Amplifying Stablecoin LP APY with Leverage: Tangent and LlamaLend v2

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Headlines:

- Morpho expands coinbase earn vaults

- Superform launches 14% usdt vault

- infiniFi adds siusd pendle market

- Morpho raises record $175m round

- Citigroup issues tokenized private shares

- Tori Finance opens pre-deposit vault

- Re launches new Pendle markets

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi

As capital efficiency remains paramount in DeFi, leveraging stablecoin liquidity provision (LP) positions has emerged as a core strategy for yield optimization. Rather than deploying capital passively, a growing class of protocols enables traders to utilize yield-bearing LP tokens as productive collateral — borrowing against them to amplify exposure while maintaining the underlying yield stream.

This guide outlines a comparative framework for three protocols offering these mechanics: Curve LlamaLend v2, and Tangent, evaluating their underlying architectures, multi-layered yield generation, execution frictions, and distinct risk profiles. Each represents a fundamentally different architectural approach to the same problem: how to leverage a stablecoin LP position without abandoning its yield.

1. Why Stablecoin LP Leverage Matters

The emergence of protocols dedicated to leveraging stablecoin LPs is a direct response to structural inefficiencies in the current DeFi landscape.

Structural Issues Solved

The “Low-Yield” Cap on Delta-Neutral Capital: In standard market conditions, organic stablecoin LP yields generally range between 5% and 12%. Traditional money markets do not natively support looping these complex yield-bearing LP positions efficiently, leaving massive amounts of sidelined capital underutilized.

Capital Efficiency Ceilings on Full-Range LPs: Traditional constant-product or StableSwap LPs distribute capital across the entire price curve, leaving the vast majority of deployed assets idle at any given price point. Concentrated liquidity (Uniswap v3) solves this structurally but introduces active management requirements that create a natural demand for integrated lending and automation platforms.

Liquidity Fragmentation & Execution Slippage: Liquidity across decentralized exchanges is often heavily fragmented. Executing market swaps with larger sizes frequently incurs significant price impact, creating friction for capital deployment and degrading overall trading efficiency.

Strategic Opportunities Created

Amplified Delta-Neutral Yields: By utilizing automated or structured leverage loops, baseline stablecoin yields can be amplified into the 20% to 45%+ range. Because the underlying assets are pegged stables, users can target equity-like returns while maintaining a structurally delta-neutral profile.

Productive Collateralization: LP tokens are no longer the end point of a capital journey; they become the foundational collateral for secondary credit expansion.

Incentivizing Deep Market Liquidity: By offering outsized, leveraged yields, these frameworks create a massive incentive for users to supply capital. This draws deep, concentrated liquidity into the underlying AMM pools, healing fragmentation and drastically reducing the price impact for all market participants executing standard swaps.

