Crypto Rallied Despite DeFi Stress, Capital Rotating To Proven Yields - Weekly Onchain Outlook

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

In this letter, we bring you the best bottom-up analysis of onchain trends, along with top-down market analysis, helping you find top yield opportunities and position for trends before they happen

1. Broader Market Outlook

2. Stablecoin flows per chain

3. Perps Volumes Analysis

4. DeFi token price gainers & their catalysts

5. TVL gainers - for protocols above $50M

Key Takeaways

1. The post-Kelp DeFi rotation is taking shape: clean-collateral protocols winning, affected protocols recovering.

Capital is rotating into protocols whose collateral isn’t tied to rsETH/Aave contagion — Spark, Re, Euler/Sentora’s clean vaults, Superstate, fx Protocol. Meanwhile, Aave’s “DeFi United” initiative has raised ~$305M of the ~$230M needed to backstop the rsETH bad debt.

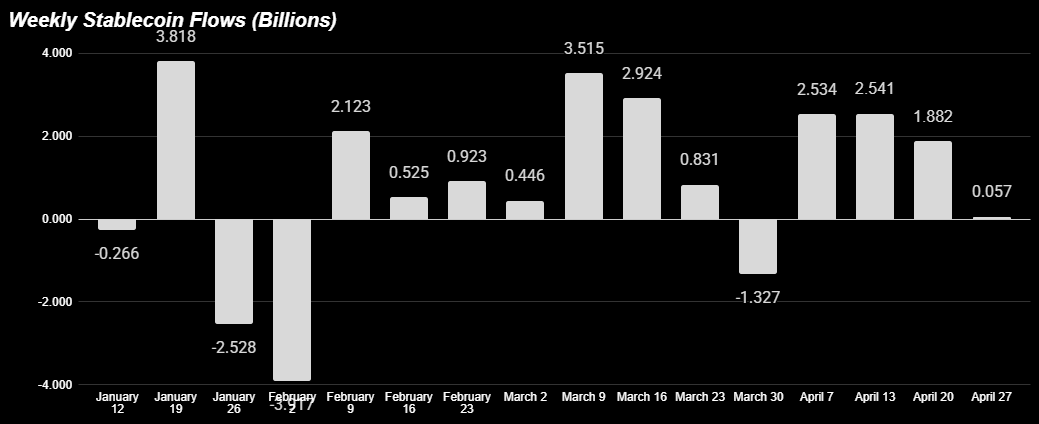

2. Stablecoin rotation has a mixed signal, risk-on for crypto prices, but people are leaving DeFi

Flows nearly stopped at +$57M (+0.02%), lowest since February. USDT absorbed +$2.53B (risk-on for trading and CEX activity), but USDC contracted -$407M and has stopped growing since the Resolv hack — capital is pulling out of DeFi.

