Intro to Yield Basis V3: LP With No Impermanent Loss

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Highlights:

- Morpho unveils fixed-rate Midnight lending protocol

- Sei targets 200K TPS with Giga roadmap

- Base upgrade cuts withdrawals to one day

- Stake DAO exploited via fake vsdCRV minting

- Hastra PRIME vault cap raised to 80M

- Ventuals oracle glitch triggers SPACEX liquidations

- Anchorage Digital takes strategic position in Solstice’s SLX

- Solflare enables SOL-backed card borrowing

- Jupiter launches RainFi JUICED airdrop

- Claude Opus 4.8 officially launches

- DxSale exploited after hidden ownership transfer

- Frax sunsets EtherFi Top Spender rewards

- Praxis opens Base testnet in June

- Odyssey launches leveraged Cap cUSD strategies

- Superform unveils fully onchain vault operating system

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

Yield Basis, developed by Curve Finance founder Michael Egorov, is an AMM protocol designed to address impermanent loss for LPs. By integrating natively with Curve’s infrastructure, it attempts to allow LPs to maintain 1:1 spot exposure to volatile assets while earning trading fees.

The Problem: Impermanent Loss (IL)

When providing liquidity to a standard BTC/Stablecoin pool, LPs are essentially agreeing to continuously trade against the market:

If BTC rises: The AMM automatically sells the LP’s BTC for stablecoins.

If BTC falls: The AMM buys more BTC using the LP’s stablecoins.

Because of this constant rebalancing along a square-root curve, LPs are forced to sell winners and buy losers. The gap between the value of simply holding the assets and the value of the LP position is known as Impermanent Loss (IL).

To visualize this mathematical drag, assume a user starts with 1 BTC (priced at $100,000) and $100,000 in crvUSD. They can either hold both assets in their wallet or deposit both into a standard liquidity pool:

(Note: The following scenarios and figures are simplified for conceptual clarity and serve as a rough reference only, rather than a precise mathematical calculation).

As the table shows, in trending markets, standard LP positions mathematically underperform a simple “buy and hold” strategy regardless of the direction.

The Mechanism: Hedging IL via Leverage

Yield Basis attempts to eliminate IL mathematically by utilizing 2x compounding leverage.

Instead of depositing two tokens, a user deposits only the volatile asset (e.g., 1 BTC). The protocol uses that BTC as collateral to flash-borrow an exact equivalent USD value of crvUSD. It then pairs the deposited BTC with the borrowed crvUSD and deposits both into a Curve pool. This creates a 50% debt-to-value ratio (2x leverage).

To maintain this strict 2x leverage, Yield Basis relies on automated arbitrageurs to continuously rebalance the position based on price movements.

(Again, these figures are for rough reference only to illustrate the mechanism rather than a precise on-chain calculation).

The Setup: Day 1

Assume a user has 1 BTC and the current market price is $100,000.

Action: The user deposits 1 BTC. The vault borrows $100,000 in crvUSD.

The Position: The user now has a $200,000 LP position backed by $100,000 in debt. Net equity is $100,000 (matching the initial capital).

Scenario 1: The Bull Case (BTC jumps 44% to $144,000)

Standard LP (Underperformance): The pool sells the BTC on the way up. The total LP grows to $240,000 against $100,000 of static debt. Net equity is $140,000. As a result, the user earns $4,000 less than they would have by simply holding the raw 1 BTC and $100,000 crvUSD.

Yield Basis: As BTC climbs, the debt ratio drops below 50%. The vault automatically borrows more stablecoins to buy more BTC, compounding on the way up. The LP climbs to $288,000 against $144,000 in automated debt. Net equity is $144,000. The balance exactly matches the upside of holding 1 BTC, plus accumulated Curve swap fees.