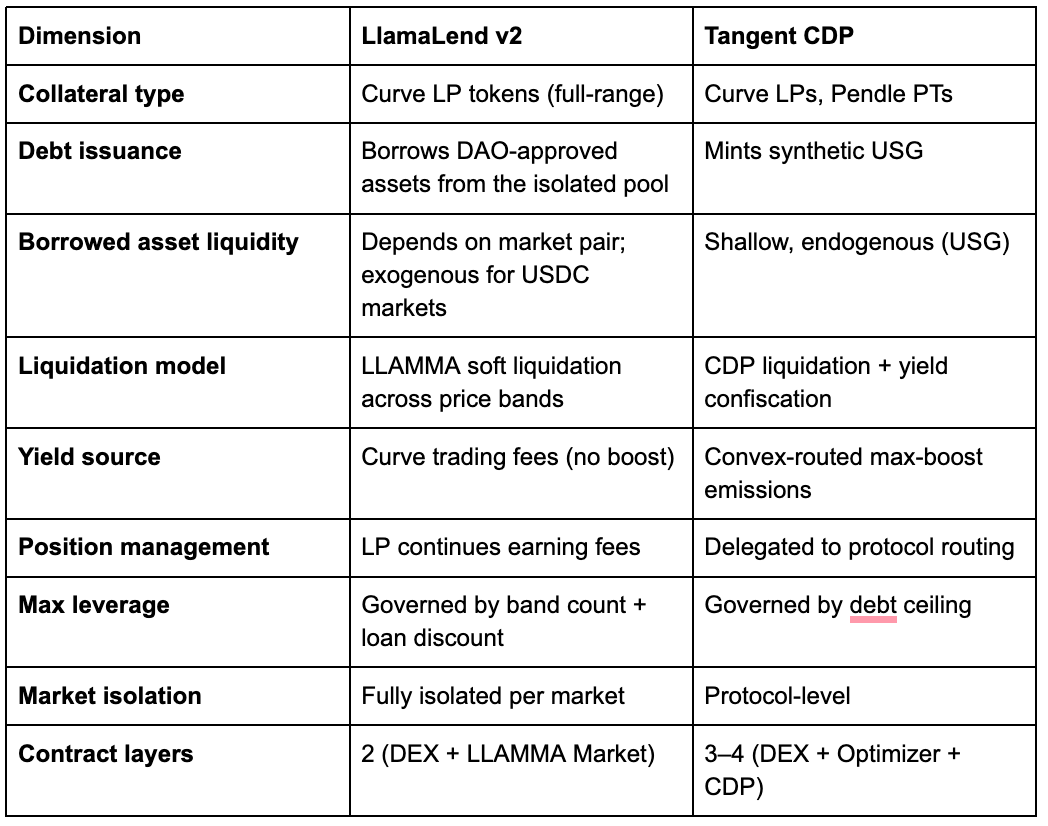

2. Protocol Architecture & Mechanics: The Multi-Layered Stack

The mechanics of stablecoin LP leverage rely on layering different decentralized protocols on top of each other. Each layer serves a specific role in generating yield or facilitating credit. The three protocols in this guide represent three architecturally distinct approaches: peer-to-pool lending with range-based soft liquidation against Curve LPs (LlamaLend v2), and CDP-based synthetic stablecoin minting against Curve LPs (Tangent).

2.2 Curve LlamaLend v2: The Soft-Liquidation Lending Stack

LlamaLend v2 — launched June 10, 2026 — extends Curve’s lending infrastructure beyond crvUSD-only borrowing into a generalized framework of isolated lending markets. Its defining innovation is the LLAMMA (Lending-Liquidating AMM Algorithm) mechanism, which replaces fixed-price liquidation with range-based soft liquidation.

Layer 1: The Base DEX (Curve). Capital is deployed into a standard Curve pool (StableSwap or CryptoSwap). Unlike Revert’s concentrated v3 positions, Curve LP positions are full-range and do not require active tick management — they earn fees continuously regardless of price movement within the pool’s invariant.

Layer 2: The Lending Market (LlamaLend Isolated Market). LlamaLend v2 accepts Curve LP tokens as collateral while the position continues to earn trading fees. Each lending market is fully isolated — it carries its own collateral asset, borrowed asset, oracle configuration, borrow caps, and risk parameters. LlamaRisk serves as market curator, reviewing proposed markets and calibrating risk parameters including the band width factor (A), LLAMMA swap fee, loan discount (which determines maximum LTV), liquidation discount, and min/max borrow rates.

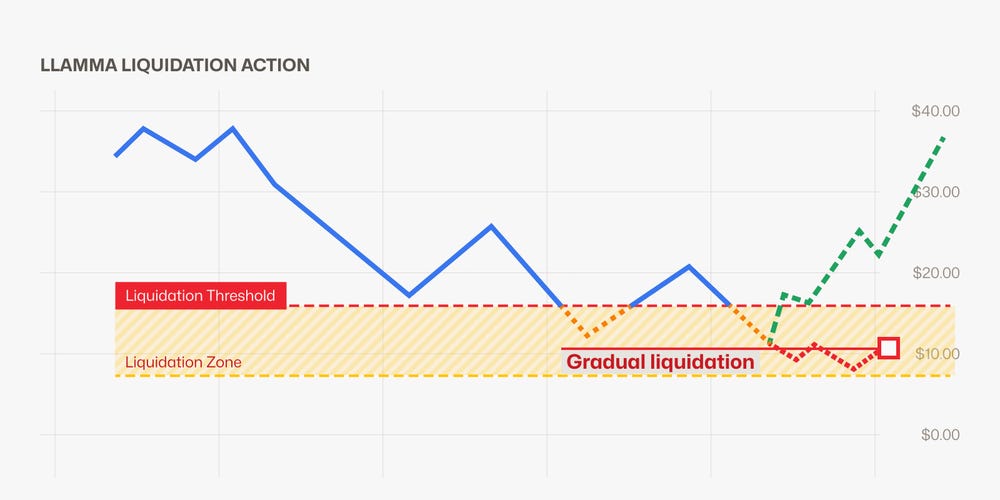

The LLAMMA Soft Liquidation. This is LlamaLend’s core differentiator. When a position’s collateral value enters the borrower’s liquidation range, rather than triggering a single catastrophic liquidation event, LLAMMA gradually converts collateral into the borrowed asset across multiple price bands. The borrower selects how many bands (4 to 50) to spread their collateral across when opening a loan — more bands means a wider liquidation range with more gradual conversion, but lower maximum LTV. If the price recovers above the liquidation range, the system reverses the conversion (de-liquidation), potentially allowing near-full recovery. This stands in stark contrast to traditional DeFi liquidation, where a position is closed at a fixed threshold with immediate loss.

The Leverage Loop. The borrowed asset (which can now be USDC, WETH, or other DAO-approved assets — no longer restricted to crvUSD) is swapped for the underlying LP components, redeposited into the Curve pool, and the resulting LP tokens are supplied as additional collateral.

2.3 Tangent Finance: The Integrated CDP Stack (Higher Risk)

Tangent is a decentralized Collateralized Debt Position (CDP) protocol that operates as an overarching asset controller, holding collateral and issuing debt directly under one roof.

Layer 1: The Base Yield Generator (Curve/Pendle). The foundation is built on organic yield-generating components, such as Curve stablecoin pools or Pendle Principal Tokens (PTs).

Layer 2: The Automated Yield Router (Convex/StakeDAO). Tangent’s smart contracts automatically route the deposited collateral “under the hood” into protocols like Convex to capture max-boosted rewards without requiring manual orchestration.