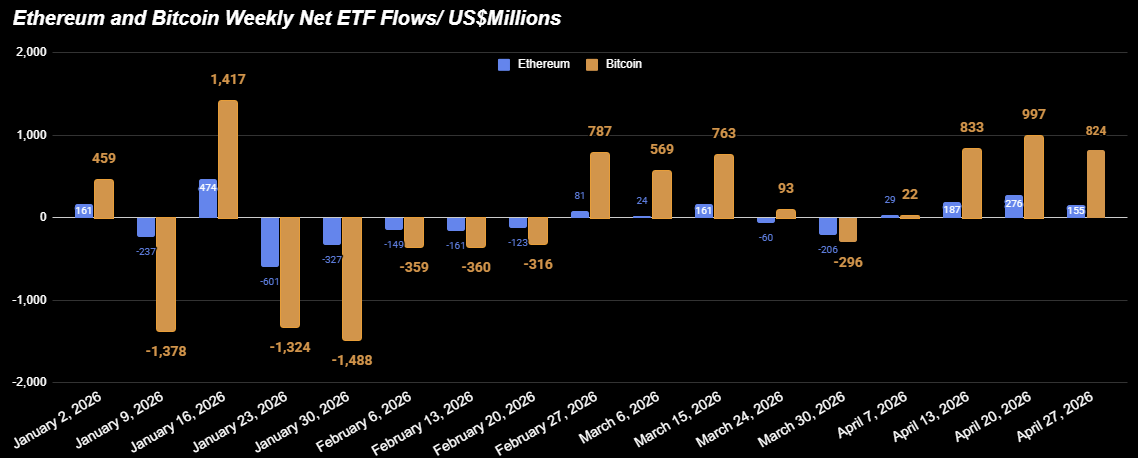

3. ETF flows held strong despite geopolitical stress and DeFi turmoil

BTC +$824M (9-day inflow streak), ETH +$155M. Combined $979M — fourth straight week of strong inflows, with $2.44B absorbed in April alone (highest since October 2025). Institutions are stacking exposure ahead of Wednesday's FOMC, even with Kelp aftermath and geopolitical tensions remains unresolved.

Broader Market Outlook:

Both BTC and ETH showed modest recovery momentum amidst this year's DeFi’s biggest hack. BTC traded as high as ~$79,500 (+6% weekly), repeatedly testing but failing to break $80K. ETH gained 4% last week despite heavy DeFi stress.

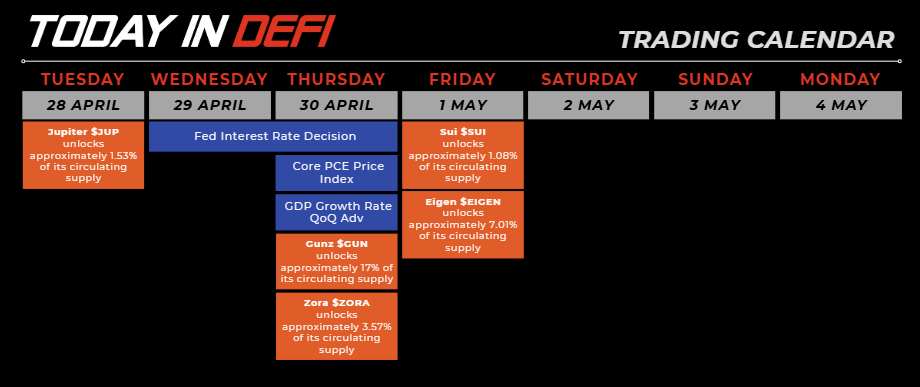

A heavy macro week ahead. Tue Apr 28 — US Consumer Confidence. Wed Apr 29 — FOMC decision + Powell press conference (98% probability of a hold at 3.50-3.75%, possibly Powell’s last meeting before Warsh transition May 15). Thu Apr 30 — US Q1 GDP + March PCE inflation. Apr 27-29 — Bitcoin Conference Las Vegas, historically market-moving.

ETF Flows: The Institutional Counter-Narrative

Weekly spot ETF flows: BTC +$824M, ETH +$155M. Combined $979M — fourth straight week of strong inflows for BTC. The streak isn’t slowing; it’s slightly cooling but staying decisively positive while DeFi is bleeding.

This is the dominant macro signal for the week ahead: institutions are adding exposure to Wednesday’s FOMC. The divergence has been running for 4 weeks now and shows no sign of breaking — and it’s the cleanest case for “buy what institutions are buying” we’ve had this year.

