MicroStrategy Buys Bitcoin, Derive Earns Record Fees - Onchain Outlook

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Headlines:

- Yield Basis lowers vault collateral requirement

- Coinbase activates aqav2 on hyperliquid

- Circle launches bitcoin-backed cirbtc

- Makina season 3 rewards go live

- Tangent raises borrow caps 50%

- aerodrome lend relaunches on base

- Felix HIP-3 dex begins shutdown

- Humanity wallets drained, token crashes

- AFI Protocol hit by $480k exploit

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

Key Takaways:

1. MicroStrategy is buying Bitcoin again.

A new 8-K shows the company raised $181M through an ATM share sale and bought 1,550 BTC at an average $65,332 (~$101M), and also lifted cash to $1.0B. The signal cuts both ways: it signals MicroStrategy would rather accumulate than sell below its cost basis, and the cash raise signals support for STRC — but the $100M only extends its preferred-dividend runway by about a month, and the company has shifted from pure buyer to both buyer and seller, a source of latent sell pressure once BTC trades back above its cost basis.

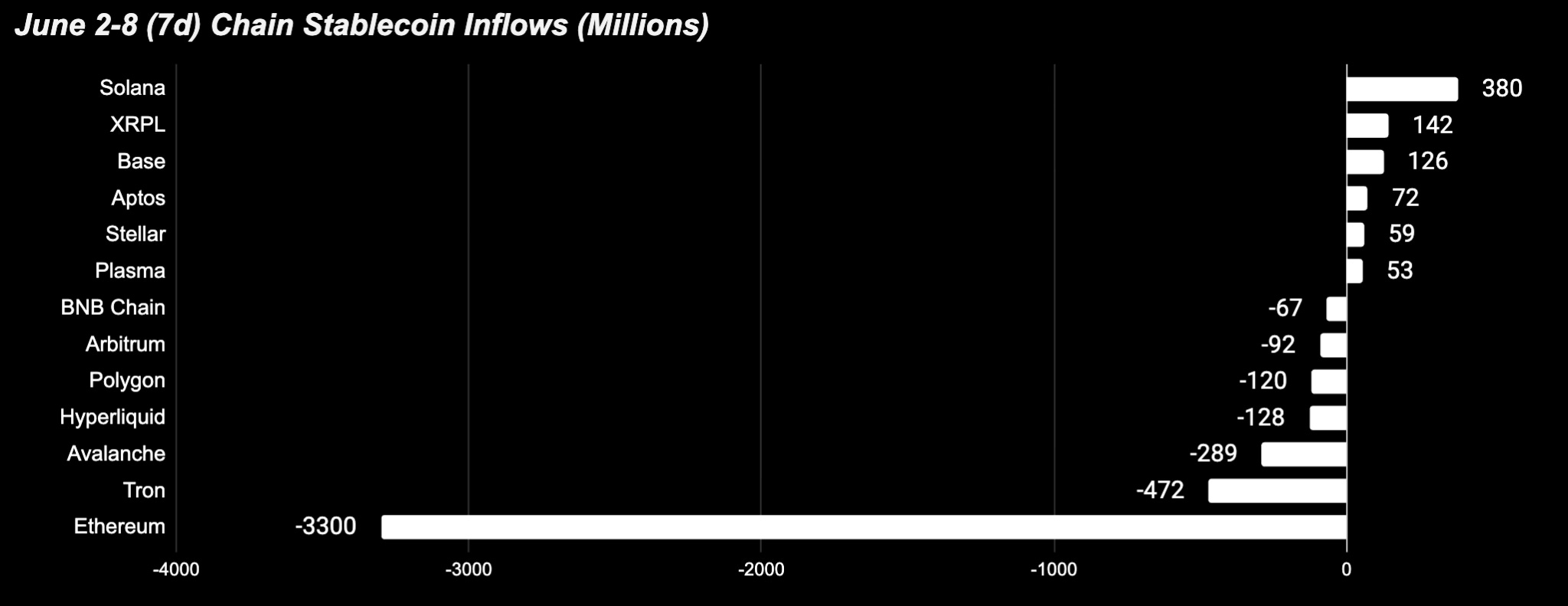

2. Solana, the outlier in the bleed.

Solana drew the largest stablecoin inflow of any chain (+$369.3M) and was the top DEX venue at $16.3B (+83.3% on the week), with institutional execution now driving volume in place of memecoins — Jump’s BisonFi (+177%), Orca, and cross-stablecoin settlement on Manifest. Ethereum did the opposite, shedding -$3.43B in stablecoins, its worst week of Q2 and 71.9% of all chain outflows, as capital migrates to purpose-built rails.

3. Derive outperforms the bleed.

Derive was the standout protocol in a defensive week, and for a structural reason: options are popular when volatility spikes, demand for hedging and optionality rises. The onchain options leader posted a record organic fee week (~$140K, its highest without incentives this year) on $707M of volume.

