Intro to Yield Tranching - Royco Dawn

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

In this article, we break down how risk tranching works, why Royco Dawn matters, and how DeFi users can choose between safer yield and higher-risk, higher-return exposure.

Intro to Risk Tranching

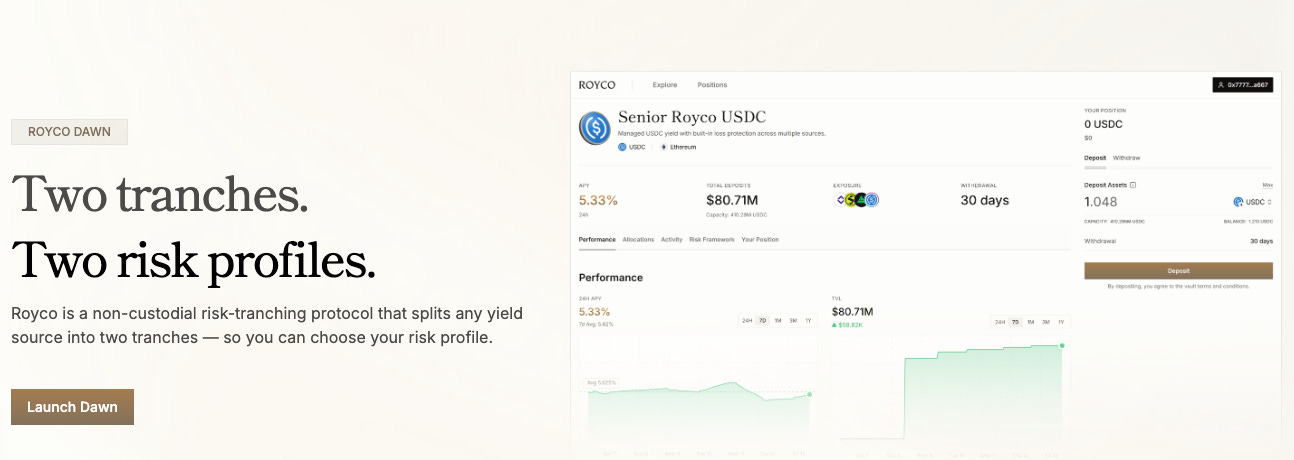

Royco Dawn Overview

Senior and Junior Tranches

Key Concepts and Variables

- Risk Premium

- Coverage Ratio

- Junior Leverage Ratio

- How Yields are Distributed

- What happens When Things Go Wrong

- Withdrawal Rules

Live Markets and Farming Opportunities

General Risk Notice

Royco Dawn vs. Strata Comparison

Imagine you and a friend put money into the same savings jar. It earns interest, but it can also lose money if something goes wrong. Risk tranching changes how that profit and loss is shared.

One person takes the safer “senior” side: lower yield, but more protection. The other takes the riskier “junior” side: higher potential yield, but they absorb losses first.

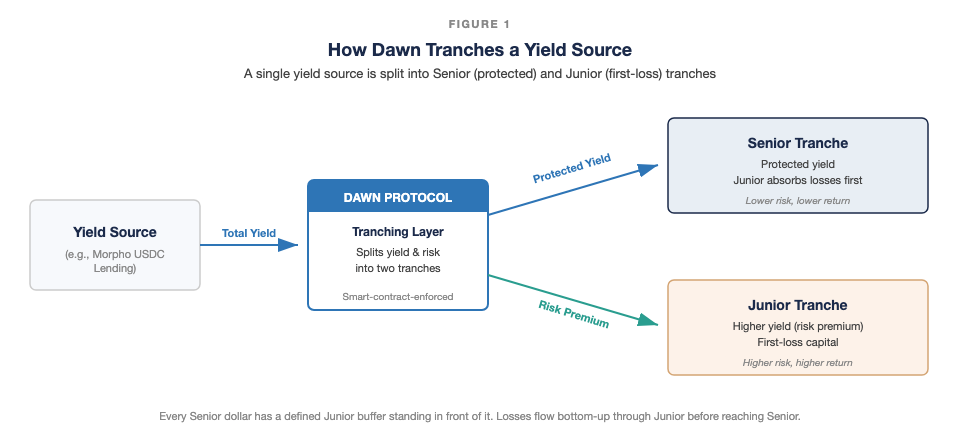

That’s the basic idea. One pool of capital, in this case a yield-bearing stablecoin strategy, is split into two layers with different risk and return rules.

