Breaking: Bailout for Aave, How Saturn and Apyx Unlock 12%+ Yield

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

🚨Breaking News:

DeFi Industry Unites to Bail Out Aave

April 24, 2026 — Aave, Lido, EtherFi, Mantle and others coordinate crypto’s first industry-wide bailout as $13B flees DeFi.

Read the full news on our website

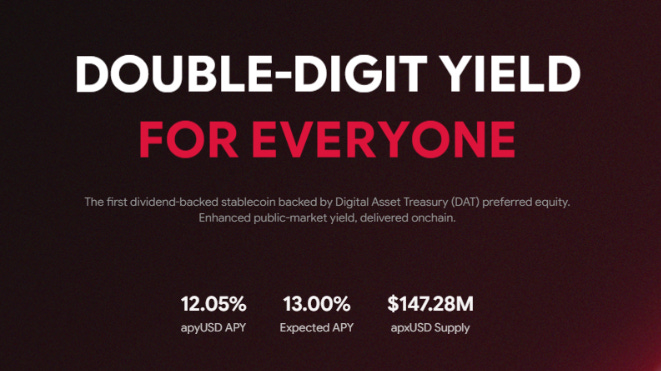

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

The decentralized finance landscape has historically relied on cyclical yield sources—primarily inflationary protocol emissions, funding rate arbitrage, and on-chain basis trading. As capital pivots toward RWAs for sustainable returns, the sector has encountered a structural dichotomy.

Tokenized U.S. Treasuries offer high liquidity and absolute transparency, yet their yields consistently underperform the DeFi average. Conversely, tokenized private credit delivers superior yields but introduces severe illiquidity, opaque risk profiles, and elevated default probabilities.

The introduction of protocols like Saturn and Apyx establishes a distinct asset class that strikes a balance between these extremes: Bitcoin-Backed Corporate Credit. By tokenizing preferred equity and digital credit instruments issued by off-chain entities—specifically Digital Asset Treasuries (DATs)—these protocols channel sustainable, fiat-denominated dividend cash flows directly into DeFi.

Because the underlying corporate debt is collateralized by Bitcoin, which is liquid and verifiable in real-time, this architecture mitigates the opacity and default risk of traditional private credit while sustaining double-digit, institutional-grade yields that operate independently of on-chain leverage cycles.

The Underlying Engine: STRC Mechanics & Risk Profile

To understand the sustainability of the double-digit yields offered by Saturn and Apyx, it is necessary to examine the foundational collateral asset: STRC. While protocols maintain minor allocations to alternative digital assets (like SATA, which serves as a marginal diversification instrument within Apyx’s treasury), STRC is the dominant yield engine powering these ecosystems.

STRC Structure and Mechanics

STRC functions as the first short-term, high-yield credit instrument built directly on a Bitcoin standard. Issued by “Strategy”—the largest corporate holder of Bitcoin—STRC is structured as perpetual preferred equity rather than traditional corporate debt.

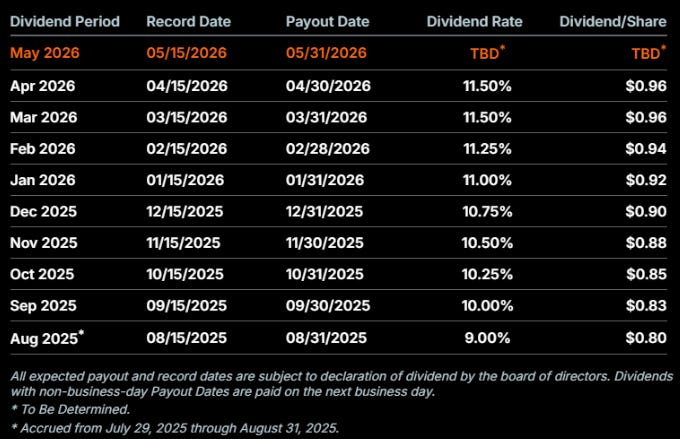

Dividend Rate & Adjustments: STRC pays a variable monthly dividend benchmarked against the one-month SOFR rate and the 30-day Volume-Weighted Average Price (VWAP) of the STRC asset itself. To keep the instrument trading near its $100 par value, the issuer utilizes a dynamic dividend adjustment matrix:

If VWAP < $95: Dividend increases by 50 bps or more.

If VWAP $95 – $98.99: Dividend increases by 25 bps or more.

If VWAP $99 – $100.99: Discretionary ±25 bps adjustment.

If VWAP ≥ $101: Dividend decreases by 25 bps or more.

Liquidation Preference: The instrument carries a liquidation preference of $100 per share plus any accrued and unpaid dividends, providing downside structural protection in the event of issuer liquidation.

