Capital Rotating Back To DeFi, Base Overtaking BSC - Weekly Onchain Outlook

Subscribe for daily free DeFi news, outlooks, airdrops, and actionable farming opportunities.

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

In this letter, we bring you the best bottom-up analysis of onchain trends, along with top-down market analysis, helping you find top yield opportunities and position for trends before they happen

1. Upcoming DeFi Events and Catalysts

2. Stablecoin Flows

4. Chain Comparison

5. DeFi Token Movers

6. TVL Gainers + Interesting Protocols Worth Farming

Today’s News Headline:

- Anthropic warned pre-IPO trades might be scams.

- CoW DAO approves DNS hijack reimbursements

- Circle unveils ARC Layer-1 tokenomics

- Royco Dawn opens sNUSD tranche vaults

- Strategy buys additional 535 ($43M) Bitcoin

- Sushi launches Hyperliquid-powered Perps v2

- Resolv finalizes recovery agreement with Fluid

- Stream Finance provides update on reimbursement process

- US court approves Arbitrum ETH transfer

- 21Shares launches Hyperliquid ETF THYP

Outlook Key Takeaways

DeFi capital is rotating back, USDC's reversal is the supporting evidence.

After three straight weeks of contraction, USDC swung +$1.6B this week — the single biggest weekly inflow of 2026. The broader read isn't about USDC itself, it's about DeFi-native capital flowing back into deployable, dollar-denominated liquidity for stablecoin yield, curated lending, and onchain activity.Ethena is recovering from the Kelp shock.

After USDe lost a third of its supply (-$1.59B, -32%) as the Aave WETH freeze forced leveraged USDe positions to unwind. This week confirms the recovery is complete: USDe supply is back to ~$3.96B after three straight weeks of inflows (+$151M, +$151M, +$62M), and ENA token rallied +30% this week.Lending liquidity continues migrating away from Aave to Morpho and Euler.

Most new DeFi TVL this week flowed into Morpho curators, Euler vaults, and isolated lending structures like Steakhouse, RockawayX, and Sentora. Capital is increasingly favoring curated risk-managed vaults over traditional pooled lending markets.

1. Upcoming DeFi Events and Catalysts

DeFi Catalysts & Launches for the Week Ahead (May 12–18, 2026)Here’s a fresh scan of upcoming DeFi-specific events, upgrades, DAO votes, and infrastructure moves for this week:

Starknet will launch strkBTC, a Bitcoin asset with built-in privacy features, on May 12.

Base network: Azul upgrade (first major independent upgrade) launches on May 13.

Balancer DAO: Voting ends May 12 on a one-time $500K USDC airdrop to veBAL holders.

Stable Network: v1.3.0 mainnet upgrade deploys on May 13 (focuses on safety and reliability).

Flare Networks: Community vote on revenue sharing and $FLR emissions scheduled for May 13 (direct DeFi yield implications).

Euphoria: Mainnet launch expected May 14 (DeFi-focused protocol).

Bitcoin Cash : “Layla” network upgrade on May 15 — adds full smart contract support, opening the door to new DeFi apps on the chain.

Token Unlocks

Avalanche (AVAX): ~$16.5M unlock on May 12.

Arbitrum (ARB): ~$13M unlock on May 16.

Starknet (STRK): Large unlock also on May 15 (adds to original Starknet item).

Events & Broader Catalysts

The macro week is dominated by the Trump-Xi summit in Beijing on May 14-15 — Trump's first visit to China since 2017, with the agenda covering trade, AI, export controls, Taiwan, and the Iran war.

Digital Assets Week USA (New York, May 13–14): Institutional-focused conference with heavy DeFi panels and potential yield/RWA announcements.

This week is lighter on brand-new product launches and heavier on upgrades, DAO governance, and token supply events.