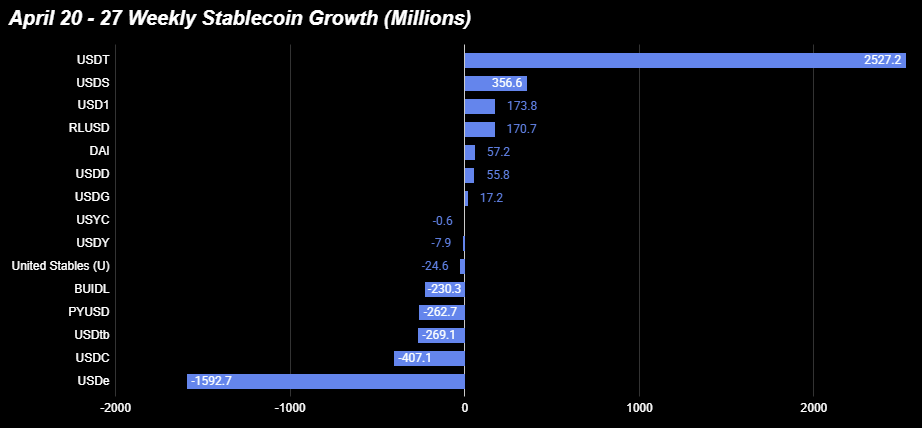

1. Stablecoin Flows: Lowest Weekly Inflows This Month

Weekly flow: +$57M (+0.02%). This is the lowest weekly print since the contractions in early February. Net stablecoin growth has effectively stopped.

USDT +$2.53B (+1.35%). Another huge week. USDT inflows usually read as risk-on — but this week's print looks more like a defensive parking move.

USDC - $407M (-0.52%) contracting for two weeks running confirms broader DeFi deleveraging. The likely driver is USDC leaving DeFi positions. USDC growth used to outpace USDT, but ever since the resolv hack, USDC growth has stagnated and reverse

USDe -$1.59B (-32%) — the move of the week. Ethena’s synthetic dollar lost a third of its supply in a single week. The mechanism: most USDe was used as liquid leverage on Aave (farmers borrow USDC and USDT against sUSDe to amplify Ethena’s basis yield). When the Kelp DAO exploit froze Aave’s WETH markets and pushed stablecoin borrow rates to extremes, those leverage strategies flipped to negative carry — forcing widespread unwinds. Each unwind redeems USDe.

USDtb (-32%, -$269M) tells the same story. Ethena’s RWA-backed stablecoin contracted by exactly the same percentage as USDe, on the same mechanism — leveraged farmers unwinding Ethena positions across the board.

USDS +$357M — full reversal from last week. Last week USDS was the biggest loser at -$797M (mostly internal sUSDS → stUSDS rotation). This week the flow flipped, with capital coming back in as stUSDS yields stabilized and SKY price held through the Aave fallout. The “Sky vindication” trade is real — they didn’t break.

USDD +$56M, RLUSD +$171M (+12.23%), USD1 +$174M. RLUSD (Ripple’s stablecoin) growing 12% in a week is one of the few quiet bright spots.

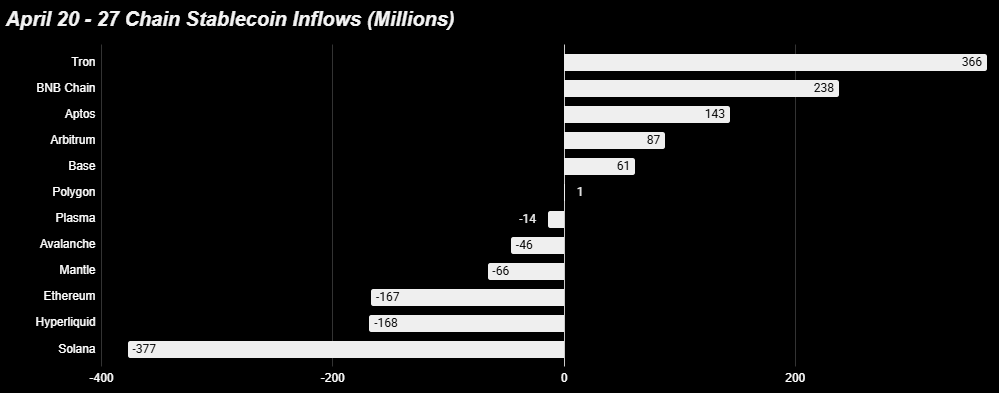

2. Stablecoin Flows Per Chain✅

The “DeFi blue chip” chains all contracted this week. Ethereum, Solana, and HyperEVM — the three biggest hubs for active DeFi yield strategies — all bled stablecoin supply.