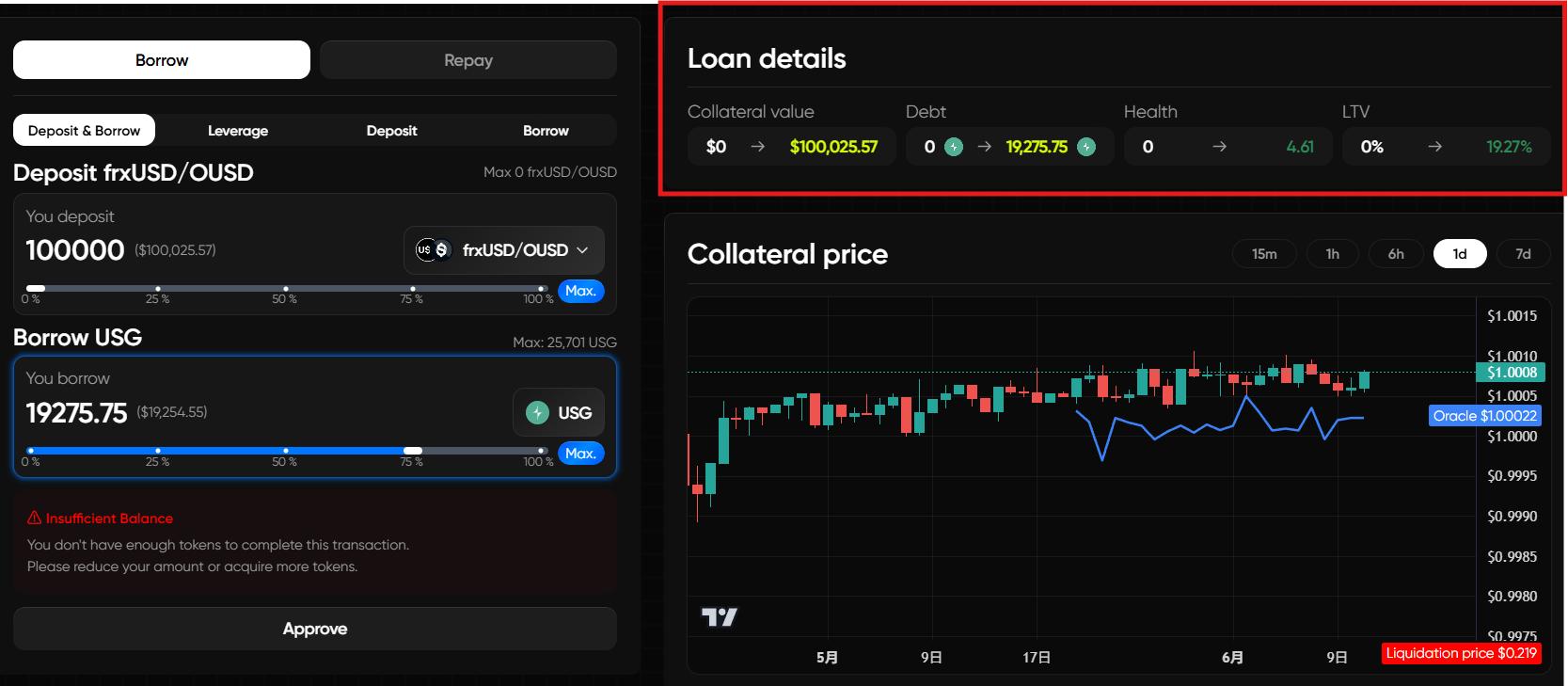

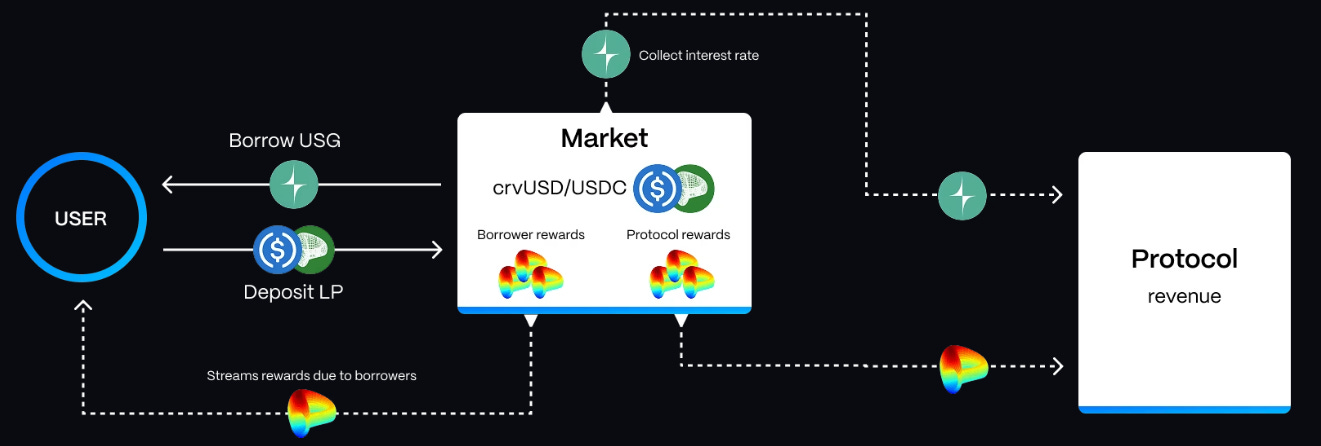

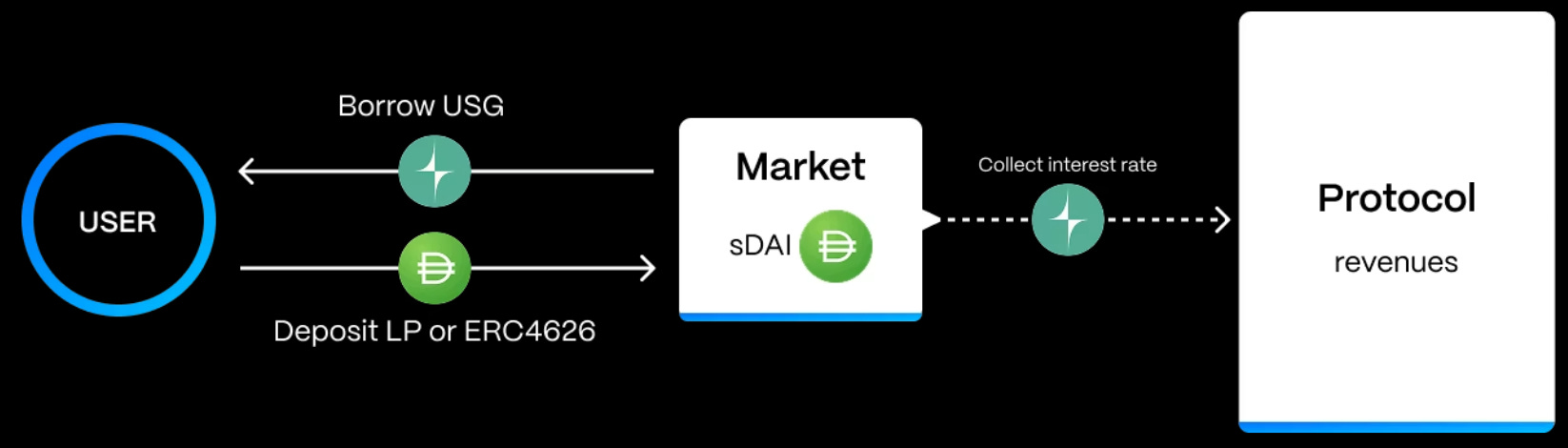

Layer 3: The Debt Issuer (Tangent CDP). Instead of borrowing from a pool of depositors, users lock their yield-bearing LPs into Tangent to mint its native, over-collateralized stablecoin, USG.

The Leverage Loop. USG is minted, swapped for base stablecoins (USDC/USDT) on a decentralized exchange, redeposited into the underlying LP, and the loop repeats.