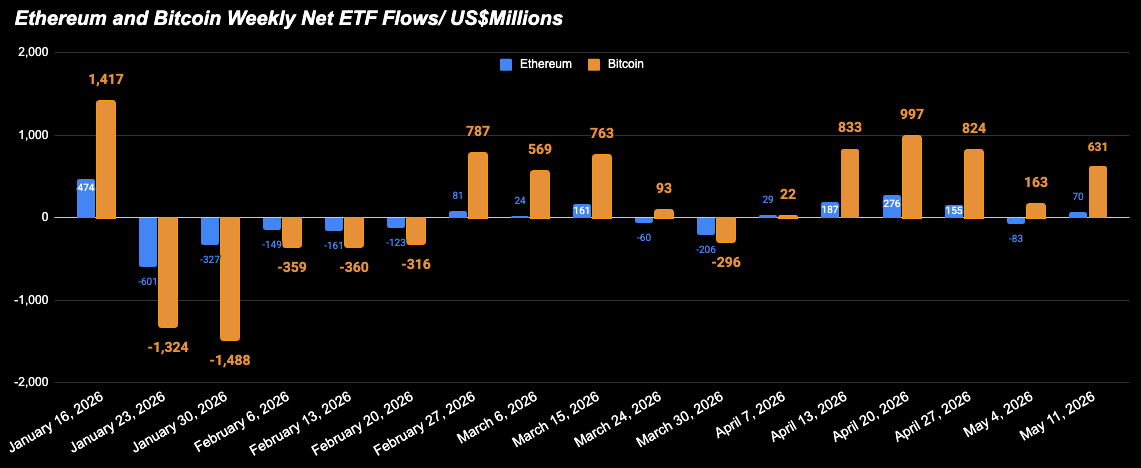

ETF Flows:

BTC ETFs recorded $631M inflows this week, the fifth consecutive week of net inflows — and ETH ETFs flipped positive at +$70M after going negative last week. Combined ~$701M vs $80M last week is a meaningful recovery in the institutional bid. Sources: Yahoo Finance, Spotted Crypto (May 5-11).