This structure has existed in traditional finance for decades across mortgages, loans, and bonds. Royco Dawn and Strata bring the same concept on-chain, where smart contracts automatically enforce who earns first, who takes losses first, and how yield is distributed.

Protocol Deep-Dive: Royco Dawn

Royco Dawn launched in April 2026. It is designed as a permissionless tranching infrastructure — meaning any yield source (a lending market, staking deposit, RWA fund, or off-chain strategy) can be structured into Senior and Junior tranches. Each market on Royco has its own independently configured parameters.

SENIOR TRANCHE — The Safer Layer

The Senior earns a steady yield. If anything goes wrong with the strategy, Junior money takes the hit first. Senior is only ever touched once every single dollar of Junior capital has been used up. In exchange for this safety, Senior gives up some yield to Junior.

Suited for: Anyone who wants to earn yield but wants a clear buffer protecting their money — conservative savers, institutions, or anyone who cannot afford to take a big loss.

JUNIOR TRANCHE — The Riskier Layer

This is the front row — louder, more exciting, but you’re the first one in the mosh pit. Junior earns more yield than Senior, but Junior money is the first to be used up if anything goes wrong. In exchange for taking on that risk, Junior gets paid a bonus on top of the base yield — called the risk premium — as compensation. More reward, but real exposure.

Suited for: Yield-seekers who are comfortable with higher risk in exchange for higher returns, and who understand they could lose a significant portion of their deposit.

Key Concepts and Variables:

Risk Premium: What Junior Gets Paid for Taking Risk

The risk premium is the extra yield that Senior pays to Junior as a reward for agreeing to take losses first. Think of it like an insurance payment. Senior is effectively buying protection from Junior, and the risk premium is the price of that insurance.

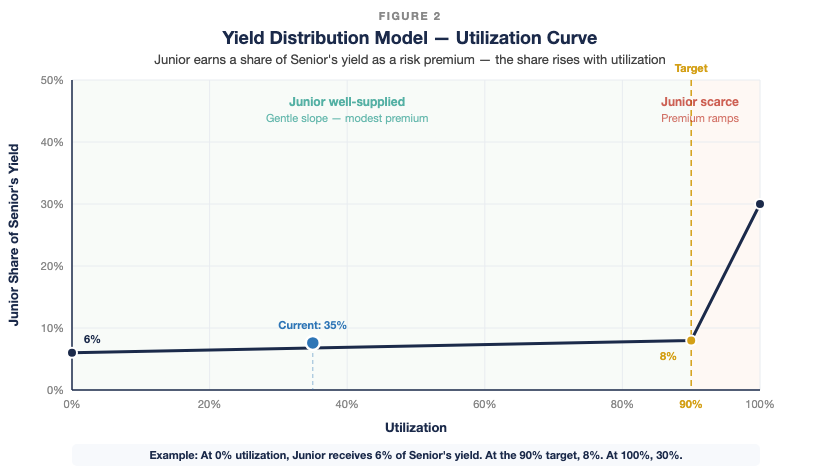

The premium is not fixed. It moves automatically with utilization:

When there is not much Junior money in the pool relative to Senior money > the premium goes up to attract more Junior depositors.

When there is plenty of Junior money > the premium goes down.