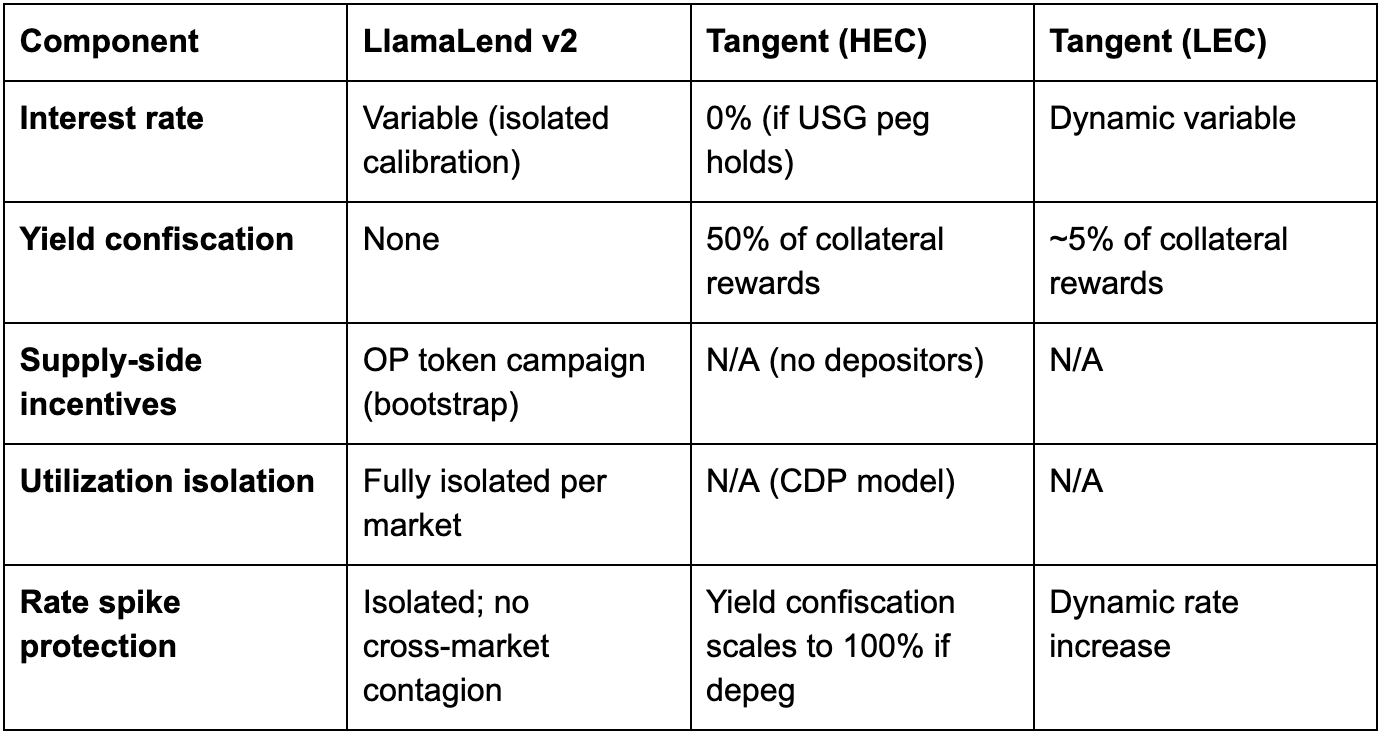

3. Borrowing Cost Frameworks

The structural divergence between the three protocols results in fundamentally different cost structures and protocol interventions for leverage.

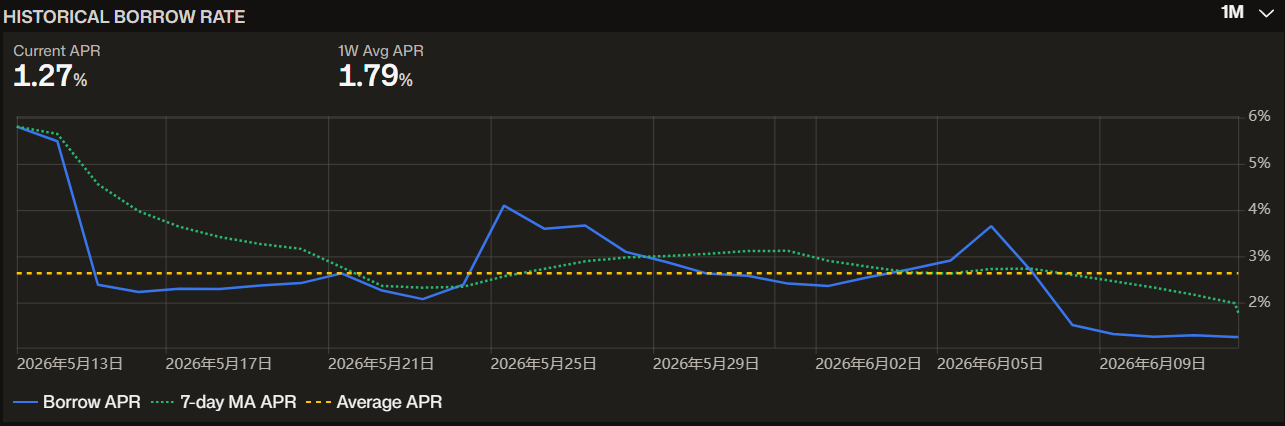

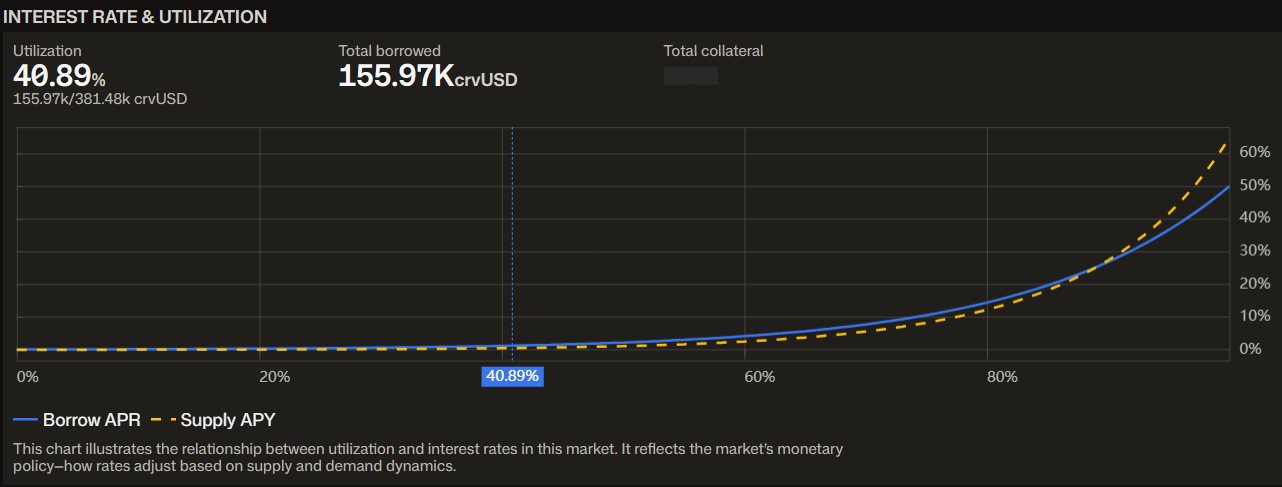

LlamaLend v2: Utilization-Driven Interest with Isolated Calibration

Each LlamaLend v2 market has independently configured minimum and maximum borrow rates. The min rate applies at zero utilization; the max rate at 100% utilization. Most markets target approximately 80% utilization. Rates are bounded by system constants (1% floor, 1000% ceiling) and calibrated by LlamaRisk on a per-market basis depending on collateral characteristics and risk profile.