SATA (Strategic Asset Allocation): In contrast to STRC, assets like SATA (which comprises ~3.97% of Apyx’s treasury) are utilized as secondary strategic holding instruments. While details are less standardized than STRC, they serve to slightly diversify the protocol’s digital credit exposure away from a single issuer.

⚠️Risks Associated with STRC (The Underlying Asset)

While STRC mitigates many of the opacity issues of traditional private credit, the architecture introduces severe, specific risk vectors that extend beyond the underlying asset and into the wrapper protocols (Saturn and Apyx) themselves. Market participants must underwrite the following:

Bitcoin Performance and Principal Loss: The underlying corporate issuer (Strategy) relies heavily on a balance sheet concentrated in Bitcoin. Because Bitcoin does not naturally generate a yield, the issuer depends on Bitcoin’s price appreciation and treasury maneuvering to fund STRC’s double-digit dividends.

The “Flat Market” Risk: Even if Bitcoin doesn’t crash, a prolonged period of flat price action will inevitably bleed the treasury. Without price appreciation, dividend payouts become unsustainable, leading to severe yield impairment.

The Drawdown Risk: A severe macroeconomic drawdown in Bitcoin’s price would aggressively deteriorate the issuer’s collateralization. Simply put: if the corporate treasury is depleted, they will not be able to return your initial $100 per share investment. You could lose some or all of your principal.

Interest Rate (SOFR) Exposure: Because the STRC dividend rate is benchmarked against SOFR, a macro environment involving aggressive central bank rate cuts would compress the baseline yield of STRC, subsequently dragging down the floating APY of sUSDat and apyUSD.

Secondary Market Liquidity for STRC: While the instrument aims to maintain a $100 par value, it is traded on secondary markets (like the Nasdaq). During periods of extreme macroeconomic stress or institutional panic, buyers for STRC could disappear. This lack of liquidity would cause the asset to trade at a steep discount to its par value, meaning anyone forced to sell during this window would realize a loss.

Protocol Mechanics & Collateral Architecture: The Dual-Token Model

Both Saturn and Apyx utilize a bifurcated token model to solve the fundamental tension between liquidity provision and yield accrual. By separating the monetary layer from the yield layer, the base stablecoin can achieve deeper integration across centralized and decentralized venues, while the yield-bearing variant functions as an efficient value-accrual vault. Their respective yield profiles are directly derived from how they structure the underlying collateral for these two layers.

Saturn: Dynamic Compartmentalization

Saturn bridges the emerging Bitcoin credit market into a composable DeFi format, employing a strict compartmentalization of its collateral to manage the distinct objectives of its two tokens.

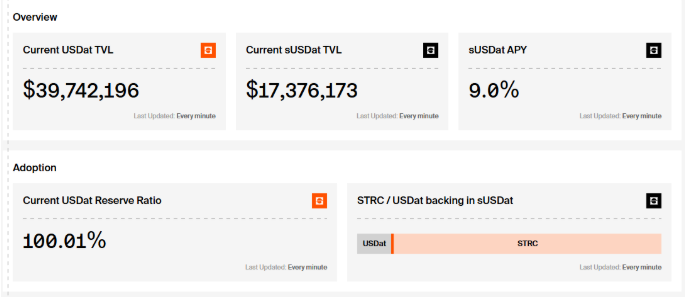

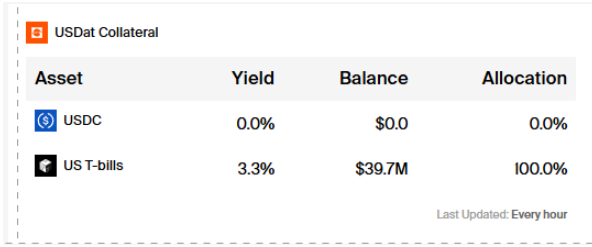

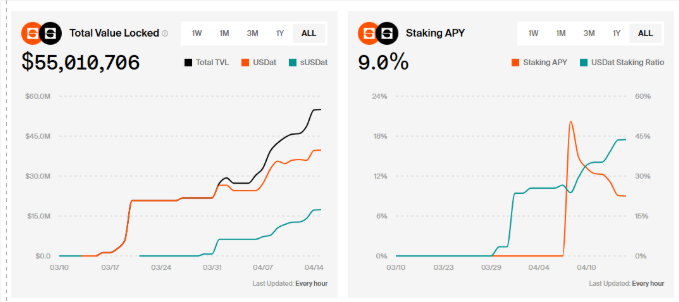

The Monetary Base (USDat): Designed strictly for settlement and liquidity, USDat is minted at a 1:1 ratio. To maximize stability and insulate the primary settlement layer from credit market volatility, the USDat reserve ($39.6M) is currently allocated 100.0% to US T-bills, which generate a conservative baseline yield of 3.3%.

