Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Headlines:

- Echo opens eBTC exploit claims

- Midas launches tokenized debt fund

- Zest sets Season 1 claim deadline

- Magic Eden faces a class action lawsuit

- ENS treasury proposal faces backlash

- ERC-4626 vault exploited on Base

- Derive’s upcoming V3 expands into RWA options

- Re Protocol opens RE governance

- Ansem airdrop sparks distribution debate

- Strategy unveils $1.25B Bitcoin sale plan

Key Takeaways:

1. The macro backdrop is improving, but crypto hasn’t followed.

The 2-year eased with May’s PCE likely the inflation peak, and Strategy’s new capital framework shored up the credit behind the largest corporate BTC holder — yet BTC/NQ still printed a fresh low, capital favoring tech over crypto. Conditions are turning; the flows aren’t.

2. Few chains grew against a contracting market

Base’s growth came entirely from Ethena’s USDe via the Coinbase–Steakhouse yield vault; XRPL’s from RLUSD on Mastercard’s settlement integrations. Distribution deals, not broad risk appetite — the chain-by-chain breakdown is in Section 3.

3. Capital went to onchain credit; New catalysts are lining up

Maple drew $240M in deposits this week — against falling prices — on a first-of-its-kind deal with Kraken. And Derive is taking its onchain options into real-world assets, with founder Nick Forster outlining a v3 expansion.

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

1A. Traditional Macro

US 2Y yield

US 2Y yield: 4.10%, −1.99% WoW. EASING — the week’s relief. After spiking to roughly 4.18% on the hawkish FOMC, the 2-year corrected lower this week.

The driver is the inflation outlook flipping forward: May PCE came in hot at 4.1% headline and 3.4% core, both multi-year highs, but it’s widely read as the peak because crude has since collapsed and that disinflation isn’t in the data yet. The front end is beginning to price that the inflation scare rolls over from here.

Still above the 20W MA, so not a regime change — but a genuine relief after weeks of pressure.

BTC/NQ ratio

BTC/NQ ratio: another yearly low. WEAK — crypto-specific. The ratio printed a fresh 2026 low, meaning capital is still rotating toward tech equities over crypto. Even with oil falling and rates easing, crypto is underperforming — pressured by the strong dollar, contracting liquidity, and a second wave of ETF outflows that pulled Bitcoin near $59,400.

Two forces shaped the week. The war kept de-escalating — oil fell again as Gulf supply came back online — while the rate picture stayed the binding constraint, though the front end of the curve finally eased.

The net: macro headwinds are softening at the margin, but crypto isn’t participating. The dollar pushed to another yearly high and crypto printed a fresh relative low against tech.

Supporting context — the war keeps fading

Oil fell again, even through fresh strikes — and that’s the signal. Brent dropped to around $72 on Friday, the lowest since February 27 and a 10%+ weekly fall, as Strait of Hormuz traffic accelerated and Gulf exports recovered to roughly 75% of pre-war levels, with Saudi Arabia, the UAE, Kuwait and Qatar all ramping supply.

The ceasefire is still bumpy — Trump posted that US aircraft struck Iranian missile, drone, and coastal radar sites for again violating the agreement — yet oil traded lower anyway. That falling-oil backdrop is exactly the disinflation the 2-year started to price this week.

A note on Bitcoin’s credit backdrop.

Strategy (MSTR) unveiled a Digital Credit Capital Framework on June 29 — a $2.55B USD reserve (~17 months of preferred-dividend coverage, ~26 months including authorized BTC monetization), a STRC dividend lifted to 12%, and $1B buyback programs for both its digital-credit securities and common stock.

The practical effect is that it shores up STRC and the credit stack behind the largest corporate Bitcoin holder, reducing a latent forced-seller tail risk around BTC — though, with the funding mechanism being potential BTC sales and the price barely reacting, the market read it as risk reduction, not a catalyst.

Composite: liquidity contracting

The dollar at yearly highs, the 2Y easing (the lone bright spot), and crypto at relative lows. The macro inputs are tentatively turning — rates correcting, oil down, the war fading — but the two levers that matter most for crypto, the dollar and liquidity, are still pointed the wrong way.

1B. Crypto Capital On-Ramp

Total stablecoin supply 7d change (level + WoW)

A sharp reversal from last week’s small +$0.27B print, and the supply base is shrinking again. One accuracy note on the framing — this isn’t quite the worst in weeks: June 1 (−$2.80B) and June 8 (−$3.65B) were deeper. But it’s the sharpest contraction in three weeks, and it erased the brief recovery.