While HyperEVM’s 3% outflow is primarily caused by Purrlend’s $1.5M exploit, the chains absorbing capital are the ones that act primarily as USDT payment rails: Tron, BNB Chain, and Aptos (the +8.87% on Aptos is the biggest % gain on the board).

When capital pulls out of DeFi because of sentiment or unnattractive yields (negative carry on basis trades, frozen lending markets), capital sits on the chains where stablecoins move and earn nothing, not the chains where they’re deployed for yield.

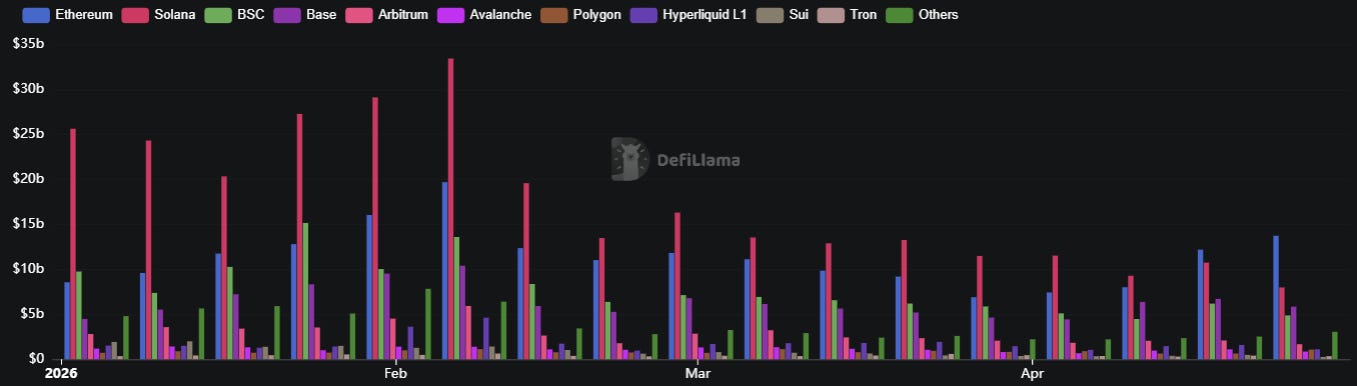

3. DEX Volumes — Ethereum Reclaims Dominance

Ethereum is back at #1 in weekly DEX volume (~$13.5B) — the first time since early February. Solana, which has led most weeks of 2026, dropped to roughly $8B and continues its deceleration from the $25-30B February peaks.

Base continues to outpace BSC’s DEX volume in the last 3 weeks. The chain hierarchy in DEX activity now reads: Ethereum > Solana > Base > BSC, a meaningful change from the Solana-led pattern that defined Q1.

The connecting thread: Ethereum lost stablecoin supply this week but gained DEX volume. That’s not a contradiction — that’s existing capital being put to active use rather than new capital being parked. The active traders left on Ethereum are working harder. Solana saw the opposite pattern: stablecoin outflow and DEX deceleration.