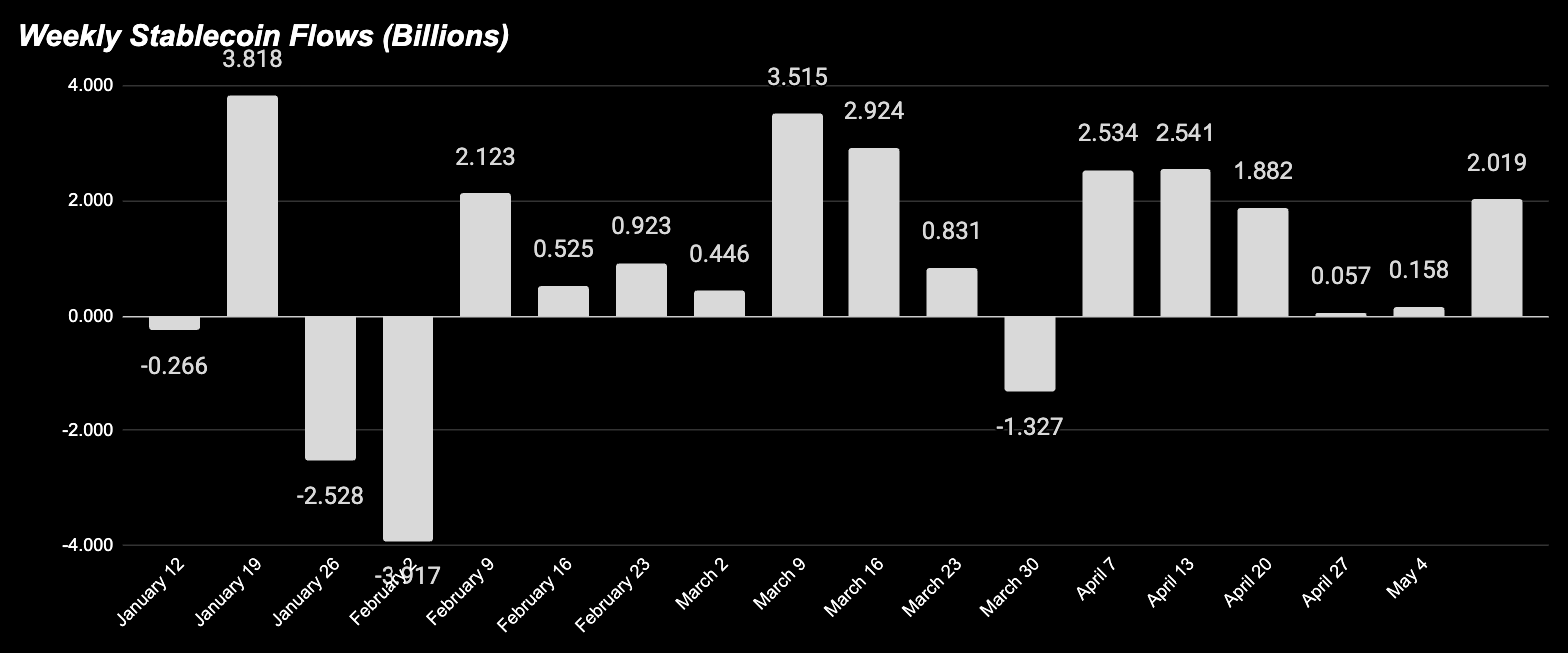

2. Stablecoin Flows

Weekly flow: +$2.019B (0.61%). A clean recovery from two weeks of near-zero growth (+$57M, +$158M). Net stablecoin demand is back, and the composition matters — capital didn’t flow into USDT for parking, it flowed into USDC for deployment.

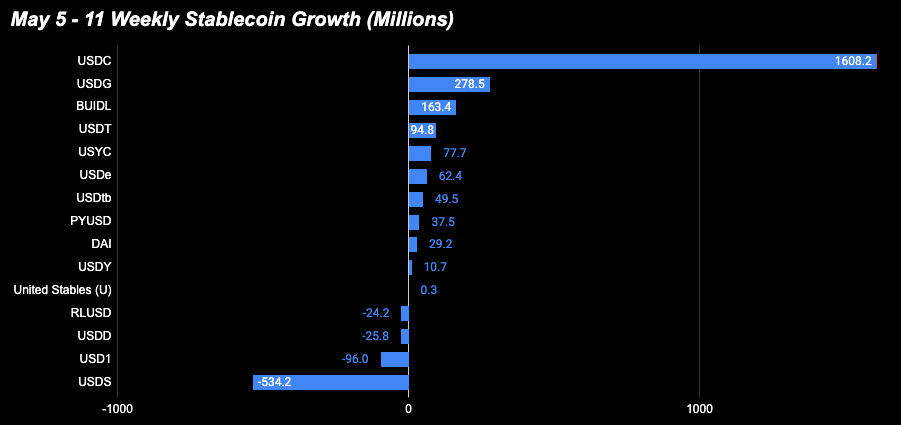

USDC +$1.608B (+2.08%) — the move of the week. After three straight weeks of contraction, USDC swung to the single biggest weekly inflow of 2026. The signal isn’t about USDC itself — it’s about what USDC enables. USDC is the dominant collateral and deployable asset across Ethereum DeFi: it gets supplied to Morpho/Euler vaults, used as borrow asset for ETH-collateralized loans, and routed into curated lending strategies.

A USDC inflow this size means deployable capital has returned On-Chsin. We flagged USDC last week as the marker to watch for broad recovery. It turned this week.

USDS -$534M (-6.37%) — biggest weekly loser, but for a different reason. USDS reversed from last week’s +$444M inflow with a sharp -6.37% drop in supply. The Sky Savings Rate sits at 3.75% (after the January Fed cut), while curated stablecoin vaults on Morpho and Euler are paying 5-6% with isolated risk. This looks like yield rotation, not loss of confidence — USDS holders are exiting toward higher-paying venues now that USDC is flowing back into DeFi.

USDe +$62M (+1.60%) — third straight week of stabilization. USDe supply is now back to ~$3.96B (after dropping to a multi-month low of $3.8B post-Kelp). The Ethena unwind is firmly over. ENA token rallied +30% this week as investor confidence in the basis trade returned. Watch for whether USDe growth accelerates as the MegaETH–Ethena flywheel continues — Ethena is one of the largest USDM suppliers on Aave MegaETH, so the loop directly impacts USDe supply.

Other movers (briefly): USDS -$534M and USD1 -$96M contracted as yield seekers rotated into higher-paying curated vaults. USDG +$278M, BUIDL +$163M, USDtb +$49M added to the regulated/RWA-backed tier (these are growing on institutional channels, less tradeable for retail). USDT +$94.8M was modest — not where the action was.