The cause is concentrated in the two transactional giants: USDC bled −$1.11B and USDT −$1.38B, together −$2.49B — essentially the entire weekly drop. When the transactional dollars used for trading and settlement contract this hard in one week, it reads as capital stepping back, in line with the risk-off tape and the price correction. (The full composition split — including DAI’s +8% and the yield/RWA names — is in Section 2.)

ETF flows

ETF flows — the worst week of the year. Bitcoin −$1.787B, Ethereum −$273.5M, Solana −$1.9M for June 22–28, together roughly −$2.06B — the largest weekly outflow of 2026. This is now the seventh consecutive week of net outflows, and instead of exhausting, the selling accelerated to a yearly extreme. It’s the single biggest drag on the crypto tape this week and the clearest evidence institutional demand is still in retreat, not stabilizing.

Verdict: Onchain regime — COOLING / RISK-OFF.

The onchain picture moved in line with macro this week: transactional stablecoins contracted hard, ETHBTC failed its bounce, and the overall risk tone softened.

The one counter-signal is leverage — funding is building toward the borrow rate, with longs growing into the weakness, which is either early positioning for a turn or a setup that unwinds if the tape stays heavy.

1C. Week-Ahead Catalysts

⭐ Non-Farm Payrolls — Thursday, July 2. The one most likely to move the rate debate. Consensus is 110K, a sharp slowdown from May’s 172K, with unemployment seen holding at 4.3%. A

soft number would strengthen the case that the labor market is cooling enough to pull the Fed off its hawkish path; a hot one would reinforce the hike pricing that built through June.

Section 2 — Onchain Risk Regime

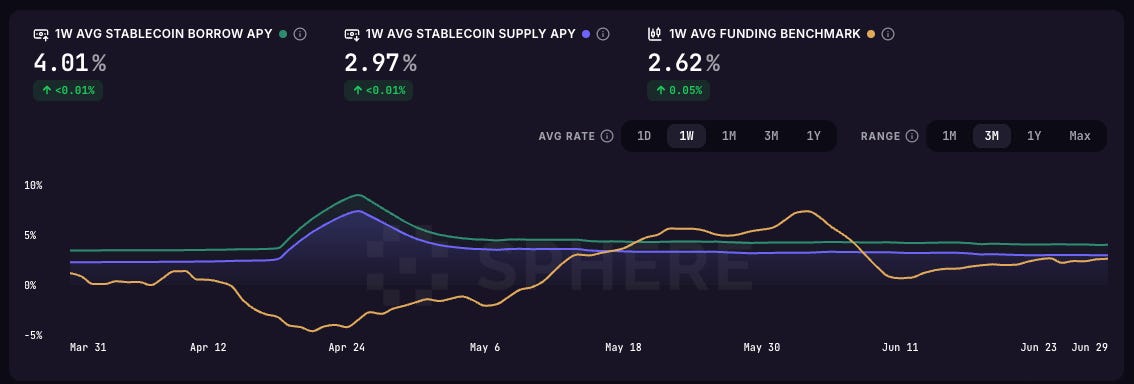

Aave / Sphere Rates

Borrow APY 4.01% and supply APY 2.97% were both essentially flat (each +0.01%). The mover, for a third straight week, was funding: the benchmark rose to 2.62% (+0.65%) — its sharpest weekly climb in the series — and is now closing in on the 4.01% borrow rate.

This is the week’s most interesting tension. Funding has now climbed steadily (1.73% → 2.13% → 2.62%) and is heading toward the borrow rate, which means leverage demand is building and longs are being added.

Funding still sits below borrow, so it’s not yet at greedy or crowded levels — but the direction is clear, and, notably, traders are adding leverage into a risk-off tape with crypto at relative lows. Either a contrarian build or early positioning for a turn. Worth flagging that if funding crosses the borrow rate, that’s the signal leverage has tipped from constructive to crowded.

ETHBTC

ETHBTC vs 20W MA — Downtrend stalling. After two green weeks and a marginal red candle (−0.41%), ETHBTC is no longer in the clean downtrend it held through the spring — it’s flattening into consolidation just below its 20-week moving average. Still unconfirmed (under the MA),

but a stalling ETHBTC matters beyond ETH: the ratio is a rough risk-on/off gauge for the whole alt complex, and with Solana already outperforming, a base here gives alts some room to move. Not a turn — but no longer “lower every week,” which is the relief the alt side has been waiting for.

Verdict: Onchain regime — COOLING / RISK-OFF.