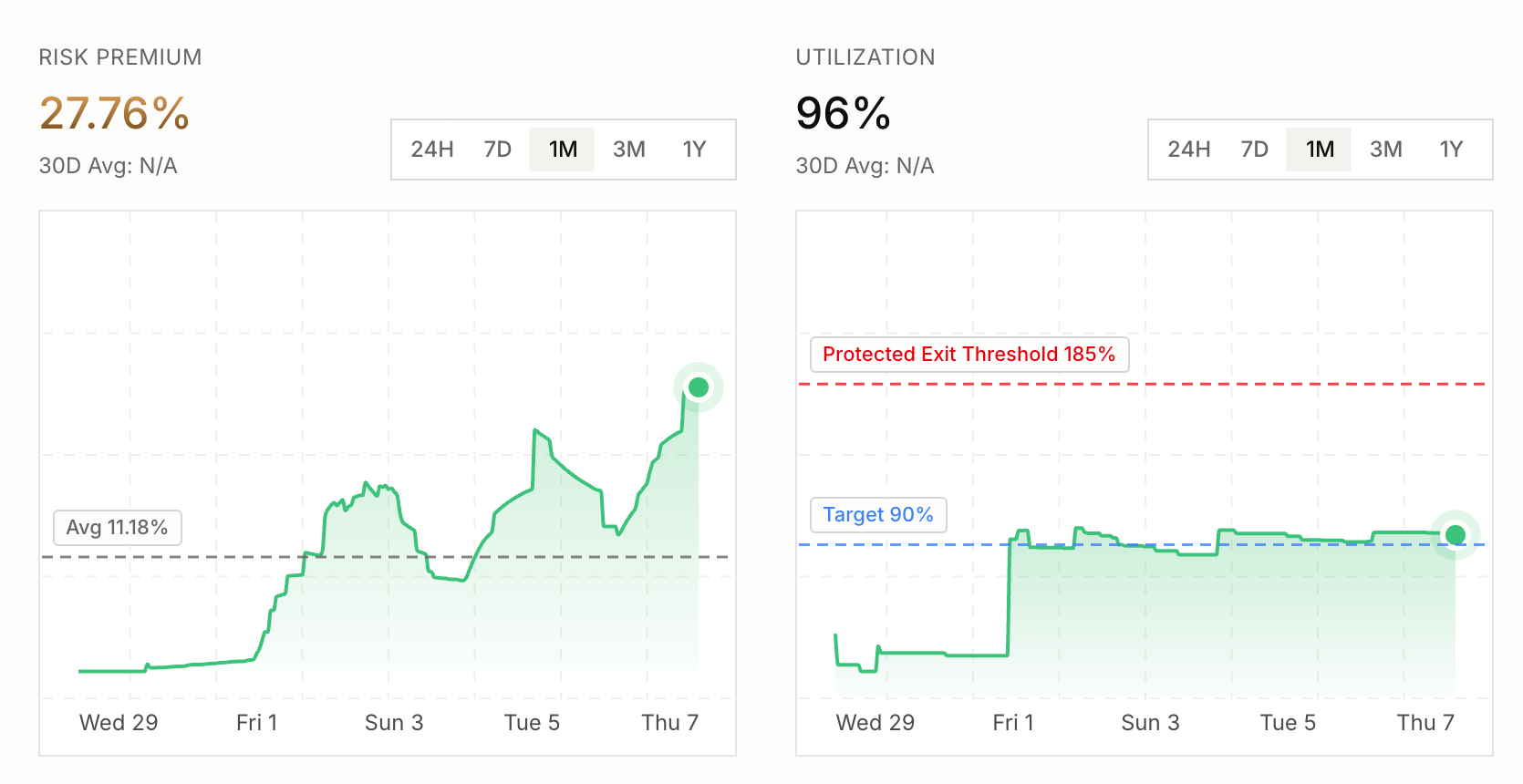

In this case, risk premium on the junior tranche page is 27%(with the 7-day average: 11.18%). This means Senior is paying 27.76% of its yield over to Junior as compensation. The current utilization is 96% (derived from 15/15.68%), meaning Junior capital is almost fully stretched backing Senior deposits. That is why the premium is elevated compared to the 7-day average: Junior is scarce, so it is being paid more to stay.

Why the Risk Premium Looks Different for Senior vs Junior

The risk premium is the same number — it’s just being expressed from two different angles.

Think of it like a salary and a bonus at a small company:

The company (Senior pool, $1.84M) pays out a $82,000 bonus pot (4.46% of its value)

The bonus recipient (Junior pool, $342K) receives that same $82,000 — but because their “salary base” is only $342K, the $82,000 represents a 27%+ boost to their earnings

Same dollar amount flowing. Totally different percentages depending on which side of the pool you’re measuring from.

