Hyperliquid’s Biggest Catalyst, Solana Stablecoin Boom - Weekly Onchain Outlook

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Headlines:

- Echo Protocol exploited through fraudulent eBTC minting

- Liminal’s limUSD launches yield trading on Pendle

- Pendle lists new STRC markets by Apyx

- Bitwise allocates BHYP fees toward HYPE holdings

- Aave upgrades Savings GHO (sGHO) to 4.25% APR

- Curvance pauses Echo eBTC isolated market

- SEC plans decentralized tokenized securities exemption

- Strategy acquires additional 24,869 Bitcoin

- Galxe SpaceStation exploited through compromised signing key

rFind and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

In this letter, we bring you the best bottom-up analysis of onchain trends, along with top-down market analysis, helping you find top yield opportunities and position for trends before they happen

1. Macro + Capital Backdrop

1A) Traditional Macro Variables

1B) Crypto Capital On-Ramps

1C) Week-Ahead Catalysts

2. Onchain Risk Regime

3. Chain Comparison

3A) Stablecoin Flows by Chain

3B) Structural Shifts

4. Project & Protocol Discovery

4A) Token Price Movers

4B) TVL Gainers

4C) Protocols to Farm

Key Takeaways:

Regime: Mixed/Neutral with a hostile edge.

Net liquidity is supportive, but rates are pushing on risk. Onchain stablecoin supply grew , but at 900M, growth was below average. ETF Flows were negative - probably reacting to inflation fears. Bond yields rising recently present a headwind to both risk assets and onchain liquidity which have to compete with higher off chain yields.Solana is the main destination for stablecoin farming this week, gaining more than $1B in inflows tied to USDe and USDG yield strategies across Kamino and Jupiter Lend. The flows appear driven primarily by leveraged stablecoin carry trades rather than broad speculating/trading activity.

Hyperliquid continues to strengthen structurally.

Stablecoin supply on the chain rose another 2% this week and more than 6% over the past month, supported by growing adoption around HIP-4 prediction markets and the AQAv2 USDC integration involving Coinbase and Circle. Unlike the sharper incentive-driven spikes seen elsewhere, Hyperliquid’s growth remains steady and increasingly tied to ecosystem usage and liquidity depth.

1. Macro & Capital Context🏛️:

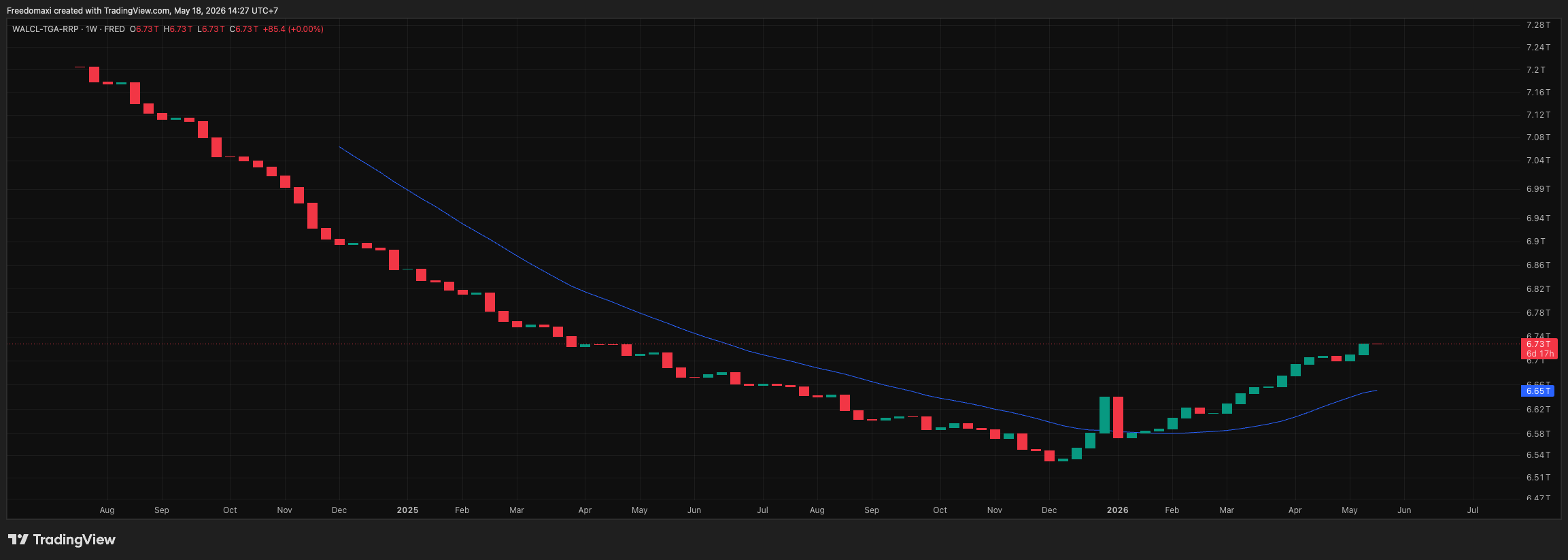

1A) Net liquidity (WALCL-TGA-RRP): level + WoW change + trend vs 20W MA

This week's add is roughly 5x last week's pace. Net liquidity reversed from the early-2026 $6.55T trough and is now trending decisively above its 20W MA after 18 months below