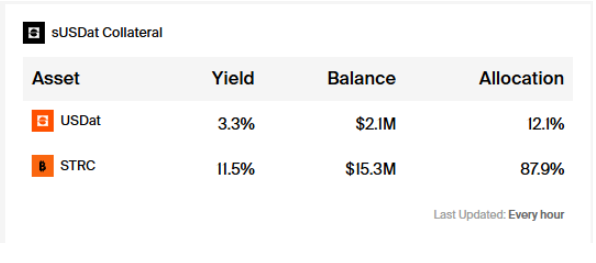

The Yield Vault (sUSDat): When USDat is staked, users receive sUSDat, an ERC-4626 standard yield-bearing vault token. The underlying collateral is reallocated into STRC—a perpetual preferred equity instrument collateralized by corporate Bitcoin balance sheets. To optimize returns while maintaining operational liquidity, the sUSDat vault ($17.3M total) utilizes a blended allocation:

88.5% STRC ($15.3M): The core yield engine, capturing the 11.5% dividend rate generated by the Bitcoin-backed corporate credit.

11.5% USDat ($2.0M): A cash-equivalent buffer (yielding 3.3%) to service standard unstaking requests without forcing the premature sale of the underlying STRC on secondary markets.

Mechanic: As STRC dividends accrue, they are captured within the vault, steadily increasing the sUSDat-to-USDat exchange rate without the need for manual compounding.

Apyx: High-Conviction Credit Exposure

Apyx operates as a dividend-backed stablecoin protocol designed to route off-chain digital credit yields on-chain. It demonstrates a more aggressive, concentrated exposure to the digital credit sector to maximize the yield passed through to its users.

The Liquidity Layer (apxUSD): A synthetic dollar functioning as the primary liquidity layer. It is backed by preferred shares issued by DATs, but the token itself does not accrue yield. This non-rebasing structure ensures frictionless integration into AMMs and lending protocols.

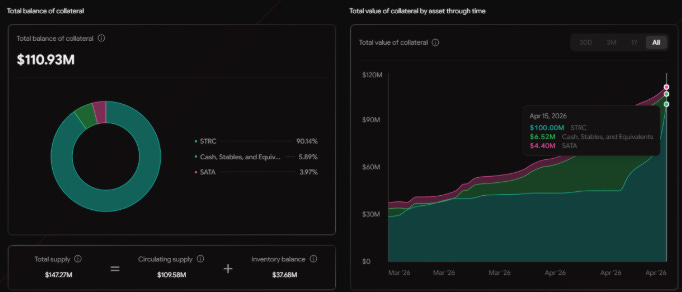

The Yield Layer (apyUSD) & Treasury Composition: Market participants holding apyUSD capture the dividend streams generated by the underlying DAT shares, with apyUSD systematically appreciating against apxUSD as off-chain cash flows are realized. To fuel this, Apyx maintains a highly concentrated treasury. Current data shows a total collateral balance of $110.93M against a circulating supply of $109.58M (approx. 101.2% overcollateralization), composed of:

90.14% STRC: The vast majority of the treasury is deployed directly into the primary digital credit instrument, maximizing dividend cash flows.

5.89% Cash, Stables, and Equivalents: A necessary but minimized liquidity buffer used to facilitate standard redemption and swap mechanics.

3.97% SATA: A minor allocation to an alternative strategic asset, providing slight diversification within the broader digital asset treasury framework.

Comparative Yield Profile & Ex-Dividend Mechanics

Both protocols effectively solve the “RWA Yield Divide” by utilizing STRC as a highly verifiable, Bitcoin-collateralized middle ground. However, their structural differences result in distinct behaviors during dividend cycles:

Saturn’s Volatility Pass-Through: Because sUSDat is directly backed by its proportional share of USDat and STRC, its NAV is sensitive to STRC’s secondary market behavior. After a dividend record date, STRC often trades below its $100 par value and can take several days to recover. This temporary ex-dividend discount directly impacts the sUSDat vault valuation, causing short-term pricing volatility for sUSDat holders.

Apyx’s Overcollateralization Buffer: Apyx’s treasury model fundamentally insulates apyUSD from this specific mechanic. Because the protocol is systematically overcollateralized ($110.93M in assets vs. $109.58M in circulating supply), the short-term STRC discount following a record date is absorbed by the protocol’s equity buffer. As long as the treasury remains overcollateralized, the apyUSD price remains unaffected by STRC’s temporary ex-dividend dips.

Current Yield Opportunities

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.