3. Chain Comparisons

Trend 1: Ethereum is healing — but the lending migration to alternative venues continues

Ethereum’s stablecoin supply stagnates since October Market peak. Stablecoin outflow slowed from -$1.58B last week to -$345M this week — a 78% reduction in outflow pace. Combined with USDC’s +$1.6B reversal (USDC is mostly on Ethereum), Ethereum DeFi liquidity is stabilizing.

Solana flipped positive (+$301M) after three straight weeks of outflows. The breakdown: USDC contributed +$600M (+7.63%) and USDG contributed +$133M (+20%) on Solana — signaling stablecoin farming incentives on Kamino, Loopscale(leverage Looping), and Jupiter are pulling capital onto the chain.

Stablecoin with structural RWA infrastructure are attracting concentrated capital:

Plume +$302M (+141% 7d) — the standout sustained-growth story. RWA-focused L1 with ~$645M tokenized assets and 280K+ holders. Ondo’s USDY deposits are scaling materially, plus partnerships with Apollo, WisdomTree, EY, and Securitize. Plume’s purpose-built RWA architecture (compliance, custody, distribution baked into the chain) is attracting issuers and capital that need regulated infrastructure. Sources: Messari, RWA.xyz.

Avalanche +$133M (+9.32%) — driven largely by RWA flows. BlackRock’s Securitize-tokenized BUIDL Fund continues to scale on Avalanche.

Arbitrum is the loser on this metric — bleeding -$203M (-5.30%) this week, and -8.9% over 30 days. Capital is rotating away from the leading L2 across every window.