DXY: level + position vs 20W MA

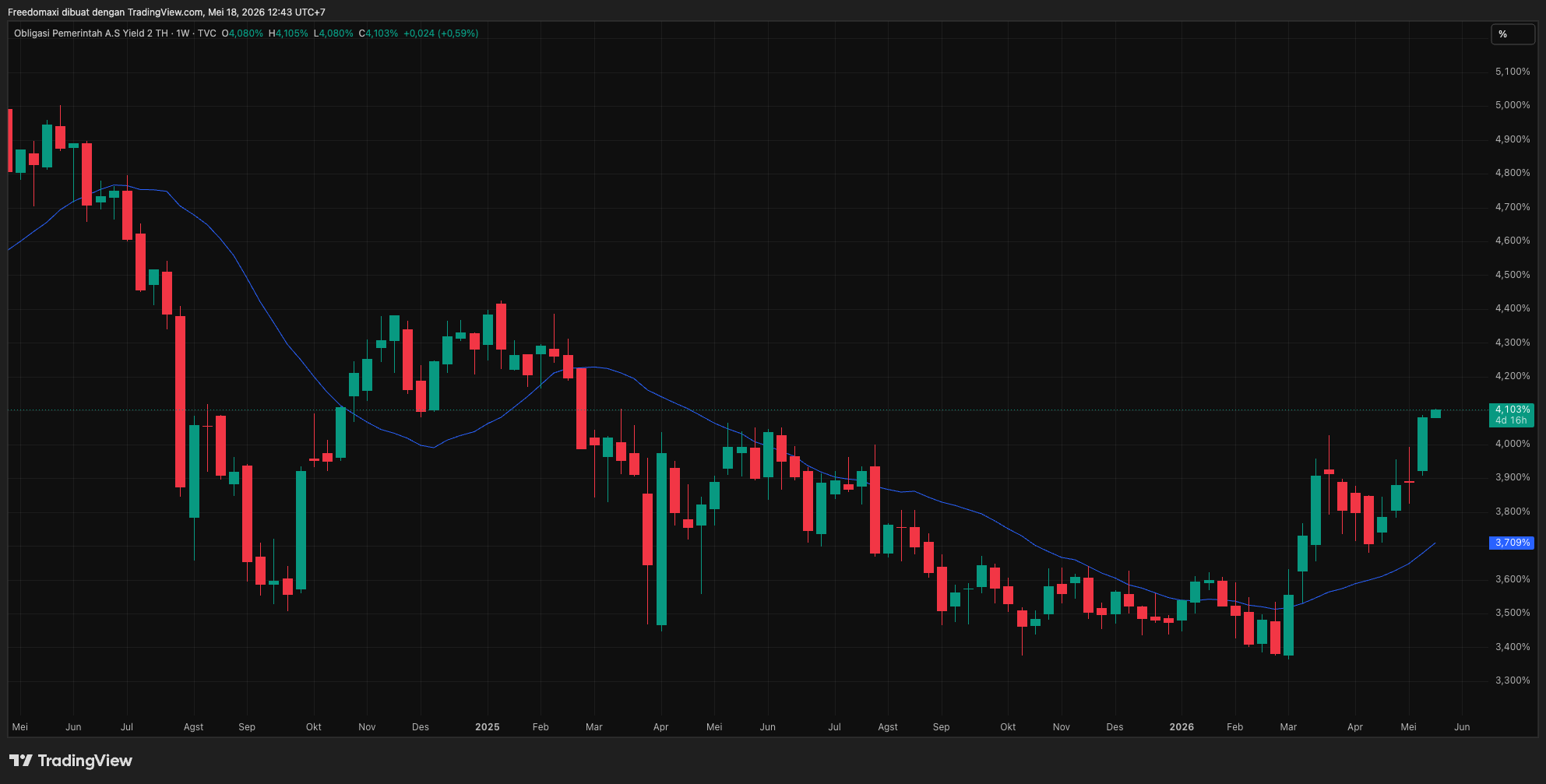

The 2Y is now ~40bps above its 20W MA after bouncing off the March 3.4% low. Bond market is repricing for a longer Fed pause — consistent with April CPI at 3.8% and rising hike-by-year-end probability.

Transmission to onchain: raises the bar for stablecoin yield vaults vs T-bills (~4.1% risk-free competing with 5-6% in curated Morpho/Euler vaults — spread compressing). Historically also a headwind for long-duration assets including BTC and ETH.

BTC/NQ ratio

Below 20W MA (2.90) — HOSTILE. Confirmed BTC underperformance regime since July 2025. Ratio is ~9% below 20W MA and has compressed near 2.65 for six weeks. Institutional capital still rotating toward tech (NVDA earnings Wednesday will test this), away from crypto.

The compression near lows is worth watching — six weeks of sideways below 20W MA often precedes either a capitulation flush or a reversal, but no signal yet.

Conclusion:

Net liquidity is doing all the heavy lifting on the bullish side. Rates and rotation are both pressing against risk. Dollar is a mild headwind. The market is essentially asking whether liquidity expansion can overcome a hardening rates picture.