In the apyUSD market concretely:

Senior pays ~4.46% of $1.84M = ~$82K per year flowing to Junior

Junior receives that ~$82K on top of its own $342K base = ~27% additional yield on their capital

Junior’s total APY = base yield (~8%) + that ~27% bonus = ~32–40%+ depending on the day

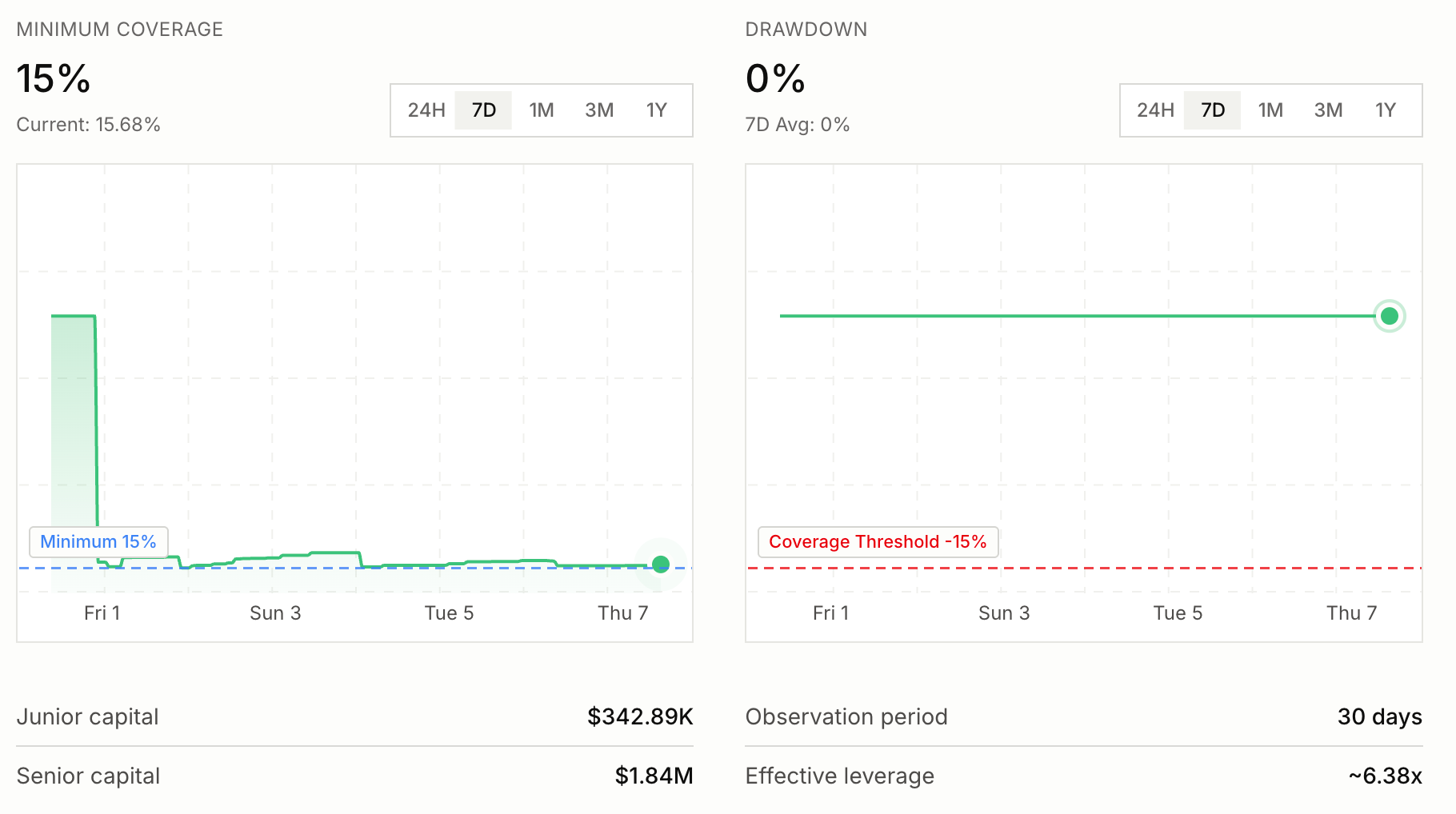

Coverage Ratio — The Safety Buffer

The coverage ratio tells you how much of a loss the strategy can take before Senior depositors are affected at all. It is calculated as the percentage of the total pool that Junior capital represents.