Scenario 2: The Bear Case (BTC drops 36% to $64,000)

Standard LP (Amplified Loss): The pool buys falling BTC. The total LP shrinks to $160,000 against $100,000 of static debt. Net equity is $60,000. Consequently, the user loses an extra $4,000, suffering a worse drawdown than if they had simply held the 1 BTC and $100,000 crvUSD.

Yield Basis: As the price falls, the debt ratio threatens to spike past 50%. The vault automatically unwinds a fraction of the LP tokens and pays down the debt to shed exposure. The LP drops to $128,000 against a decreased debt of $64,000. Net equity is $64,000. The user suffers no impermanent loss penalty compared to holding the asset.

The Engine Behind crvUSD

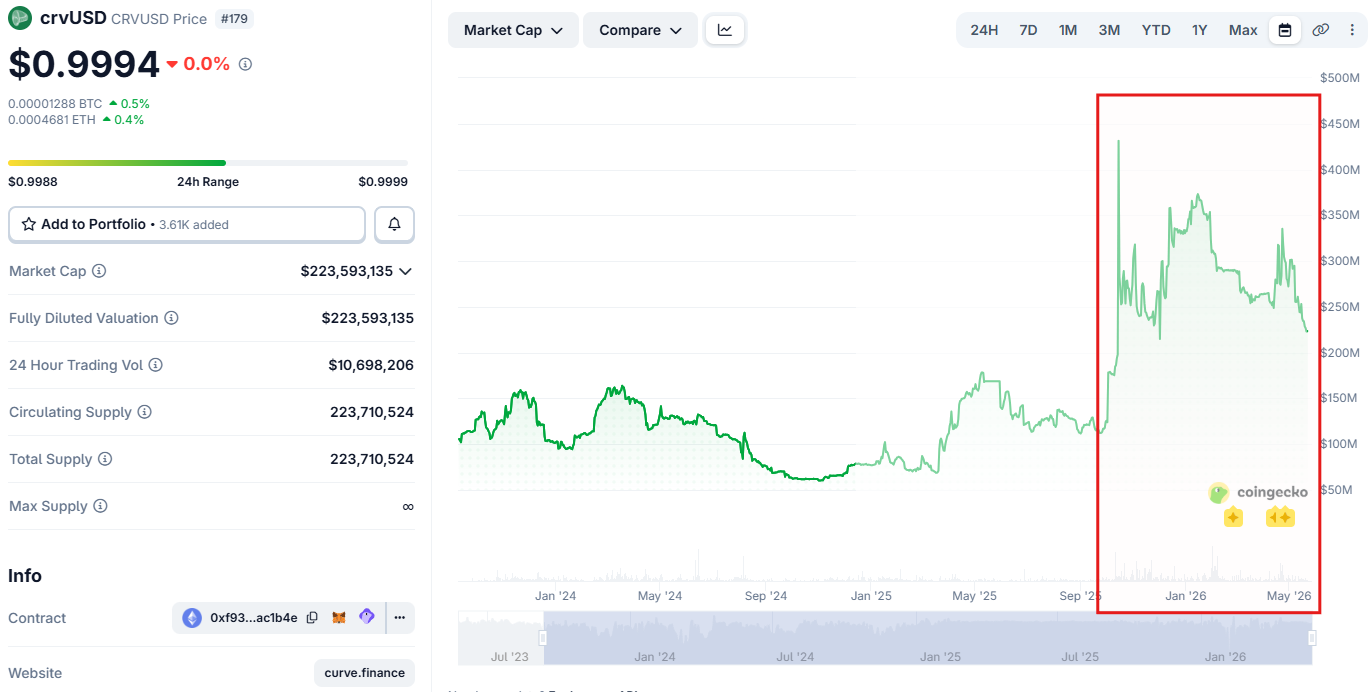

Yield Basis is intertwined with the scale of crvUSD. Because it exclusively borrows crvUSD to fuel its 2x leverage engine, it acts as a massive supply sink. The protocol borrows millions in crvUSD but pairs it immediately into liquidity pools instead of selling it on the open market, allowing Curve to theoretically scale its stablecoin supply infinitely. Since the launch of YieldBasis in September 2025, the market cap of crvUSD is up 200% (>300% at its peak).