1B. Crypto Capital On-Ramp

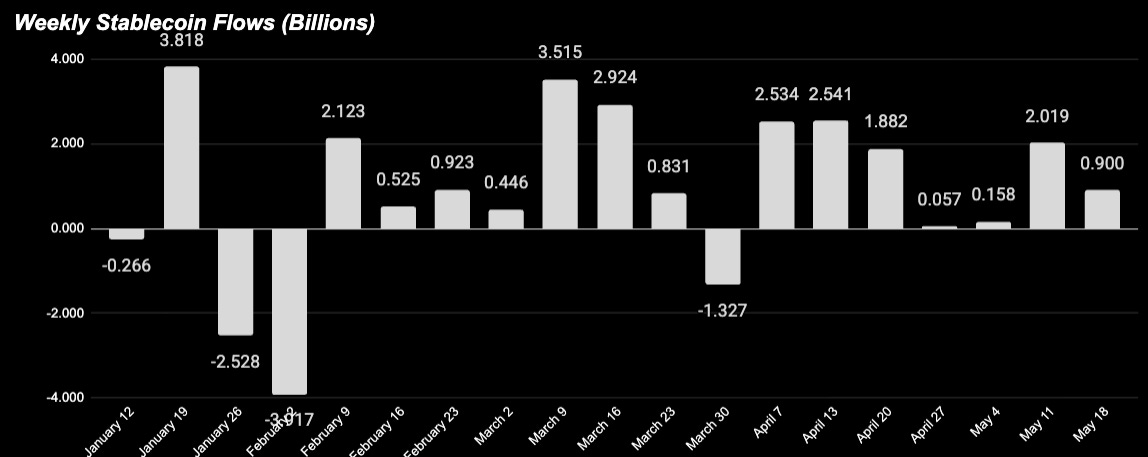

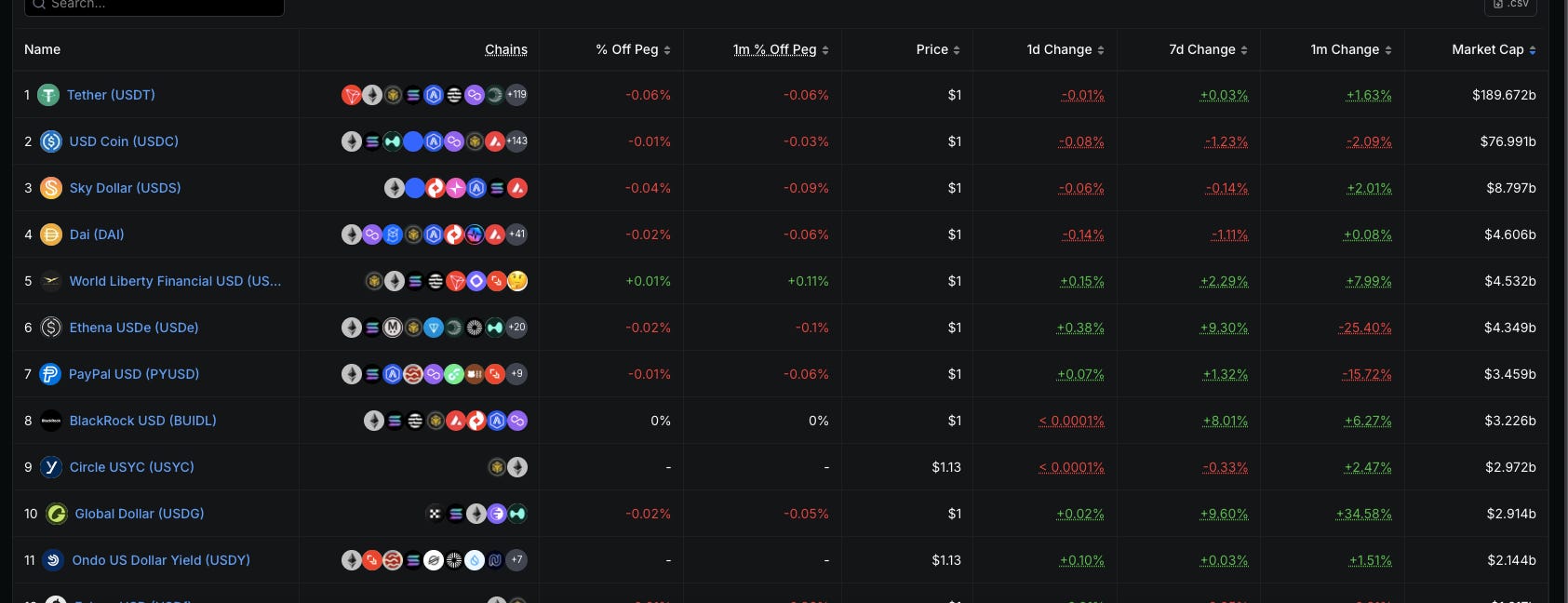

Total stablecoin supply: $323.44B, +$900M WoW (+0.28%).

Net stablecoin growth continues but the pace cooled materially from last week’s +$2.019B print — roughly a 55% deceleration. Capital is still arriving onchain, just at a normalized rather than accelerating rate. Monthly context: total supply is still in its established uptrend; this is a single week of decel, not a regime change.