Coverage = Junior Capital ÷ Total Pool Assets × 100

If the strategy loses money — say a hack, bad debt, or a sustained drop in the asset — that loss comes out of Junior’s pocket first. Senior only starts losing money once Junior has been completely wiped out. The higher the coverage ratio, the bigger the safety buffer for Senior.

From the apyUSD market right now (May 2026):

Junior capital = $342,890. Senior capital = $1,840,000.

Total pool = ~$2,182,890.

Coverage = 342,890 ÷ 2,182,890 = 15.68%

Right above the required minimum of 15%. This means the strategy would need to lose 15.7% of its total value before any Senior depositor is affected. The protocol enforces this minimum by smart contract: if coverage ever dips below 15%, no new Senior deposits are accepted until Junior capital refills the buffer, and withdrawal is paused will utilization is >100% or coverage below 15%

Junior’s Leverage — Why Junior Wins Big and Loses Big

Because Junior is only a fraction of the total pool but absorbs 100% of the losses, even a modest loss on the overall pool translates to a much larger loss for Junior specifically. This is automatic leverage — Junior did not borrow anything, but the math of absorbing losses for a pool much larger than itself creates the same effect.

Junior Leverage = 1 ÷ Coverage Ratio

From the apyUSD market right now (May 2026):

Coverage is 15.68%, so Junior leverage = 1 ÷ 0.1568 = 6.38x.

If the underlying strategy(APYX’s apyUSD) drops 2% in total value, Junior capital drops by 2% × 6.38 = roughly 12.75%. That same 2% loss does not touch Senior at all.

This leverage works in both directions — when the strategy performs well, Junior earns a disproportionately large share of the upside too. This is why the Junior tranche on this market is currently offering 40.61% APY while Senior is at 8.31%.

How Yield Is Shared — When Things Go Well

Both Senior and Junior put their money into the same underlying strategy — in this case, apyUSD, which generates yield from preferred equity dividends. The yield is then split between them by the protocol automatically.

Senior gets the base yield minus the risk premium it pays to Junior. Junior gets the base yield plus the risk premium it receives from Senior. Because Junior’s share of the premium is earned on a much smaller pot of money, the percentage return for Junior ends up much higher.

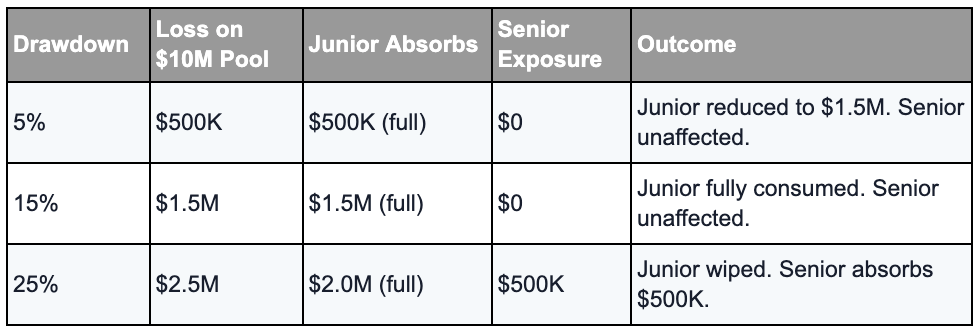

What Happens When Things Go Wrong — The Loss Waterfall

If the underlying strategy loses money through a hack, bad debt, or a sustained decline in asset value, the loss is absorbed in a strict order. Junior takes every dollar of loss first. Senior sits untouched until Junior is fully gone.

The table below shows how this plays out at different loss levels using a simple $10M pool example with 20% Junior coverage ($2M Junior, $8M Senior):

The Observation Period — a cooling-off window (Royco Dawn):

Markets can have temporary dips that recover on their own — a price blip, a brief liquidity crunch. Royco Dawn has a built-in waiting period before it finalizes any loss.