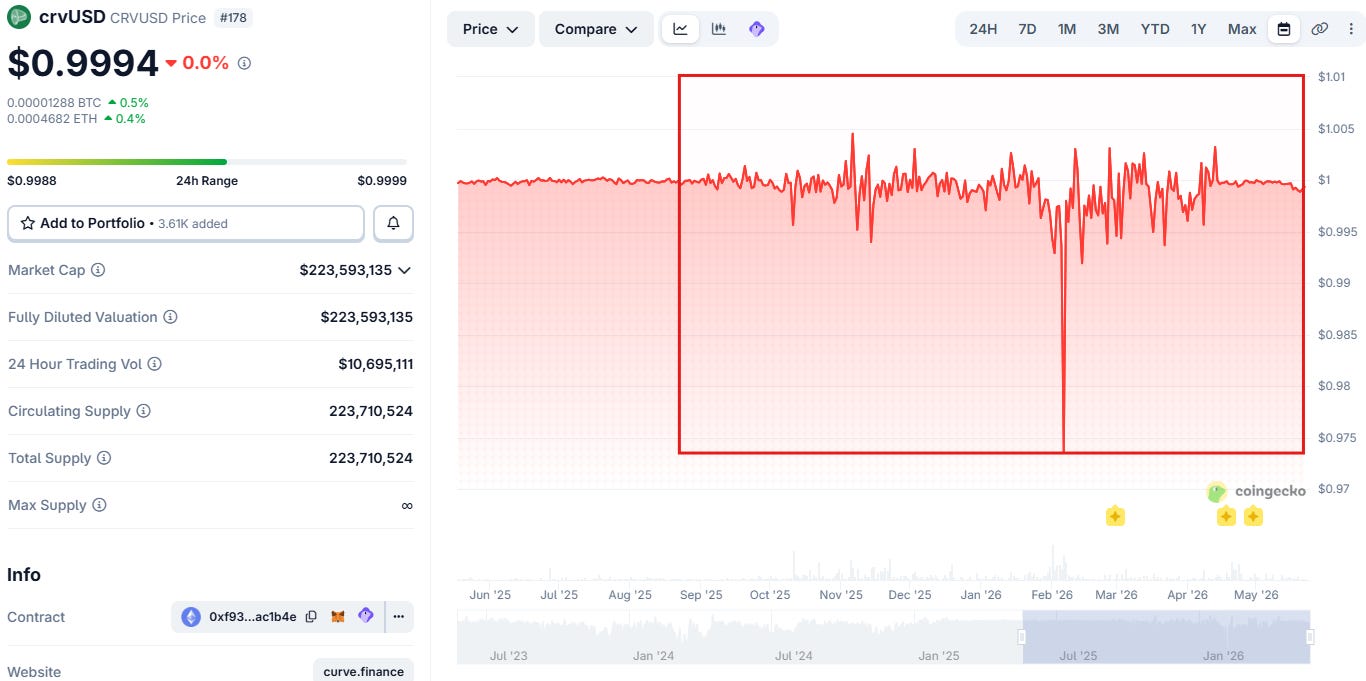

The Exception: Structural Peg Pressure

While Yield Basis is long-term supportive of crvUSD, it can make the peg highly volatile in the short term. Because Yield Basis’s BTC and ETH pools on Curve have become massive routing hubs for the broader market, they process enormous directional flows (e.g., swapping BTC to crvUSD to exit into USDC).