USDC vs USDT — full composition reversal this week:

USDC: -$896M (-1.15%) — complete reversal from last week’s +$1.608B comeback

USDT: +$94.8M (+0.04%) — essentially flat

Deployment capital (USDC) pulled back sharply, while parking capital (USDT) remained stable. Last week’s “USDC leads DeFi back” thesis partially unwound on the macro shock (PPI +6% May 13). One week isn’t structural, but watch whether USDC resumes inflows.

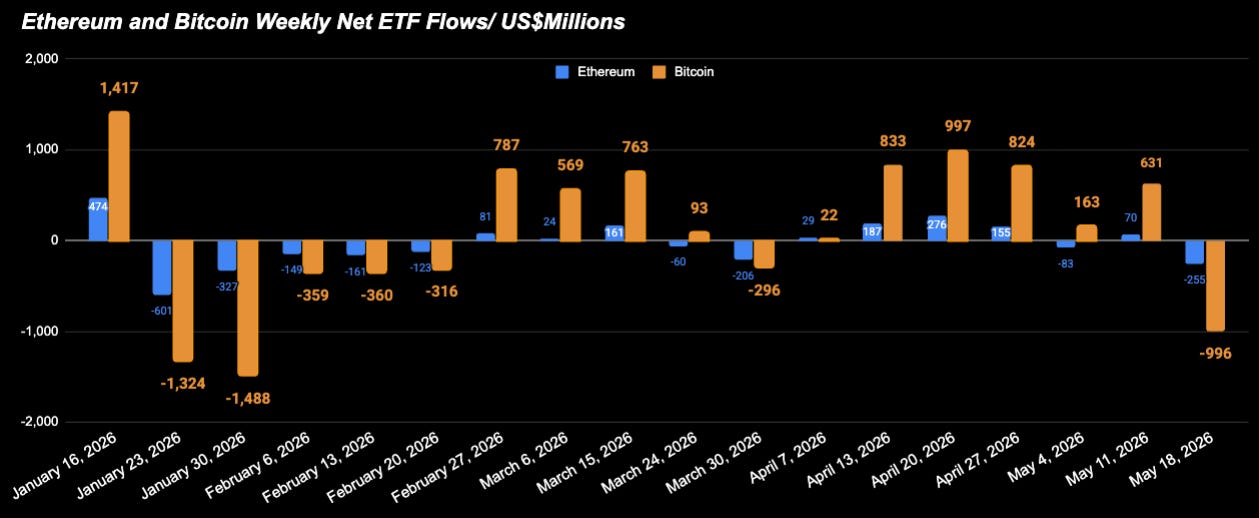

ETF flows: BTC -$996M, ETH -$255M (combined -$1.25B).

The 5-week BTC ETF inflow streak ended hard. Driver: PPI shock on May 13 reset rate expectations. Sources: Yahoo Finance, Spotted Crypto.

1C. Catalysts For the Week-Ahead

CLARITY Act cleared Senate committee May 14. SEC Chair Paul Atkins indicated full passage possible in June. Watch for Senate floor consideration this week.

SEC innovation exemption sandbox for tokenized securities expected “over the next few weeks” per Atkins.

Major L2 unlocks already hit: APT (May 12, ~$102M), STRK (May 15, ~$145M), ARB (May 16, ~$108M).

Liquidity is supportive, but rates, dollar, and rotation are pressing against risk. USDC reversal confirms onchain capital is sensitive to macro shocks. Watch FOMC minutes May 20 and NVDA earnings for direction.

2. Onchain Risk Regime

Stablecoin Composition — Who Grew, Who Shrank

Growing (7d):

USDe +9.30% (+$365.5M)

USDG +9.58% (+$252.3M) — Global Dollar Network

BUIDL +8.01% (+$237.7M) — BlackRock tokenized MMF

USDtb +7.85% (+$256.2M) — Ethena RWA-backed (MegaETH loop driver)

World Liberty USD +2.14% (+$94.8M)

PYUSD +1.25% (+$42.7M)

Contracting (7d):

USDC -1.15% (-$896.3M)

DAI -0.93% (-$43.3M)

USYC -0.33% (-$9.8M)

The “USDC leads, USDT parks” signal from last week did not extend. This week, growth concentrated in DeFi-native synthetic dollars (USDe, USDtb) and institutional/RWA dollars (BUIDL, USDG). USDC actually contracted. The composition tells you yield-seeking and RWA capital are still flowing.

USDe / Ethena Status

USDe supply at $4.33B, with +$365.5M (+9.30%) this week, obviously the biggest absolute weekly inflow since pre-Kelp. Third consecutive week of recovery (+$151M, +$62M, +$365M). Ethena’s TVL gained +$733M to $5.37B (+16.14%).