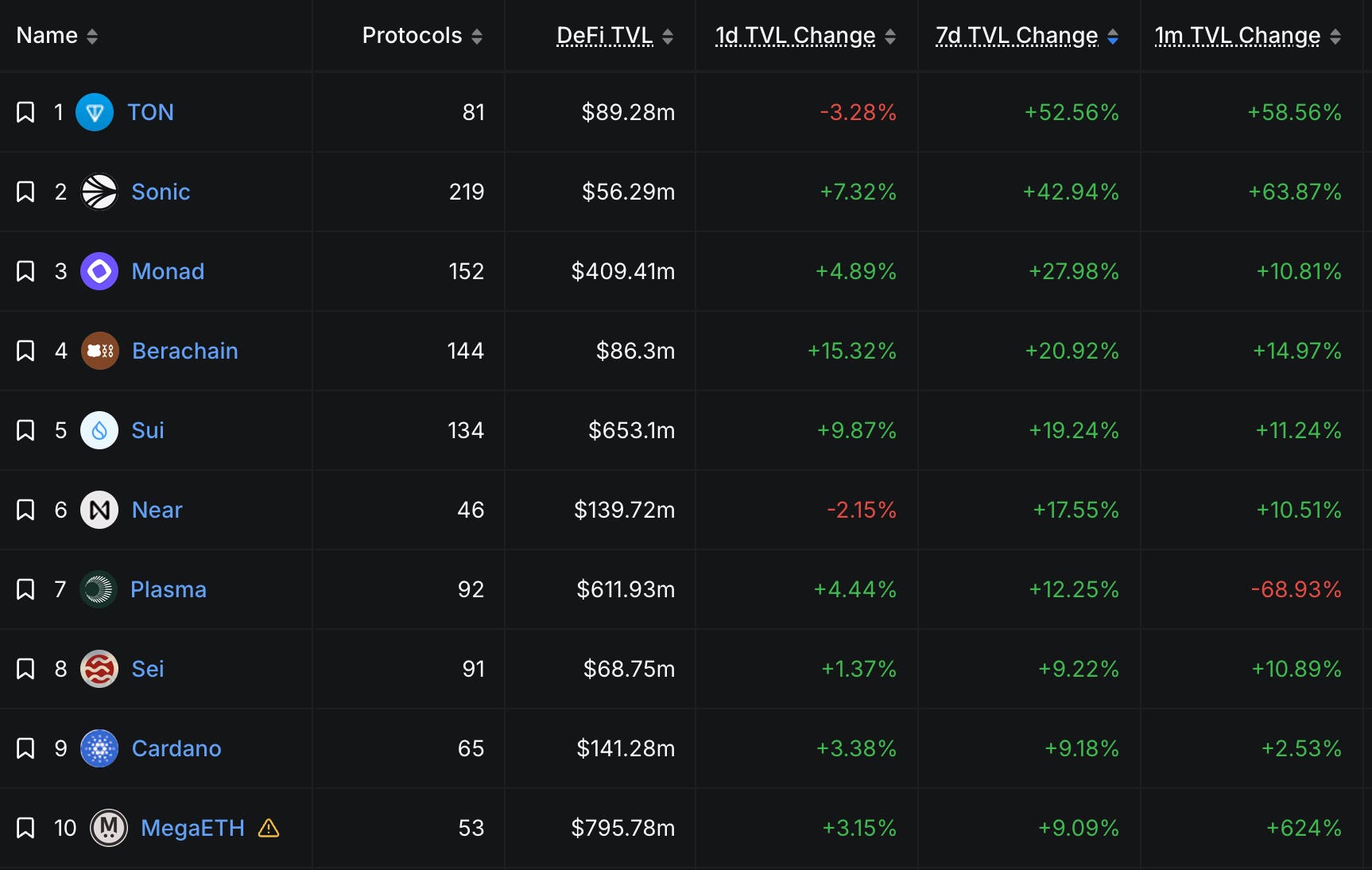

TVL Growth — Curated lending venues are the structural winner

The TVL leaderboard tells a different story from stablecoin flows. The chains showing the biggest TVL gains aren’t necessarily the same chains attracting stablecoin liquidity — TVL captures protocol-level deposits and is also sensitive to underlying token price moves:

Monad +22.75% 7d TVL — most of Monad’s stablecoin TVL is sitting in Morpho vaults curated by Sentora. That maps directly to the broader thesis we’ve been tracking: capital migrating into curated isolated lending venues. Monad has become one of the chains where that migration is happening at scale.

Sonic +40% 7d TVL — the driver is VGUSDC on Beets. VGUSDC is the receipt token for Varlamore Capital’s USDC Growth vault, which deposits into curated lending markets on Silo Finance. Beets (Sonic’s main DEX) integrates VGUSDC into boosted V3 liquidity pools where LPs stack vault lending yield, swap fees, Beets incentives, Sonic Points (10x multiplier for whitelisted yield-bearing stables), and additional yield layers. Real borrow demand on Silo + Beets composability.

Sui +20.98% 7d TVL reflects SUI price appreciation more than fundamental adoption. Worth flagging⚠️: Sui has seen 7 protocol exploits in the last month (Cetus -$223M, Nemo, Typus, Volo, Scallop, Aftermath Perps, and now DeepBook May 9). The pattern suggests a systemic security weakness at the network level that hasn’t yet been priced into chain token prices — but it should factor into any sizing decisions for Sui-based DeFi positions.

MegaETH +8.19% 7d TVL vs +618% 30d — the gap shows the inflow wave is mostly over. The Aavethena loop is still spinning (USDe cap raised again May 9, $400M → $800M proposed), but the marginal capital pace is slowing as supply caps fill faster than they can be raised.

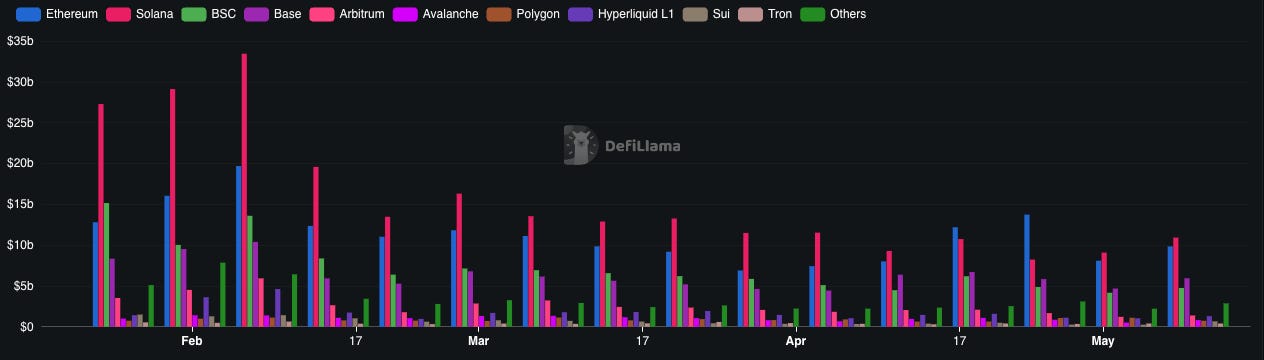

DEX Volumes: Base is structurally overtaking BSC

Looking at DEX volumes across the past 5 weeks (per DefiLlama), Base has consistently posted higher weekly DEX volumes than BSC. This week: Base $4.81B vs BSC $4.59B. The week before: similar relative positioning. The pattern has held for ~5 weeks straight.