Because markets are fully isolated, a utilization spike in one market (e.g., WBTC ↔ USDC) has no effect on borrowing costs in another (e.g., ETH ↔ wstETH). This isolation prevents the systemic liquidity crunches that can occur in unified lending pools, where a surge in borrow demand for one asset drives up rates for all borrowers.

Tangent: Yield-Deduction and Policy-Driven Costs

Because Tangent mints its own stablecoin rather than borrowing from depositors, it does not pay suppliers interest or need to incentivize supply-side liquidity in a traditional money market. Instead, costs are defined by internal monetary policies divided into two collateral models:

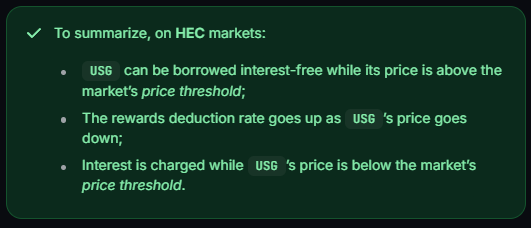

HEC (High Emission Collateral): Used for high-yield assets like Curve LPs. Borrowing features a 0% interest rate as long as USG holds its peg. In lieu of interest, Tangent extracts a flat 50% of the collateral’s generated rewards as a continuous fee.

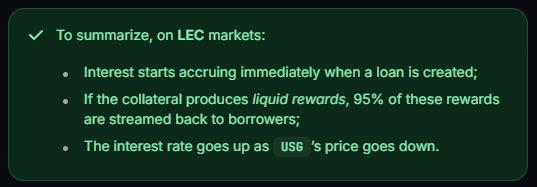

LEC (Low Emission Collateral): Used for lower-reward, highly predictable assets like Pendle PTs. The borrower retains 95% of the yield, but pays a traditional dynamically adjusted variable interest rate from day one.

4. Execution Frictions & Capital Flow

The efficiency of establishing, maintaining, and unwinding a leveraged position depends heavily on the secondary market liquidity of the borrowed asset and the tooling available for atomic execution.

LlamaLend v2 Execution Efficiency: Low-to-moderate friction for USDC-denominated markets; higher for less liquid borrowed assets. The initial launch markets (wstETH, USDC, WBTC) all have deep external liquidity. LP collateral markets (when available) will require swapping borrowed assets back into Curve LP positions, where slippage depends on the underlying pool’s depth and balance. The soft liquidation mechanism adds a unique execution consideration: during adverse price movement, the LLAMMA is actively converting collateral, and attempting to manually unwind during this process requires careful coordination.

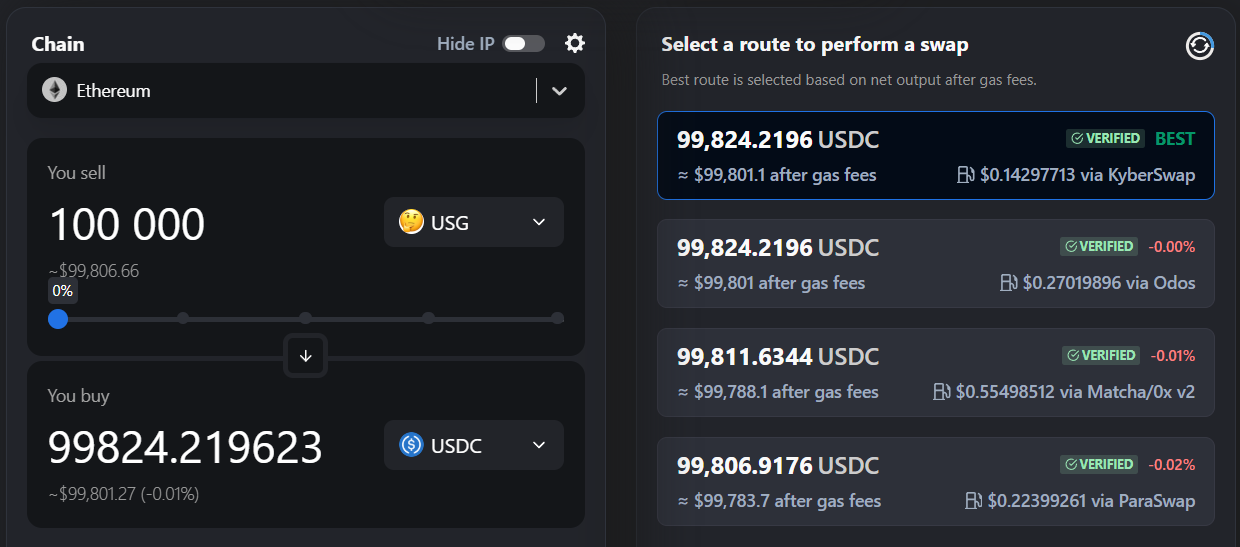

Tangent Execution Efficiency: High friction dependency. Execution efficiency is entirely bottlenecked by the secondary market depth of the USG stablecoin. If the USG/USDC pool is shallow, swapping minted USG to continue the loop incurs high slippage, directly degrading the net ROI of the leverage strategy.