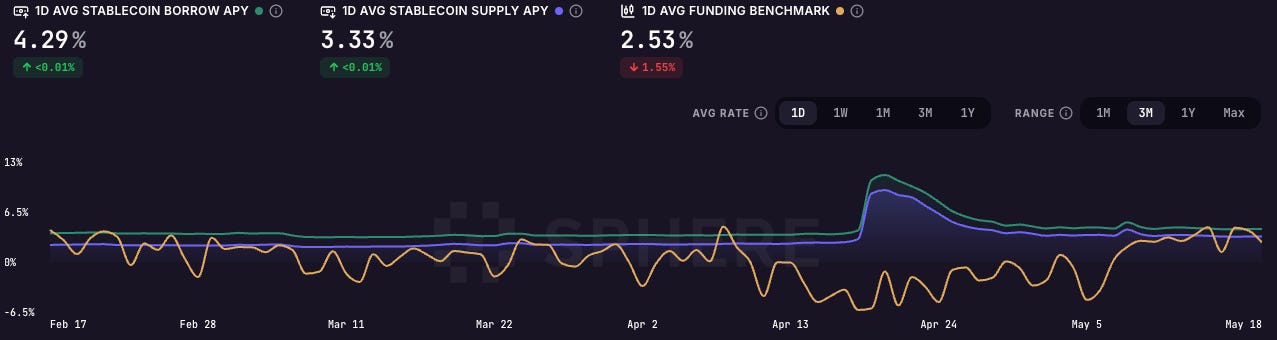

Aave / Sphere Stablecoin Rates

Borrow APY 4.29%, supply APY 3.33%. The mid-April spike during the Kelp unwind has fully unwound; rates are back at pre-event baseline. Funding benchmark at 2.53%.

Signal read: Onchain leverage is calm — no forced unwind pressure. The market has digested the Kelp event from a rates perspective. Source: Sphere.

Watch item: Supply APY at 3.33% is now ~80bps below the 2Y Treasury at 4.10% — base Aave yields are no longer competitive with T-bills, pushing yield-seeking capital toward curated vaults (Morpho/Euler at 5-6%) or out of DeFi entirely. This explains the structural Aave-to-Morpho migration we’ve been tracking, but the spread compression is also a headwind for total DeFi yield-seeking capital.

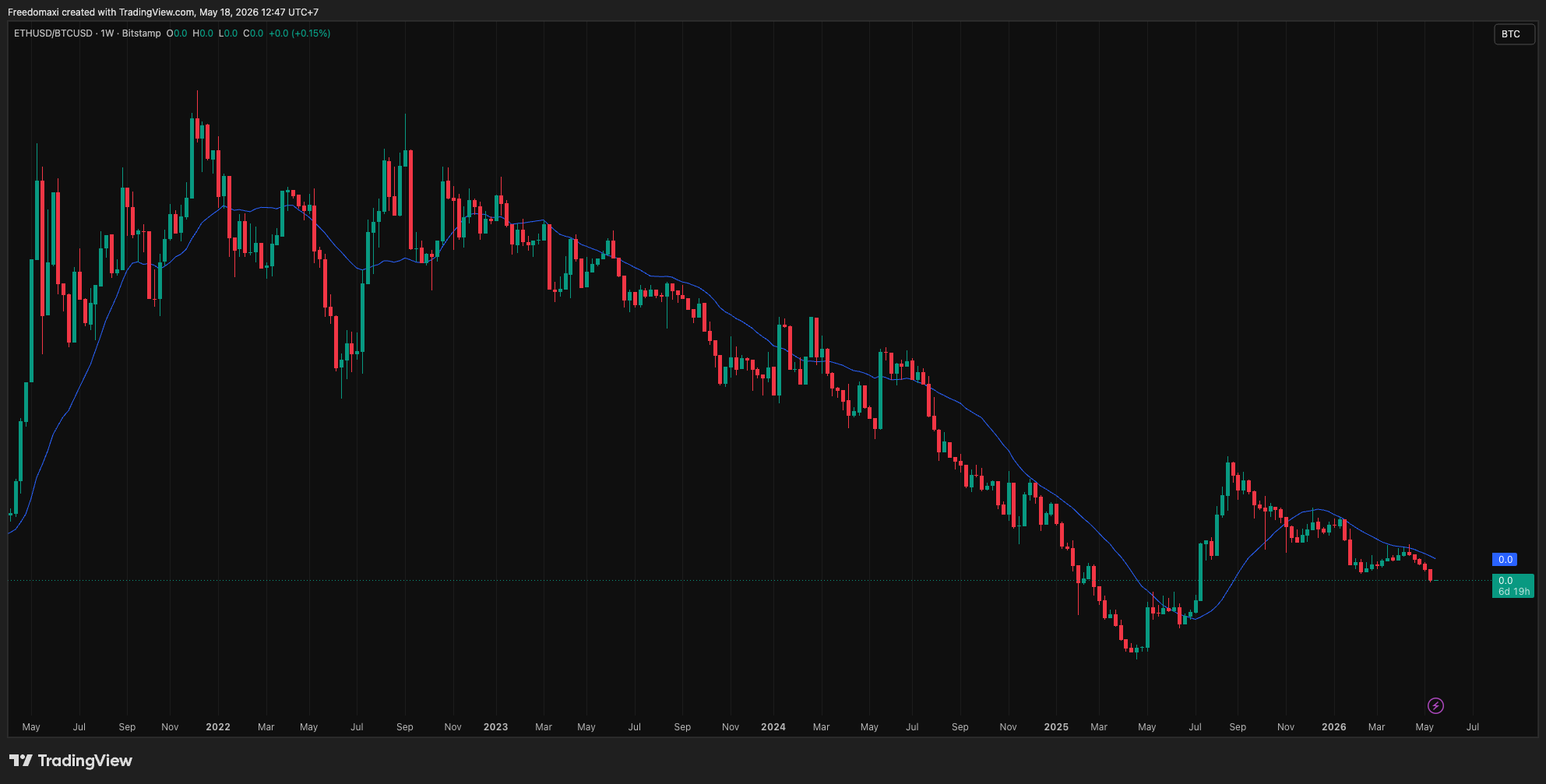

ETHBTC vs 20W MA

ETH/BTC pair remains in the multi-year downtrend, still below the 20W MA after a failed 2025 reclaim attempt. Capital within crypto continues to favor BTC over ETH. Allocation read: No signal yet to overweight ETH within the crypto sleeve. Wait for a weekly close above 20W MA before sizing up ETH exposure.