The onchain picture moved in line with macro this week: transactional stablecoins contracted hard, ETHBTC failed its bounce, and the overall risk tone softened. The one counter-signal is leverage — funding is building toward the borrow rate, with longs growing into the weakness, which is either early positioning for a turn or a setup that unwinds if the tape stays heavy.

Section 3 — Chain Comparison

3A. Stablecoin flows by chain

The global on-chain stablecoin market closed the week at $312.6 billion, a decline of $2.16 billion (−0.69%) week-on-week and $8.0 billion (−2.49%) over the trailing 30 days. The headline contraction, however, masks a structurally bifurcated picture.

A small group of chains posted compounding gains against the market trend, each supported by a named, dated, and independently verifiable catalyst. In every instance, on-chain supply data confirms that the timing of inflows aligns with the announcement window.

Market Snapshot — Structural Gainers:

Monad - Total Supply: $458M - [7d: +8.09%] - [30d: +3.37%]

Monad was the strongest stablecoin growth story this week after Pendle launched AUSD pools on June 19 with up to $100K/week in incentives through October 2026. AUSD supply on Monad more than doubled from ~$33M to $72.7M in one week, now representing ~40% of global AUSD supply. Pendle currently offers up to 8.6% fixed APY on AUSD, making the incentives the primary driver to monitor.

Base - Total Supply: $4.89B - [7d: +0.32%] - [30d: +4.46%]

Headline growth was modest, but almost entirely driven by Ethena’s USDe (+14.7% 7d, +$23.5M). The catalyst is Coinbase’s new Steakhouse High Yield Vault, which routes user deposits into Morpho markets using USDe as collateral. Coinbase Ventures also accumulated ENA, making this one of the clearest institutional distribution catalysts in DeFi.

Coinbase Ventures purchased ENA from the open market to signal institutional alignment with the collaboration. The vault creates the first instance of Ethena’s yield infrastructure being accessible within a major CEX application, extending potential distribution to 100 million+ Coinbase users without requiring them to navigate a separate DeFi front end.

XRP Ledger - Total Supply: $818M - [7d: +4.29%] - [30d: +9.00%]

RLUSD continues to dominate XRPL after Mastercard expanded stablecoin settlement support to include RLUSD and later selected Ripple as a launch partner for Agent Pay, its AI-agent payments network. The investment thesis remains continued adoption of regulated payment stablecoins.

X-Layer (OKX) - Total Supply: $1.82B - [7d: +2.70%] - [30d: +22.77%]

USDG supply continues expanding following OKX's Exchange OS launch, which moves exchange infrastructure onchain and creates natural demand for USDG as margin and settlement collateral. Watch for additional Exchange OS applications to sustain growth.

Notable Losers

Ethereum’s USDT and USDC outflows remain gradual, suggesting capital rotation rather than panic selling.

Hyperliquid’s stablecoin decline appears driven by derivatives deleveraging instead of users leaving the ecosystem.

Tron’s slow USDT decline continues with no identifiable catalyst, likely reflecting rotation toward higher-yield alternatives.

Solana’s weekly decline appears temporary, given continued strength in on-chain activity and TVL.

3B. Structural Shifts

DeFi’s dominant theme this week is institutionalisation across every sector. The market is not pricing speculative rotation — it is pricing the infrastructure that professional capital requires to operate on-chain: perpetual trading venues, tokenised real-world assets, compliant stablecoins, and credit markets capable of underwriting institutional balance sheets.

Three structural bets emerge with cross-signal confirmation:

Perpetual DEXs

Perpetual trading remains the strongest sector. Hyperliquid processed over $50B in weekly volume while newer exchanges like Upscale, Avantis, tradeXYZ and dYdX continue gaining share. Token performance across HYPE, DYDX and JTO continues validating the theme.Tokenized Assets (RWA)

The biggest structural catalyst remains DTCC’s production launch of tokenized stocks, ETFs and Treasuries beginning July 2026. RWA protocols continue seeing rising TVL, fees and institutional participation, making this one of the highest-conviction medium-term narratives.Stablecoins

The GENIUS Act continues moving toward implementation, creating a regulatory framework for compliant stablecoin issuers. Protocols benefiting from compliant stablecoin adoption remain key beneficiaries into 2027.

Narrative of Strong Market Conviction - HIGH CONVICTION:

1. Perpetuals & Derivatives Infrastructure

Perpetual DEXs remain the strongest sector this week. Hyperliquid processed over $50B in 7-day volume while maintaining ~70% market share, with tradeXYZ (+18%), Upscale (+85%), Avantis (+48%), dYdX (+26%), and Jupiter Perps (+18%) all posting strong volume growth. The fact that multiple venues are expanding simultaneously suggests structural market growth rather than simple market-share rotation.