The Drag on Capital Efficiency (Tangent vs. Hard Stables)

This execution friction gap is the single most quantifiable difference between the CDP approach and lending-market approaches. Because USG suffers from shallower market depth and slight peg deviations, a leverage loop swapping USG for underlying LP components acquires fewer LP tokens per unit of nominal debt than an identical swap using USDC or other hard stables. On a $10,000 principal margin, this can create an immediate ~0.75% to 0.90% drawdown before any yield begins accruing — a direct tax on capital efficiency that compounds with each loop iteration.

5. Risk Profiles & Vulnerabilities

The architectural design differences introduce entirely separate risk vectors for portfolio management.

5.2 Soft Liquidation Loss (LlamaLend v2)

LLAMMA’s soft liquidation is designed to protect borrowers from catastrophic cliff-edge liquidation events. However, it introduces its own form of loss that must be explicitly accounted for in leveraged position management.

How Losses Accrue. When a position’s collateral enters the soft-liquidation range, LLAMMA begins gradually converting collateral into the borrowed asset via its internal AMM. This conversion is not free — it involves trading friction within the LLAMMA bands. Critically, losses occur in both directions: when price decreases (collateral is sold for the borrowed asset) and again when price recovers (the borrowed asset is bought back for collateral). These round-trip losses are difficult to quantify precisely because they depend on the speed and magnitude of price movement, the number of bands, and external arbitrage activity.

The Leverage Amplification. At leverage, soft liquidation losses are magnified. A position that oscillates in and out of the liquidation range — common during periods of moderate volatility — accumulates compounding round-trip losses while simultaneously accruing borrow interest. Unlike Revert’s range risk (where the loss is pure opportunity cost of zero fees), LlamaLend’s soft liquidation range imposes active capital erosion on the collateral value itself.

5.3 Interest Rate Volatility (LlamaLend v2)

For both peer-to-pool lending protocols, the primary systemic risk lies in liquidity crunches within money markets. If borrow demand severely outpaces supply, the borrow rate will spike. This can result in negative carry, where the cost of debt exceeds the LP yield, bleeding capital unless the position is actively deleveraged.

LlamaLend v2’s market isolation provides structural protection against cross-market contagion — a spike in one market does not propagate. Revert’s single-vault-per-chain design means all borrowers on a given chain share the same utilization curve, creating potential for correlated rate spikes during periods of high leverage demand.

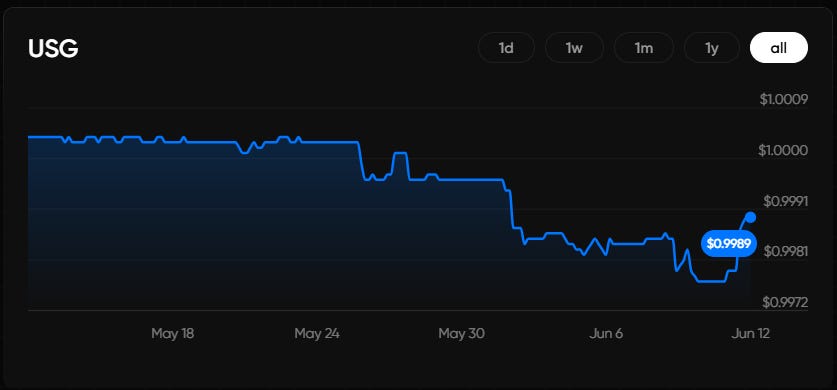

5.4 Peg Dependency & Reserve Architecture (USG vs. Hard Stables)

Tangent debt positions are structurally shorting USG, making the protocol’s underlying reserve design a critical risk vector — especially when compared to the established stablecoins borrowed on Revert and LlamaLend.

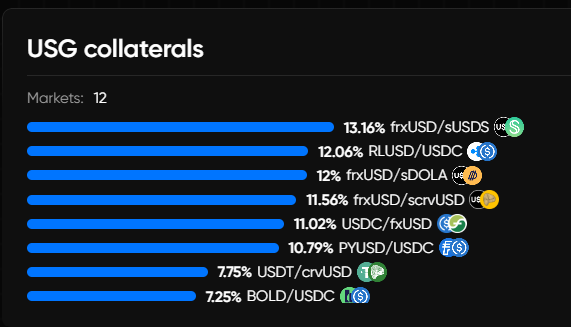

The USG Model: USG’s reserve design is endogenous. It is backed primarily by DeFi-native productive assets (stablecoin LPs and Pendle PTs). Furthermore, to bootstrap market depth, Tangent relies on self-minted, protocol-owned USG supplied directly into AMM liquidity pools.

Systemic Fragility: USG’s peg stability is entirely dependent on a complex equilibrium: the underlying quality of the collateral, the efficiency of liquidation mechanics during market downturns, the size and asset ratio of its Peg Keeper pools, and the precise management of protocol-owned liquidity.