3. Chain Comparison

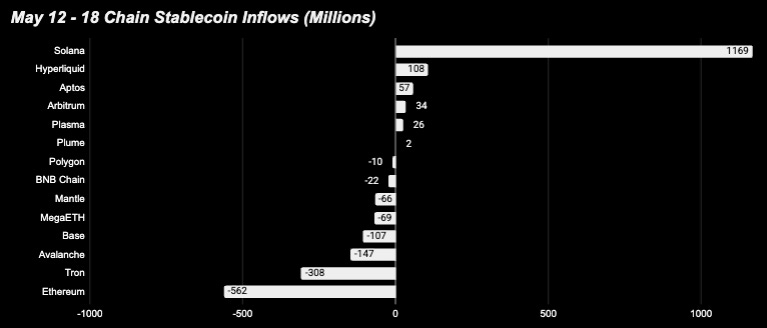

Solana gains $1.169B stablecoin supply

This isn’t broad-based ecosystem growth, it’s a specific yield loop: USDe (+$365M total) and USDG (+$252M) are flowing onto Solana for deployment into Kamino and Jupiter leveraged stablecoin strategies. Jupiter Lend’s intergation on Bitwise-managed USDe market launched this week and hit $500M TVL on day one, confirming the deployment infrastructure has the depth to absorb the inflows. This is yield-seeking farming capital, not retail speculation — sticky if the basis trade holds, mercenary if it doesn't.

Hyperliquid is one of the strongest chains on the list: +2.00% 7d, +6.02% 30d. Not a spike — a steady, building trend. HIP-4 prediction markets and now the AQAv2 announcement (Coinbase + Circle staking HYPE) are real adoption drivers.

MegaETH 7d -9.17% vs 30d +657.54% — the structural deceleration is now visible in the data. First weekly outflow after weeks of incentive-driven growth. The Aavethena loop hit structural supply cap limits. The $500M USDM KPI that would trigger the next MEGA unlock appears to have been the ceiling for this inflow wave. The 30d still looks heroic but the marginal pace has stopped.

Losers:

Ethereum -$562M(-0.1%) — second straight week of minor outflows, even larger than last week. USDC contraction is concentrated here.

Tron -$308M — first material reversal in months after consistent +$1B+ weekly inflows. USDT only +$94M total this week vs much larger prior weeks. Monitor for next week.

Avalanche -$147M (-9.32%) — reversed from +$133M last week. The BUIDL inflows aren’t enough to offset broader withdrawals.

MegaETH -$69M (-9.17%) — first outflow after weeks of growth. Aavethena loop hit structural supply cap limits.

Base -$107M — paused. Coinbase-Centrifuge institutional RWA pipeline is still ramping; no major launches landed this week.

Concentration flags:

Solana’s $1.169B revolves around a single yield loop. If the USDe/USDG leverage loop farming that offers up to 20%+ on two “Blue-chip” stablecoins. Moreover, the USDG supply itself is supplied by Ethena, and the yield from the USDe supply is earning from underlying t-bill collaterals.

3B. Structural Shifts

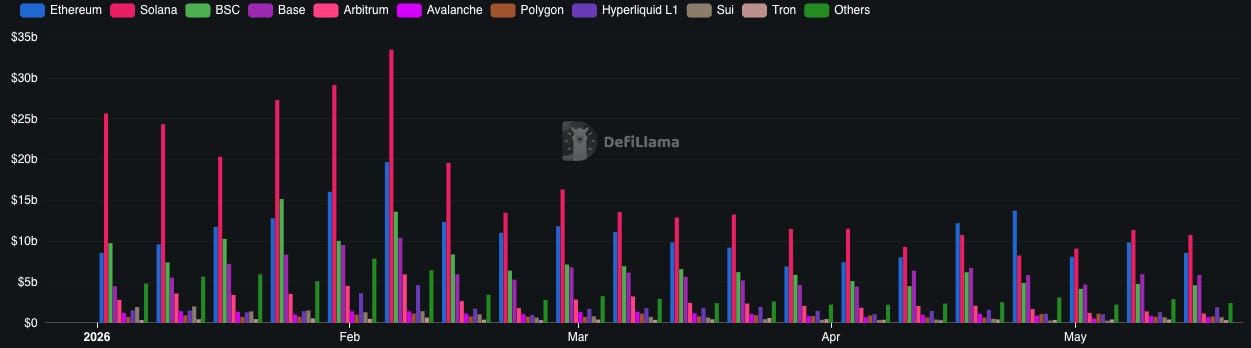

Base continues structurally overtaking BSC in DEX volumes. Sixth consecutive week of Base outpacing BSC: Base $5.929B vs BSC $5.163B (7d). The pattern is now firmly established. he interesting question is what's being traded, because Base doesn't have its own native L1 token to drive volume the way BNB does on BSC or HYPE does on Hyperliquid.