The token backdrop supports the trend, with DYDX (+34%) and JTO (+29%) among the week’s strongest performers. Hyperliquid’s fee-driven buyback mechanism continues linking protocol usage directly to token demand, while HIP-3 expands the protocol into permissionless perpetual markets for RWAs, including commodities and equities.

2. RWA / Tokenized Assets

Tokenized assets remain one of the clearest institutional themes. TVL continues growing across private credit, tokenized Treasuries, reinsurance, and institutional lending, while Securitize recorded the fastest fee growth among major protocols (+55% WoW). Tokenized stocks have grown from ~$375M to over $1.2B in one year.

The key catalyst is DTCC’s production launch of tokenized equities, ETFs, and Treasuries beginning in July, backed by over 50 institutions, including BlackRock, Goldman Sachs, JPMorgan, Circle, and Ondo. This remains one of the strongest medium-term catalysts for the sector.

Medium Conviction

3. Solana Ecosystem

Despite recent price weakness, Solana’s fundamentals remain healthy. Pump.fun, Jupiter, Meteora, and Jito continue generating strong fees, Jupiter Perps volume is rising, and daily active addresses remain near cycle highs.

The ecosystem continues benefiting from growing perpetual trading activity and remains one of the strongest high-beta plays if market sentiment improves.

4. Lending & Credit Markets

Lending continues showing strong fundamental momentum. Morpho posted the fastest fee growth among major lending protocols (+22% WoW), driven by institutional adoption and expanding RWA integration, while Aave continues benefiting from strong revenue generation, buyback expectations, and expansion into tokenized securities. The convergence of lending and RWAs remains one of DeFi’s most important structural trends.

Section 4 — Project & Protocol Discovery

4A. Token Price Movers - Observations, not trade ideas.

VELVET (+262.8%) led DeFi gains after integrating Aerodrome for deeper Base liquidity and launching chain abstraction, allowing users to move assets across Solana, Base, and BNB in a single flow.

SLX (+177.9%) surged following its Upbit listing, with over $100M traded in 24 hours, while investors also focused on aiUSX—its upcoming stablecoin designed to generate yield from AI compute demand rather than crypto funding rates.

DYDX (+34.1%) rallied ahead of a teased July 1 announcement, with markets positioning for what the team describes as a major new product or onchain-first launch.

JTO (+27.2%) gained after filing a B2 Token Transparency report, highlighting how protocol revenue flows to token holders through staking rewards, BAM fees, and historical buybacks.

AAVE (+20.3%) extended higher as the team unveiled plans for Aavenomics 3.0, including automated buybacks, reaffirmed that protocol and GHO revenue accrues to the token, and outlined V4’s expansion into tokenized securities.

DRV (+14.5%), which claims 90% of the onchain options market, is preparing v3 with plans to expand into RWA options across equities, metals, energy, and compute. The protocol recently printed its largest trade ever at $210M notional and runs buybacks funded by a third of revenue.

4B. TVL Gainers ($50M+ filter) — Ranked by absolute $ inflow.

ETH fell 8.61% ($1,726 → $1,578), BTC fell 6.34%, HYPE fell 6.00%, and SOL gained 1.04%. ETH-denominated protocols faced a significant valuation headwind, meaning every protocol below attracted net inflows despite falling asset prices. Stablecoin-native protocols — Maple, Sky, Dolomite — experienced zero price drag, making their TVL gains entirely deposit-driven.

Maple Finance — $2.37B | +$240M · ▲11.27%

Maple led TVL inflows after launching an onchain warehouse lending facility with Kraken on June 25. The USDC-denominated revolving credit facility enables institutional clients to borrow against BTC and ETH without selling, bringing TradFi-style warehouse financing fully onchain. The deal is one of the strongest institutional lending milestones in DeFi to date.

Supporting momentum came from Maple’s new Transparency dashboard and Borrower Hub upgrades, improving institutional visibility and borrower tooling.

Sky — $5.80B | +$185M · ▲3.30%

The architecture rests on Uniswap v4’s hook system. Spark acts as orchestration layer, governing allocation frameworks and risk parameters. The planned DualPool hook (pending separate security review before deployment) would allow idle capital to route into Sky ecosystem yield strategies rather than sit dormant — solving what the protocols describe as the liquidity-versus-productivity tradeoff. Phase 2 would expand to additional stablecoin issuers; Robinhood, Revolut, and bank-issued tokens have been cited as prospective participants, with USDS as the shared quoting asset.

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.