For the apyUSD market, this window is 30 days. If the strategy recovers within 30 days, no loss is recorded — it was just noise. During this window, Senior withdrawals are paused and all yield is redirected to Junior to help refill the buffer. If the drawdown does not recover within 30 days, Junior absorbs the loss permanently.

This protects Junior depositors from being penalized for temporary volatility that would have resolved itself.

When Can You Withdraw?

Withdrawal depends on your tranche and current utilization. For apyUSD, the pool must always keep at least 15% junior coverage, so no withdrawal can happen if it pushes coverage below that floor.

Senior withdrawals are usually available immediately, but pause during an Observation Period when a drawdown is being monitored. The exception is the Protected Exit Threshold: if utilization reaches 185%, senior can exit even during the Observation Period. However, apxUSD itself has a 20-day unstaking window, so converting back to USDC may still take time.

Junior withdrawals are only available when there is excess junior capital above the 15% coverage minimum. If utilization is too high, junior capital is fully backing senior depositors and cannot leave until senior exits or new junior capital enters. New junior deposits are also blocked during an Observation Period.

Right now, apyUSD utilization is around 96%, with coverage at 15.68%. That means junior liquidity is tight, and junior depositors may face restricted withdrawals until the pool has more breathing room.

What’s Live Right Now:

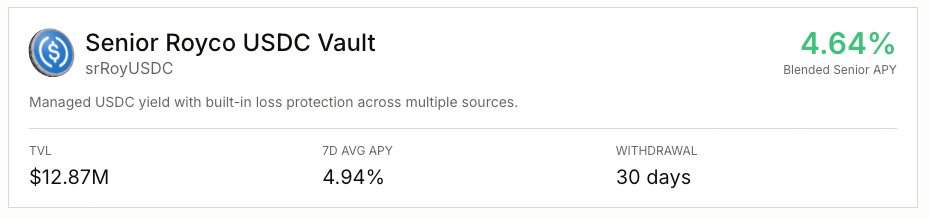

srRoyUSDC (Senior Vault)

Deposit USDC, receive a yield-bearing ERC-4626 token. Capital is allocated exclusively to Senior tranches across multiple yield sources. Protected yield, diversified across markets by Dialectic.

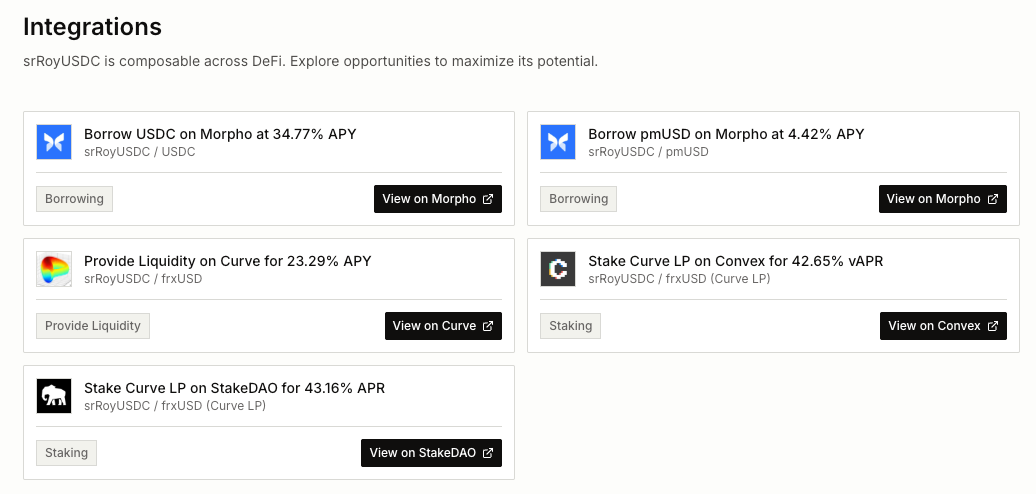

One of Royco’s recent developments is that srRoyUSDC is now composable, meaning you can use it inside other DeFi protocols to earn additional yield on top of what the vault already earns. These integrations are live as of the time of writing:

Borrow USDC on Morpho at 33.94% APY

Deposit srRoyUSDC as collateral, borrow USDC against it, and redeploy that USDC elsewhere. The effective yield on your original deposit can significantly exceed the vault’s base 4.64%.Borrow pmUSD on Morpho at 4.47% APY

A lower-cost borrowing option against the same collateral, useful if you want stable USDC-equivalent debt.Provide Liquidity on Curve for 23.20% APY

Pair srRoyUSDC with frxUSD in a Curve liquidity pool to earn trading fees and liquidity incentives.Stake Curve LP on Convex for 42.35% vAPR

Take the Curve LP token and stake it on Convex for boosted yield rewards on top of the Curve fees.

Risk stacking warning: Each additional protocol layer in a composability strategy adds its own smart contract risk, liquidation risk, and liquidity risk. A position that is simultaneously exposed to Royco (tranche mechanics) and Morpho (lending) carries more independent failure surfaces. Looping on Morpho, for example, can be liquidated if the strategies under srRoyUSDC price deviates from expected value.

Individual Markets on Royco(per May 2026)

The apyUSD market at 96% utilization means Junior capital is almost fully stretched. This is why its current Senior APY (8.31%) is above its 7-day average (9.01% — yes, it was higher last week) and why the Junior APY (40.23%) is well above its 7-day average (26.44%).

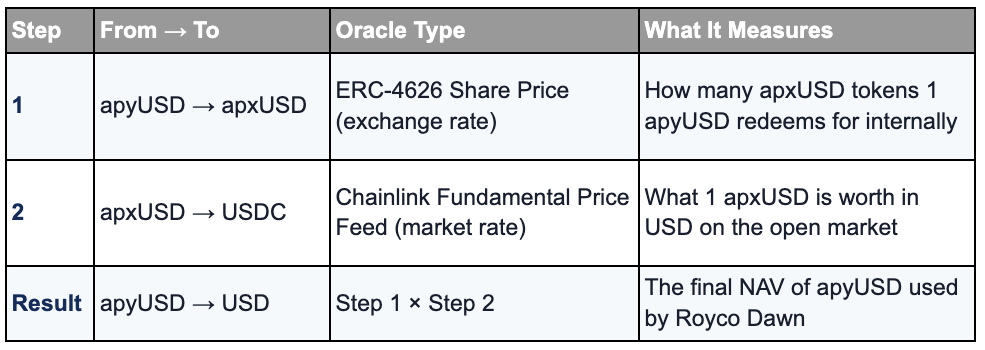

The Oracle Chain — How apyUSD Is Priced

apyUSD is not priced directly against USDC. Royco Dawn uses a two-step oracle chain:

Key Risks From The apyUSD Market

apyUSD is priced through apxUSD, so any discount in apxUSD’s market price, or any loss in Apyx’s underlying collateral such as STRC or SATA, can lower apyUSD’s NAV and trigger Royco Dawn’s loss mechanism.

If apxUSD trades below $1, the Chainlink oracle reflects that discount and apyUSD is marked lower, even if the underlying assets are still healthy. If Apyx’s collateral value falls below 100%, the risk is more direct: apxUSD may no longer be fully backed, causing apyUSD to depeg.

Junior depositors absorb these losses first. If the loss persists beyond the 30-day Observation Period, the writedown becomes permanent. At current conditions, with 96% utilization and only 15.68% coverage, Junior has very little buffer before Senior capital becomes exposed.

Risks Associated with Royco Dawn:

Smart contract risk — bugs or exploits in Royco Dawn’s infrastructure. Mitigated by audits from Hexens, Certora, and Cantina, plus a $250K Immunefi bug bounty.

Underlying strategy risk — if the yield source (e.g., apyUSD/apxUSD) suffers a hack, bad debt, or default, the Dawn market is affected. Junior absorbs first.

Junior exhaustion — if losses exceed Junior’s buffer and persist beyond the Observation Period, Senior capital is exposed to the remainder.