Based on the fees generated on Aerodrome, you can see the most traded tokens are AI-related tokens like Venice AI’s VVV token. LLM model broker. It allows users to access the underlying models, such as chatGPT indirectly through Venice for privacy and also lower subscription price. Users can use VVV to pay for the fee, giving VVV a real usage.

Arbitrum DEX volume collapsed to $1.14B 7d — the sharpest contraction in the top-10 chains. Compare to Solana ($11.3B), Ethereum ($9.05B), Base ($5.93B). Arbitrum has lost more DEX market share proportionally than any major chain over the past quarter. The small +$34M stablecoin inflow this week is a pause, not a reversal — DEX activity confirms structural weakness continues.

4. Project & Protocols Discovery

4A. Token Price Movers

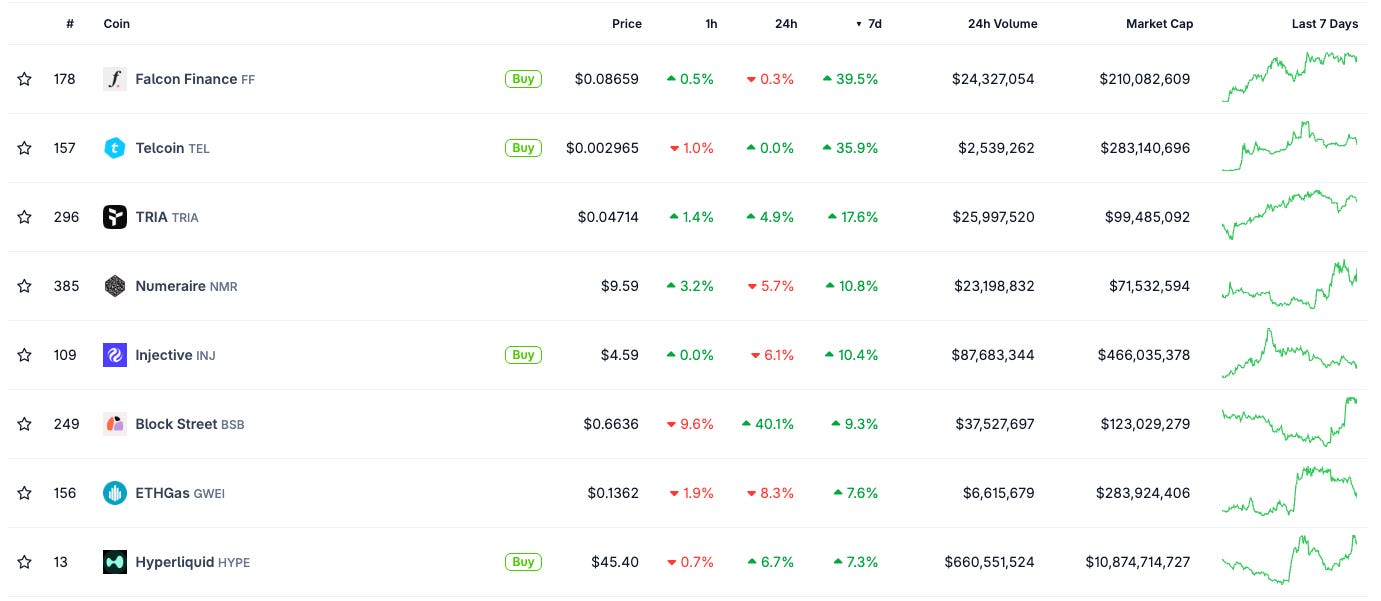

$HYPE +7.3% — Two concrete catalysts this week. First, on May 14, Coinbase and Circle announced they would activate AQAv2 on USDC, with both committing to stake HYPE. USDC becomes the most aligned stablecoin on Hyperliquid, with Coinbase as treasury deployer sharing the majority of reserve yield revenue with the protocol. USDH (Native Markets’ protocol-aligned stablecoin) gets sold to Coinbase, and HIP-4 prediction markets will use USDC as quote asset in a future upgrade. Second, Hyperliquid’s Jeff Yan spent May 14-16 in Washington meeting with policymakers during CLARITY Act advancement. Sources: Hyperliquid X, Jeff Yan X.

$INJ +10.4% — Real catalyst: On May 14, Injective announced a partnership with Musicow to tokenize music IP, targeting what they describe as a $200B asset class with “none currently onchain.” Major global artists are set to be revealed in coming months. The announcement positions Injective as the chain for music rights tokenization — a new RWA vertical distinct from tokenized stocks/Treasuries. Source: Injective X.

$FF (Falcon Finance) +39.5% — Falcon is a synthetic dollar protocol (USDf, sUSDf) positioning as the RWA collateral layer — users deposit tokenized stocks, Treasuries, and other RWAs to mint USDf without selling. The +39.5% move tracks several reinforcing narratives: total onchain RWAs hit a $32B all-time high (private markets +73%, stocks +29%, VC +25% in under a month), SEC Chairman Atkins’ tokenization comments resurfaced, and Falcon’s positioning as the collateral layer for tokenized assets aligns with these flows. Source: FalconFinance X.