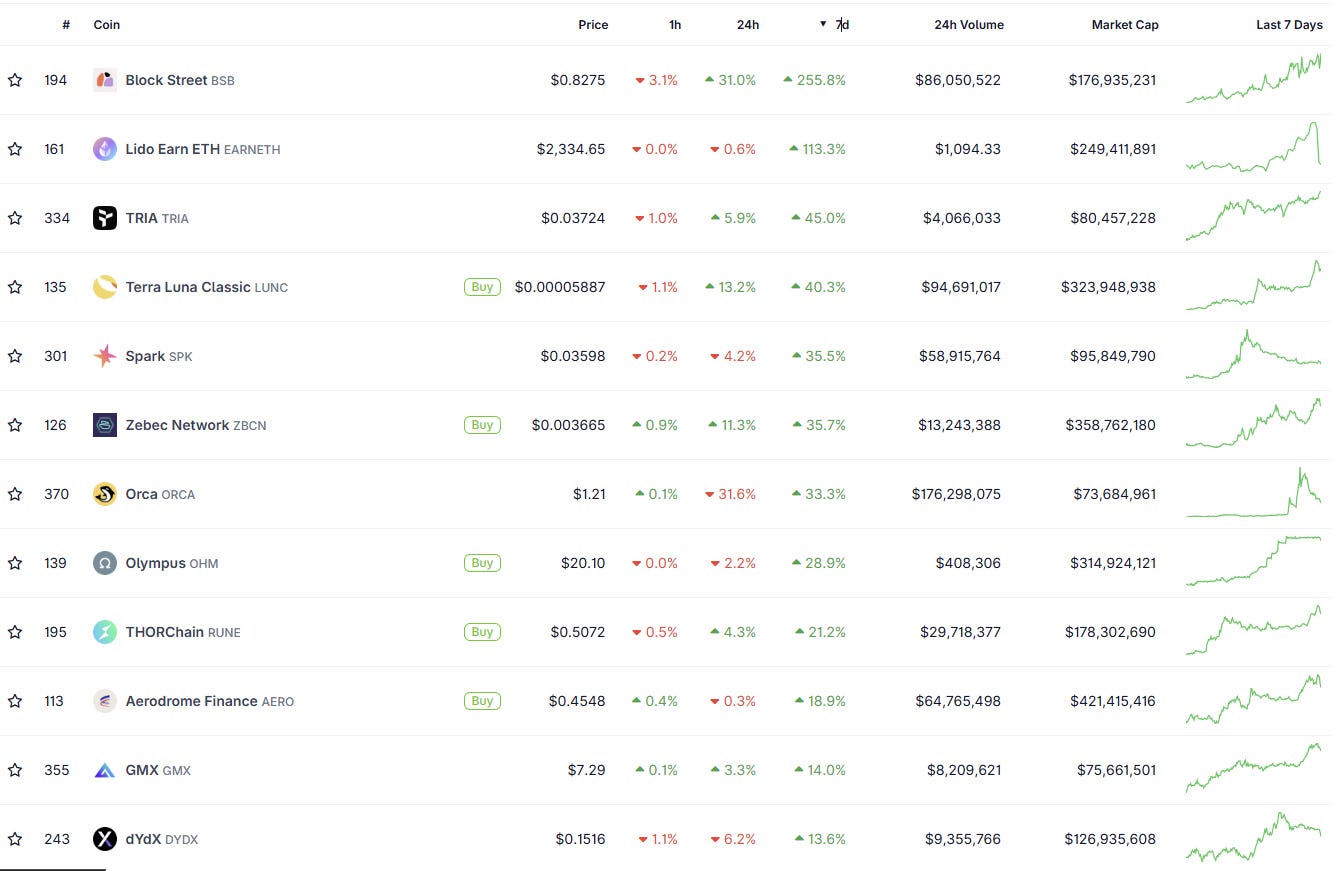

4. DeFi token price gainers & their catalysts

Context for the week’s moves — observations, not trade ideas. Many of these have already run.

$ORCA +34.4% — Solana DEX activity + Orca joined the major US crypto legislation advocacy push on Apr 24. Regulatory advocacy by a top Solana DEX positions ORCA on the right side of the legislative tailwind.

$SPK (Spark) +31.4% —The clearest Aave → Spark capital rotation story.

Following the Kelp DAO exploit, over $1B-$1.7B rotated from Aave into SparkLend in 4-5 days, with Spark's TVL jumping 28% to $4.78B. Justin Sun moved $174M to Spark, becoming the focal point. Plus: Upbit (Korea) listed SPK on Apr 23 adding KRW retail liquidity

$OHM (Olympus) +28.6% — The main reason for Cooler Loans’ TVL surge. OIP-194A governance proposal is accelerating Cooler V2 (perpetual fixed-rate loans, no price-based liquidations, treasury-backed). This is a fundamentally different lending model, and during a week when liquidations on Aave/Compound destroyed billions, “no liquidations” became a real product feature.