When the broader crypto market crashes, massive panic-selling of BTC and ETH is routed through crvUSD. Yield Basis, functioning more as a taker than a two-sided market maker, executes huge, one-sided “wrong-way” flows—selling crvUSD exactly when the stablecoin is already trading slightly below its peg. This forces Curve’s PegKeeper reserves to work overtime to absorb the sell pressure. To prevent Yield Basis from completely draining these reserves during a crash, it operates under a liquidity-anchored credit cap, ensuring its total size remains proportional to Curve’s available stablecoin defenses.

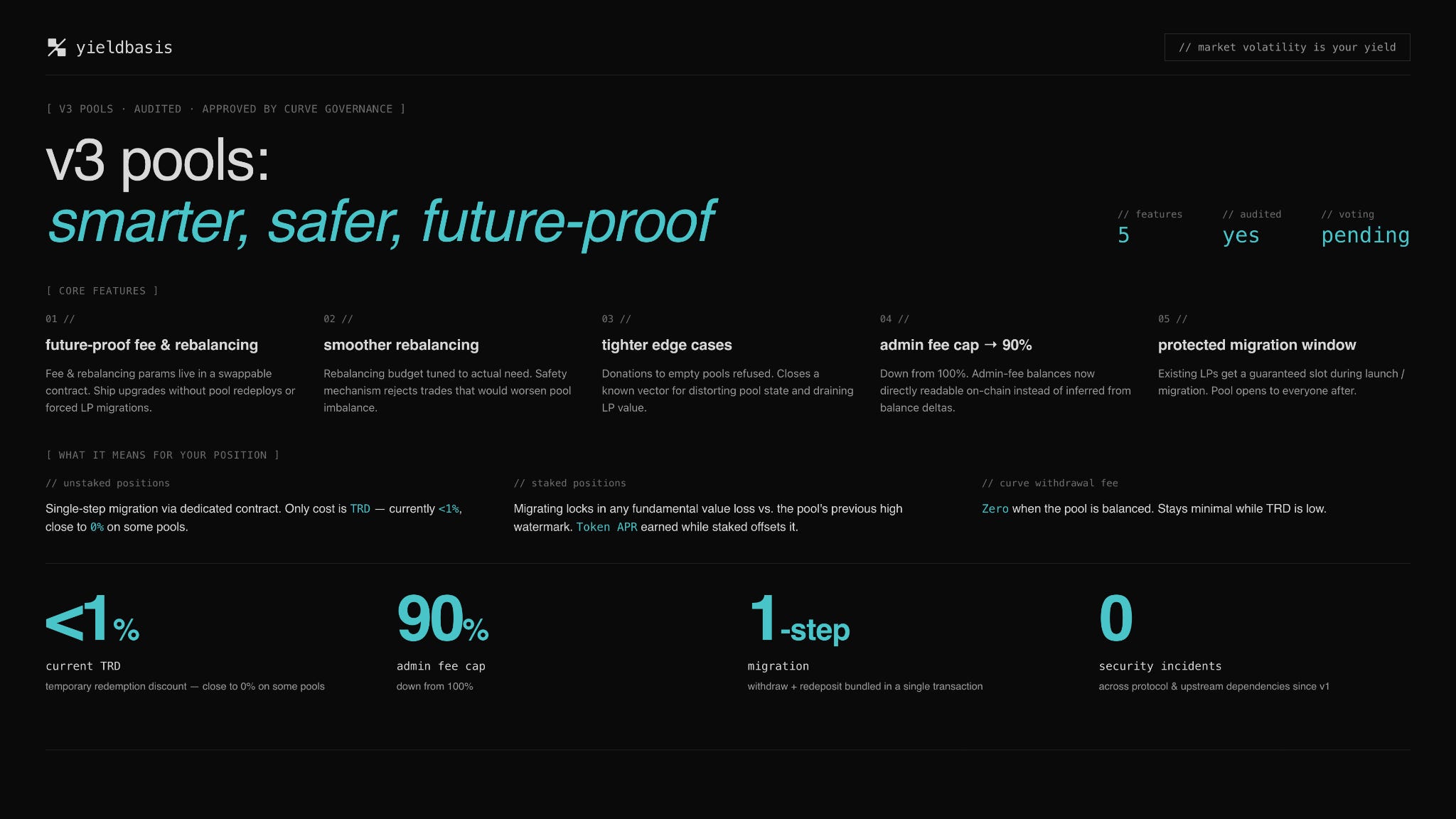

The Next Evolution: Yield Basis v3

To address scaling limits and optimize performance under market stress, the protocol is preparing to roll out Yield Basis v3. Key architectural changes include:

Hybrid Vaults: Moving beyond single-asset volatile collateral, v3 introduces Hybrid Vaults that accept a diverse basket of assets to spread risk and scale Total Value Locked (TVL) safely.

Faster TRD Recovery: By optimizing the rebalancing algorithms, v3 aims to drastically shorten the time it takes for temporary pool imbalances (TRDs) to heal back to their 1:1 spot track following severe market volatility.

Capital Efficiency: By migrating to new Curve pool invariants and fine-tuning arbitrage parameters, the protocol will require less aggressive flash-borrowing, theoretically resulting in higher baseline yields and lower friction.

Risk Warnings and Risk Factors

While Yield Basis mitigates impermanent loss, it replaces it with a different set of structural and systemic risks. This protocol is not risk-free.

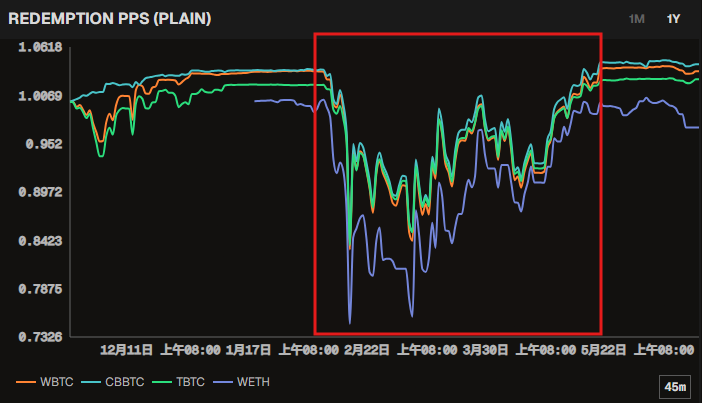

Temporary Redemption Discount (TRD) Risk: This is the most prevalent risk for LPs. When BTC or ETH crashes aggressively, everyone in the market is selling and there is a severe lack of buyers. Because Yield Basis cannot instantly find counterparties to sell into, the automated rebalancing mechanism lags behind the spot price. This liquidity bottleneck causes the LP value to temporarily trade below the 1:1 spot track—known as a TRD. (For context, a recent severe market downturn triggered a ~17% TRD that took several weeks to fully heal). If a user is forced to withdraw during this lag period, they will realize a permanent loss relative to holding the underlying asset.

crvUSD De-Peg Risk: The entire system relies on crvUSD maintaining its $1 peg. If crvUSD severely de-pegs, the underlying debt dynamics of the 2x leverage loop will break, potentially leading to catastrophic losses for Yield Basis LPs.

Smart Contract & Oracle Risk: Yield Basis operates on complex, multi-layered smart contracts interacting with Curve pools, LlamaLend CDP mechanisms, and price oracles. A vulnerability in any of these layers could result in a total loss of deposited funds.

Yield Sustainability: A portion of the protocol’s high initial yields may be subsidized by the emission of its native $YB token rather than organic trading volume. If the value of the $YB token declines or trading volume dries up, the effective APR for LPs will drop significantly.

Liquidity Risk: Exiting a large Yield Basis position requires sufficient liquidity in the underlying Curve pools. During periods of extreme network congestion or low liquidity, users may face high slippage when unwinding their leveraged LP tokens.

Yield Opportunities - up to 12% APR

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.