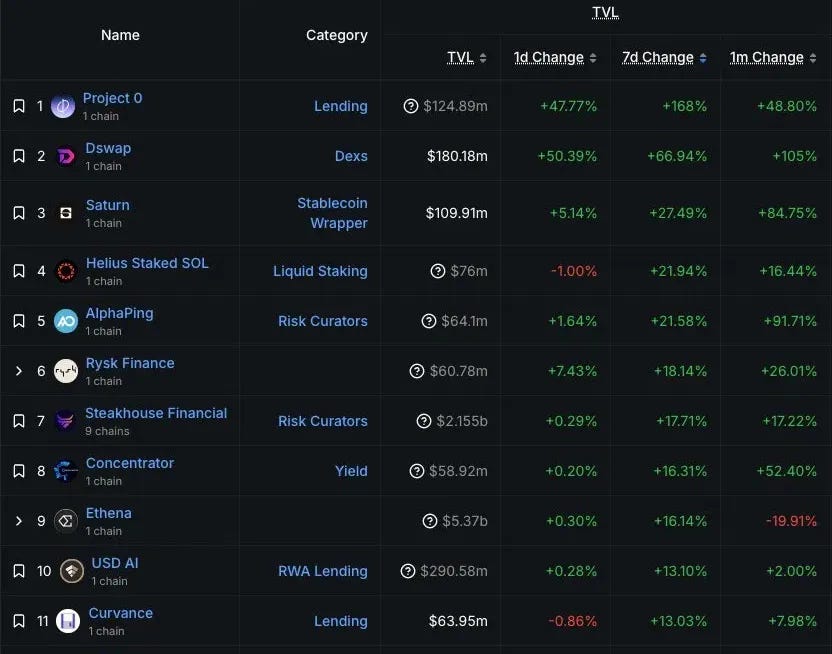

4B. TVL Gainers — Ranked by Absolute $ Inflow ($50M+ filter)

Ethena — $5.37B TVL, +$733M

Ethena recorded a 17.7% increase in TVL over the trailing seven days, reaching $5.37 billion. This represents an absolute growth of approximately $949 million, marking the largest absolute gain among tracked DeFi protocols for the week. This shift represents a recovery from a depressed baseline following the KelpDAO bridge exploit rather than a lifetime high, supported by three distinct operational developments.

Ethena deployed $400 million in USDG split equally between two Solana lending markets: the Bitwise-curated Jupiter Lend and the Sentora-curated Kamino. Kamino achieved 100% utilization within 24 hours, and the total USDe supply on Solana expanded 230-fold from $1.5 million to $350 million between May 10 and May 15.

Second, on May 7, Grayscale added ENA to its DeFi Fund with a 13.59% allocation, which corresponded with a three-month high in new institutional wallet creation and increased whale activity.

Third, the Ethena Foundation confirmed that all risk and operational conditions required to activate its fee switch have been met, signaling a transition toward a cash-flow-generating model.

Concurrently, data shows an internal capital migration; on a 30-day basis, USDe TVL declined by 25.4% while the market-neutral, T-bill-backed tranche, USDtb, expanded by 23.8%, running seven times faster than USDe on a 7-day basis.

This divergence indicates that compressed ETH funding rates are driving capital away from delta-neutral basis trading toward uncorrelated treasury-backed assets that offer comparable yields with zero crypto-market correlation.

Steakhouse Financial — $2.155B TVL, +$334M (+17.71%)

Morpho Curation Realignment: Steakhouse Financial Establishes TVL Lead Over Sentora

Fourth consecutive week of strong inflows. Morpho curator continues absorbing the Aave-to-Morpho migration with no specific weekly catalyst — purely structural lending venue shift. +17.22% monthly confirms sustained, not spiky, adoption.

M0 Infrastructure Adoption and the Onboarding Cycle of the GENIUS Act

M0, a backend infrastructure layer designed for institutions to issue regulated stablecoins, grew to $333.5 million in TVL, reflecting a 12.7% increase over seven days and a 9.2% increase over 30 days. The platform currently serves as the underlying protocol for live integrations with Stripe, MoonPay, and MetaMask.

On April 30, Anchorage Digital, the first federally chartered crypto bank in the United States, selected M0 as its core technology provider for a new regulated stablecoin issuance platform. This announcement coincided with legislative advancements regarding the federal GENIUS Act, which mandates formal stablecoin issuance pipelines for large fintech firms and positions M0 as canonical middleware for compliance.

A subsequent single-day inflow of $23.9 million on May 16 marked the largest deposit in the 30-day window, indicating a two-to-three week operational delay between corporate announcements and actual on-chain capital onboarding.

Project 0 — $125M TVL, +$80M (+168%, +48% monthly)

DEX on 1 chain. Given Solana’s massive stablecoin inflows this week and Dswap’s category (DEX), the likely driver is Solana ecosystem liquidity expansion from USDe/USDG loops flowing into LP positions. +105% monthly confirms this is sustained, not a one-week spike.

4C. Farming / Positioning Candidates [Premium]

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.