Yield Confiscation Penalty: If these mechanisms falter and USG trades below its $1.00 peg, Tangent initiates aggressive monetary contraction. Under the HEC model, the protocol’s defense mechanism can scale up to confiscate up to 100% of the collateral’s yield to buy back and burn USG, while simultaneously applying a dynamic interest rate to force debt repayment.

5.5 Smart Contract & Operational Security

Each protocol carries a distinct security profile:

LlamaLend v2: Inherits Curve’s battle-tested LLAMMA contracts from v1, which have been in production since early 2024. However, the sDOLA/crvUSD market exploit (March 2026, ~$240K in borrower losses from forced hard liquidations via oracle manipulation) demonstrated that collateral-specific oracle design is a critical vulnerability surface — the root cause was improper oracle configuration by the pool creator, not a core protocol flaw. LlamaLend v2 addresses this through mandatory LlamaRisk review of all market parameters before governance approval. Curve’s broader security history includes the $70M Vyper compiler exploit (July 2023), which was a language-level vulnerability, not a Curve-specific logic flaw.

Tangent: The most complex contract stack — positions are simultaneously exposed to the underlying DEX, the yield optimizer (Convex), and Tangent’s own CDP architecture. This three-to-four-layer depth presents the widest attack surface. Any vulnerability in any layer can propagate to the leveraged position.

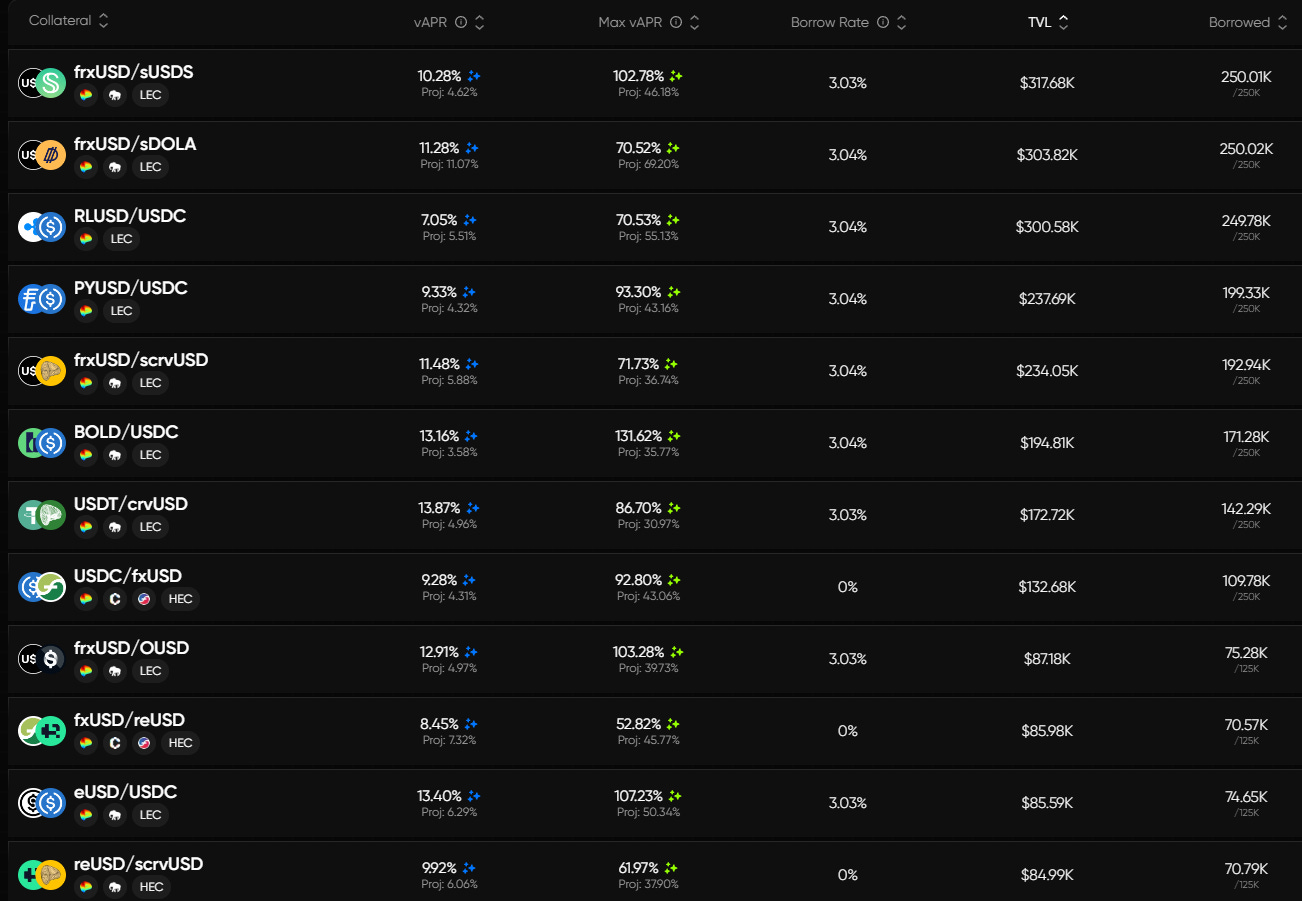

6. Example of Farming Opportunities

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.