Oracle risk — the protocol relies on Chainlink and ERC-4626 share price oracles. Manipulation or failure could cause incorrect valuations.

Liquidity risk — underlying asset illiquidity (e.g., 20-day unstaking for apxUSD) can delay withdrawals even when the tranche protocol itself would allow them immediately.

Curator risk — Dialectic, as vault curator for srRoyUSDC, has operational control over which markets to allocate to. Poor decisions or delayed responses to risk events could affect vault performance.

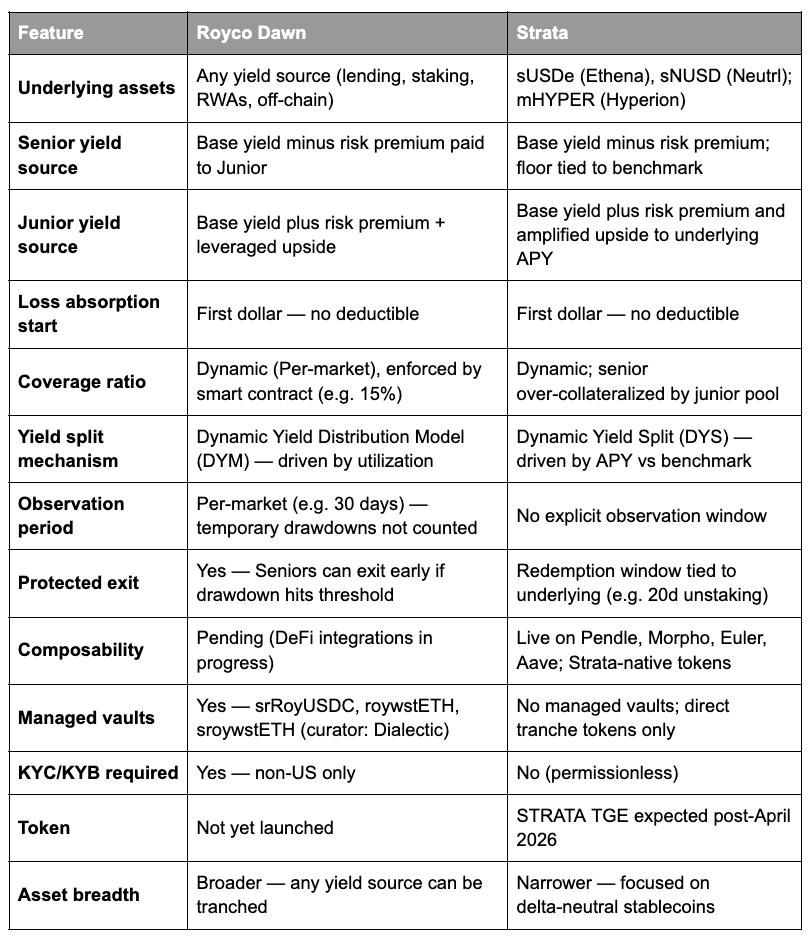

Comparing Royco Dawn vs. Strata

Both protocols implement senior/junior risk tranching on DeFi yield strategies. Their mechanics are similar in concept but meaningfully different in architecture, asset breadth, and maturity. The table below highlights the most important distinctions.

Royco Dawn is designed as a permissionless tranching launchpad, any yield source can be structured as a Dawn market, with each market having its own independently configured coverage ratio, observation period, and yield curve.

Strata is an opinionated tranching protocol built around specific yield assets (initially sUSDe), with a unified DYS mechanism. Royco’s broader asset scope and institutional-grade curator model give it a larger addressable market.

Since Strata launched earlier, it has deeper DeFi composability (Pendle, Morpho, Aave integrations already live) gives it a head start in the DeFi-native ecosystem.

‼️Disclaimer

This article is for informational purposes only and does not constitute investment advice. Participation in DeFi protocols involves risk, including the potential loss of all capital deployed. Protocol mechanics, APYs, TVL figures, and fee structures are subject to change. Always conduct independent due diligence and consult qualified legal, financial, and tax advisors before making any investment decisions.

For sponsorships, questions, or news tips, reach us at: support@todayindefi.com

Stablecoin LP-ing for 21% APY

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.