This is a structural signal. BSC has been a top-3 chain by DEX activity for years on the back of retail trading and PancakeSwap. An L2 (Base) consistently outpacing BSC week-over-week suggests:

The Centrifuge tokenization partnership — Coinbase announced May 5 it had taken a strategic equity stake in Centrifuge and named it the default tokenization layer for assets on Base. First wave of institutional ETFs, credit products, and structured products launching on Base "in the coming weeks." The precedent already exists with deSPXA (compliant onchain S&P 500 fund).

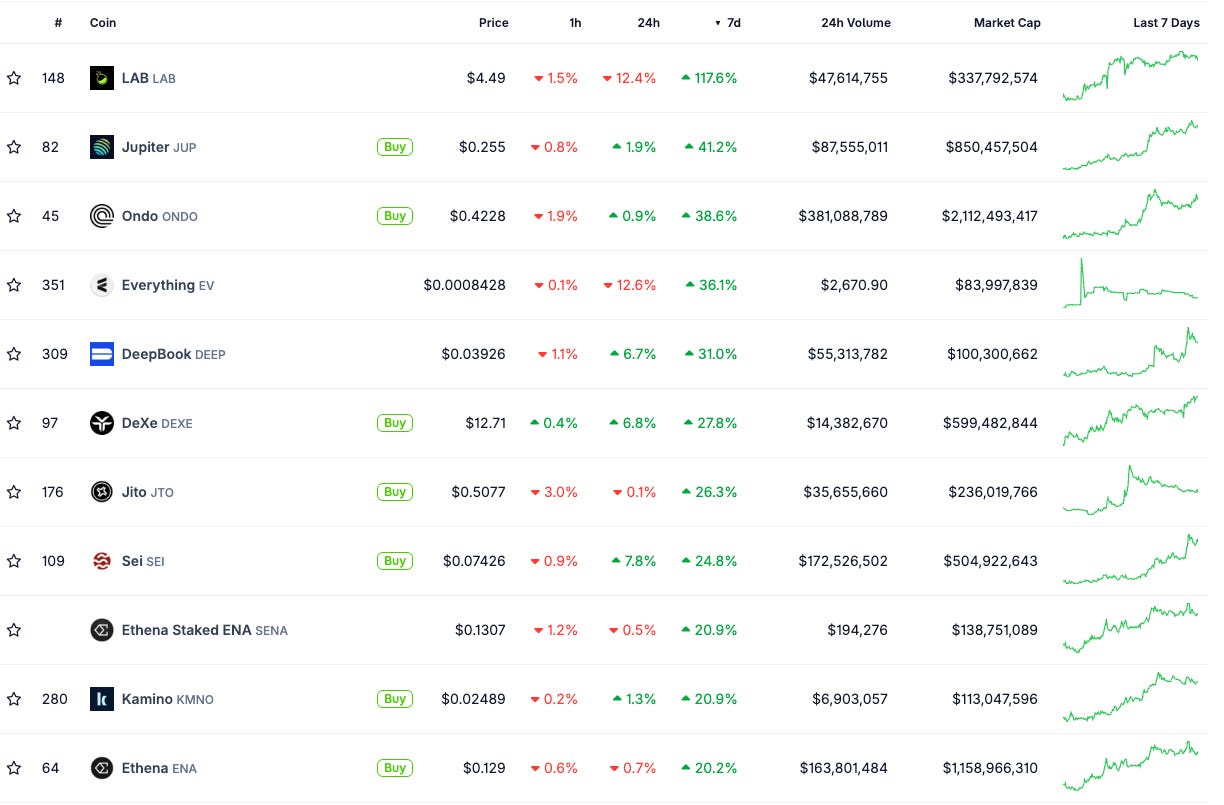

4. DeFi token price gainers & their catalysts

Context for the week’s moves — observations, not trade ideas. Many have already run.