$AERO +19.1% — Whale accumulation + cross-chain merger anticipation. Hypersphere Ventures deployed ~$680K into AERO in late April, coinciding with a 50.77% surge in Smart Money balances and tokens leaving exchanges. The structural catalyst is the Aerodrome-Velodrome merger ("Aero") targeting Q2 2026 — bringing Slipstream V3 with MEV auction capture, expanding to Ethereum mainnet.

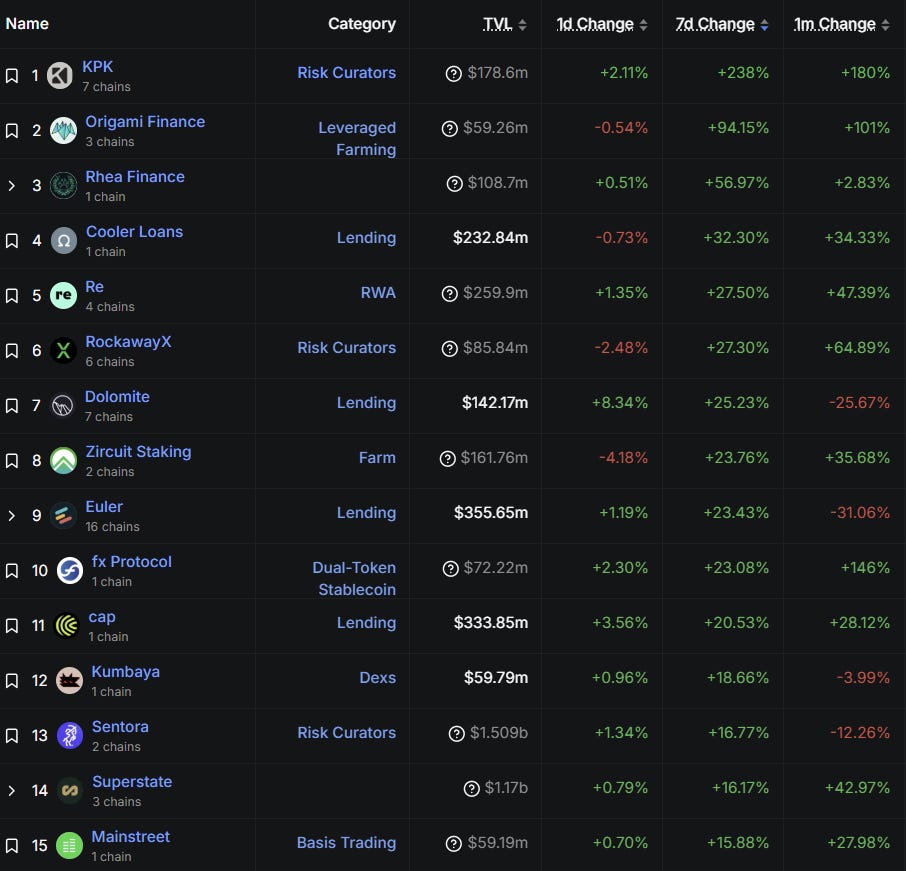

5. TVL gainers, and their catalysts

The macro theme this week is sharper than just “flight to RWA.” Capital is rotating specifically into assets that aren’t exposed to the rsETH/Aave contagion — protocols whose collateral, yield source, or borrowing markets sit outside the credit crunch.

The protocols absorbing capital share three traits: collateral that isn’t tied to rsETH or stressed lending pools, yield sources independent of DeFi credit markets, or alternative venues for leveraged exposure that don’t depend on Aave/Compound liquidity.

#1 Superstate — $1.17B TVL, +$163M weekly (+16.17%, +43% monthly)

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.