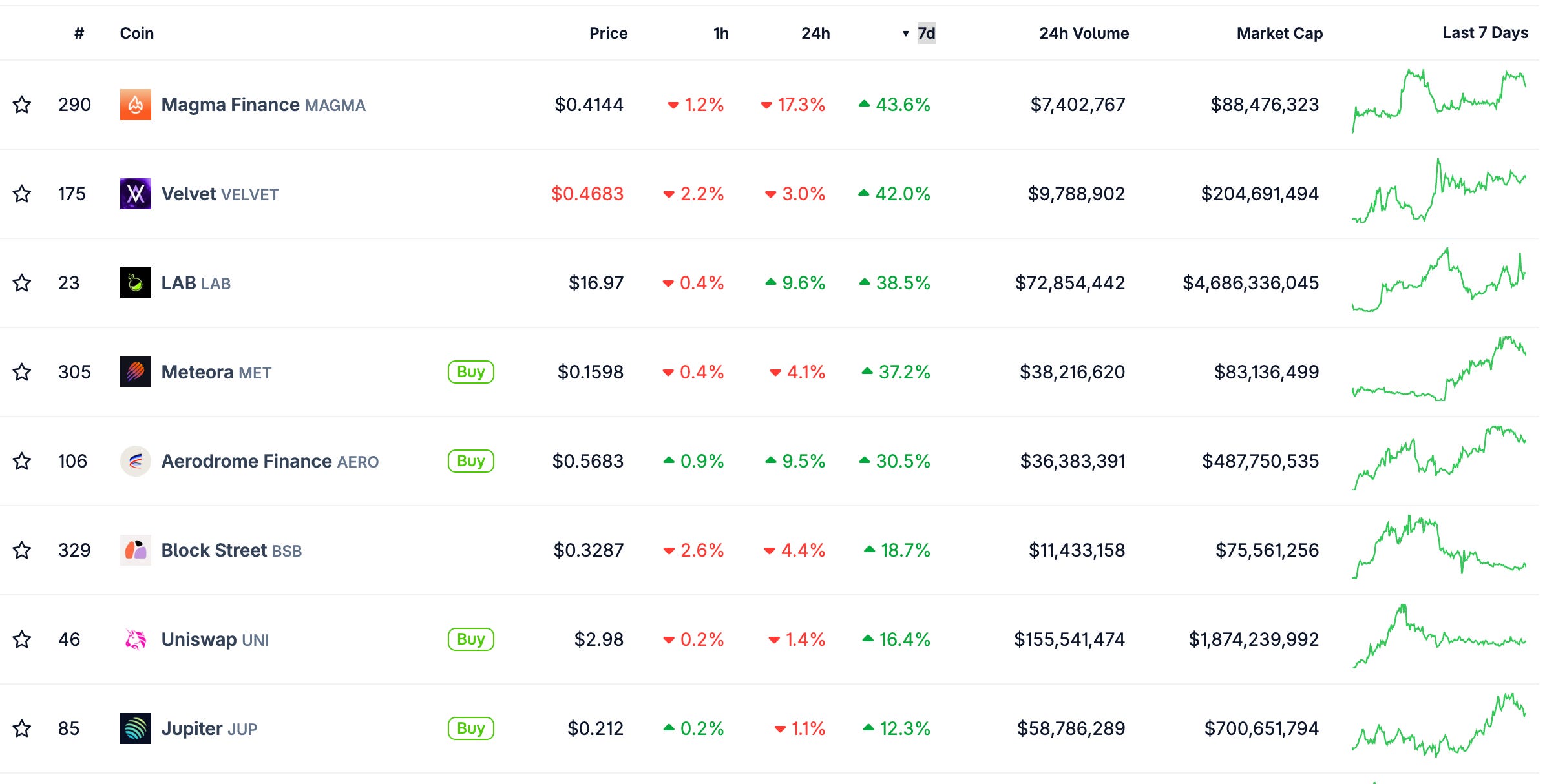

Meteora — MET, [+37% 7d]. One of the week’s strongest performers on Solana, on reported DLMM fee-revenue growth of +63.66% over 30 days (June 18) and a launchpad SDK update (June 19) — a sign of resilient demand for its liquidity products even as Solana DEX volume cooled earlier in the month. Also a mover last week.

Aerodrome — AERO, [~+30% 7d] . Its Predictive Allocation model — which ties liquidity incentives to correctly anticipating future demand — was unveiled around June 17 and sparked the rally. This is the same upcoming catalyst we flagged last week as a July launch; it’s now showing up in price rather than being fresh news. source

Uniswap — UNI, [~+16% (7d)]. The week’s clear standout. Standard Chartered initiated coverage on June 15 with a $100 price target by end-2030 — one of the most aggressive forecasts yet from a major bank for a DeFi token, built on a thesis that tokenized real-world assets increasingly trade through DeFi. The protocol’s fee switch (live since December 2025) also buys back and burns UNI, removing supply over time.

Jupiter — JUP, [+12% 7d]. A governance proposal around June 14–15 to lift the share of protocol fees routed to buybacks and burns from 50% to 70% — a deflationary tweak.

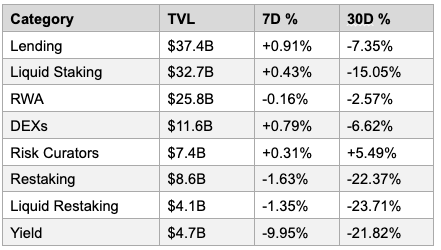

4B. TVL Gainers ($50M+ filter)

This week’s TVL gains are the cleanest in months. Each came against falling prices — ETH −3.36%, BTC −3.23%, SOL −0.08% — meaning the headline figures understate the underlying deposits. The growth reflects genuine inflows rather than price appreciation.

Sector Overview:

Lending — Aave: Five Simultaneous Institutional Signals

Aave posted one of the week's strongest TVL gains despite ETH falling 3.36%, indicating genuine net deposit growth rather than asset price appreciation. Growth was concentrated in V3 lending markets, while the Horizon RWA tier declined 1.26%.

Several institutional catalysts converged within days.

BitGo Bank & Trust, the first OCC-regulated digital asset trust bank, launched direct Aave access through Narval's institutional gateway, allowing clients to access Aave without moving assets out of qualified custody.

Meanwhile, Stani Kulechov proposed bringing repo and securities lending markets onto Aave V4’s architecture, with the initiative publicly amplified by both Aave leadership and CEO Luigi D’Onorio DeMeo, signaling growing institutional ambitions.

Aave Labs also proposed deploying V4 on Avalanche, supported by up to $15M in milestone-based incentives from the Avalanche Foundation, likely encouraging pre-positioning deposits into the ecosystem ahead of launch.

Caveat: The 30D figure (-6.65%) provides essential context. Aave is recovering from a deeper drawdown.

Uniswap: Three Events, One Structural Inflection

Uniswap reached a structural milestone as V4 volume surpassed V3 for the first time. V4 now holds 36.9% of the combined V3-V4 TVL while generating 62.6% of the volume.

Three catalysts converged within 48 hours:

(1) tokenized securities launched across Uniswap products, with over $9.1B traded in RWA pools, a use case enabled by V4's compliance-focused hook architecture

(2) Standard Chartered initiated UNI coverage with a $100 price target by 2030, helping drive a 44.7% rally, though TVL growth remained driven by LP migration and tokenized asset liquidity rather than token price; and

(3) the SEC proposed repealing key Regulation NMS rules, a structural tailwind that could further accelerate tokenized stock trading on DeFi rails.

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.