$ONDO +38.6% — Follow-through from last week’s DTCC Industry Working Group selection. Additional catalysts this week: 260+ Ondo tokenized stocks and ETFs went live on KuCoin Web3 Wallet, and the Broadridge partnership brings proxy voting capabilities to tokenized stock holders. Ondo reports ~70% market share in tokenized stocks.

$JUP +41.2% — Securitize + Jump Trading + Jupiter announced May 5 the launch of fully regulated tokenized equities on Solana, positioning Jupiter as the distribution layer for institutional-grade onchain equity trading. Other Solana developments landed the same day: Anchorage Digital + JPMorgan announcement and Firedancer 1.0 milestone.

$DEEP (DeepBook) +31.0% — Notably, DeepBook itself was hacked on May 9 — an undercollateralization vulnerability resulted in $239,700 of bad debt in the USDC margin pool.

The DeepBook Insurance Fund absorbed the loss and trading resumed within hours. This was Sui’s 7th exploit in 12 months (after Cetus -$223M, Nemo, Typus, Volo, Scallop, Aftermath Perps).

Despite the hack, DEEP token outperforms after introducing Predict, a new financial primitive for building onchain options, binary markets, and structured products integrated with Spot and Margin. Predict is live on testnet, with mainnet launch planned soon.

$ENA +20.2% — Moving with the MegaETH–Ethena loop continuation. USDe supply caps on Aave MegaETH were raised again May 9 ($400M → $800M proposed), and ENA captures fees from both USDe issuance and the MEGA rewards paid for USDM supplying.

$JTO +28.8% — The catalyst continues from last week’s announcement on JTX, a self-custody trading app for Solana targeting serious traders, consolidating charts, execution, portfolio tracking, and capital management into a single interface. Key features include dependable on-chain limit orders and self-custody by default, with early access available at jtx.trade.

$SEI +28.0% — No specific catalyst identified beyond broader L1 narrative continuation. Market cap: $503M.

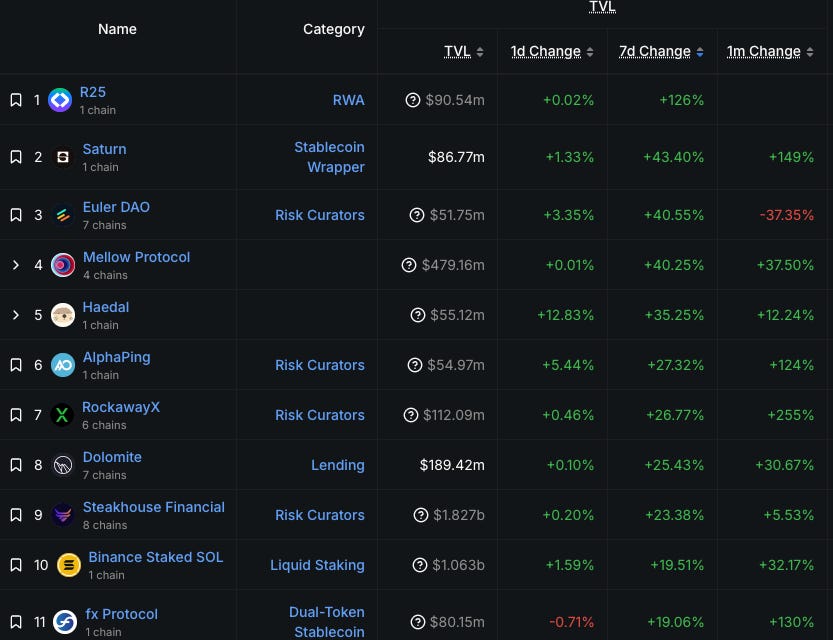

5. TVL gainers - for protocols above $100M

This week’s leaderboard has a concentration of Risk Curators (Steakhouse, RockawayX, AlphaPing, Euler DAO) and Onchain Capital Allocators (Mellow Protocol). Combined with USDC’s return to DeFi, the data suggests capital is rotating back into stablecoin yield through curated vault architecture rather than direct lending markets.

#1 Steakhouse Financial — $1.834B TVL, +$352M weekly (+23.82%, +5.91% monthly)

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.