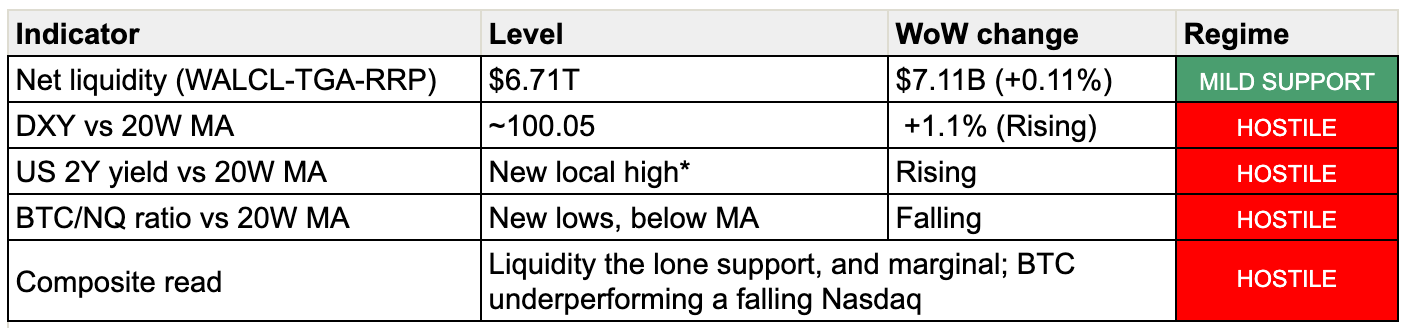

Section 1 — Macro + Capital Backdrop

MicroStrategy bought Bitcoin

For better or worse, the current Bitcoin narrative has been dominated by MicroStrategy’s balance sheet. Concerns about their balance sheet arose last week when MicroStrategy decided to buy back convertible debt with spare cash instead of reserving that cash for their preferred stock dividends like STRC.

This week’s 8-K showed that MicroStrategy sold MSTR shares through ATM to raise $181M. Along with some previously raised cash, this allowed them to buy 1,550 BTC at an average price of $65,332 (~$101M) and bring cash up to $1.0B.

While far from the $2B+ MSTR had before its debt buyback, this is a short-term mildly bullish catalyst for BTC as it shows MicroStrategy prefers to buy rather than sell below its average cost basis of $75,680 per BTC, and is also supportive of STRC as it shows MicroStrategy is prioritizing preferred over common.

However the bearish argument still stands that MicroStrategy has turned from a pure buyer to both buyer and seller — presumably creating sell pressure when bitcoin rises above its average cost of $75,680. Also the $100M treasury add only extends cash runway for preferred obligations by one month.

1A. Traditional Macro

US 2Y yield

US 2Y yield: new local high — HOSTILE. (Level/WoW to confirm — see flags.) The 2Y reversed last week’s bid and pressed back up, a direct weight on risk appetite.

BTC/NQ ratio

BTC/NQ ratio vs 20W MA: new lows, below the MA and falling — HOSTILE. The ratio is at its lowest in the visible range. Eventhough Nasdaq itself fell -4.53% (its first weekly red candle in two months), and yet BTC/NQ still declined — meaning BTC fell harder than a dropping Nasdaq. Capital continues to favor tech equities over crypto, and BTC is taking the higher-beta hit as AI-bubble fear spreads.

Composite read: hostile.

Liquidity is the lone support. The dollar index is ripping up, the 2Y is at a new high, and BTC is underperforming a market that is itself now selling off. Macro is not supporting risk, and the onchain picture (Section 2) tips the combined read hostile.

1B. Crypto Capital On-Ramp

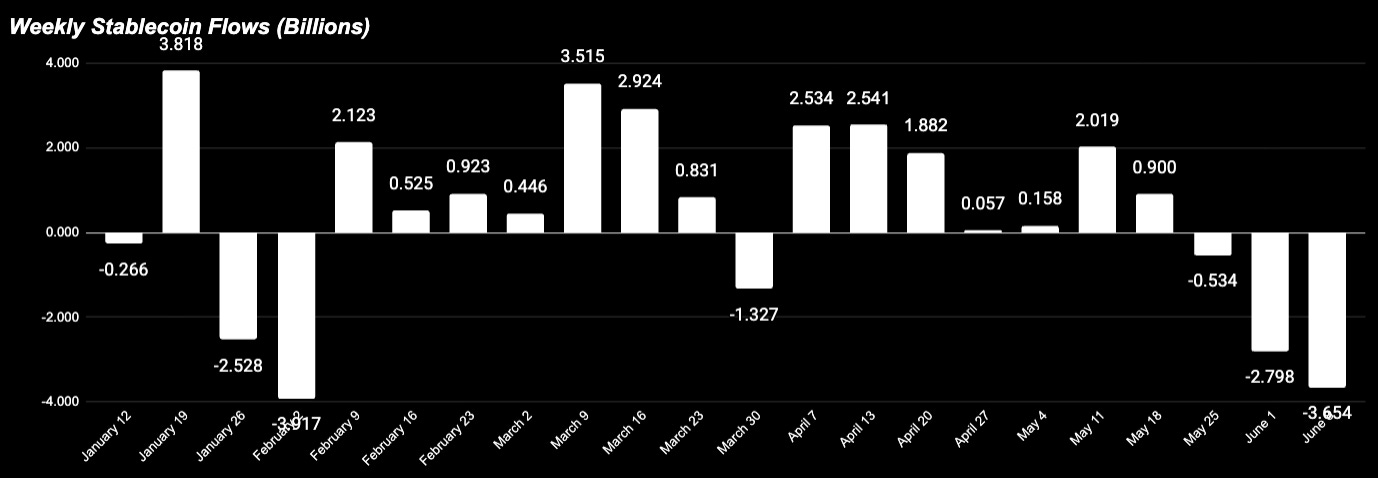

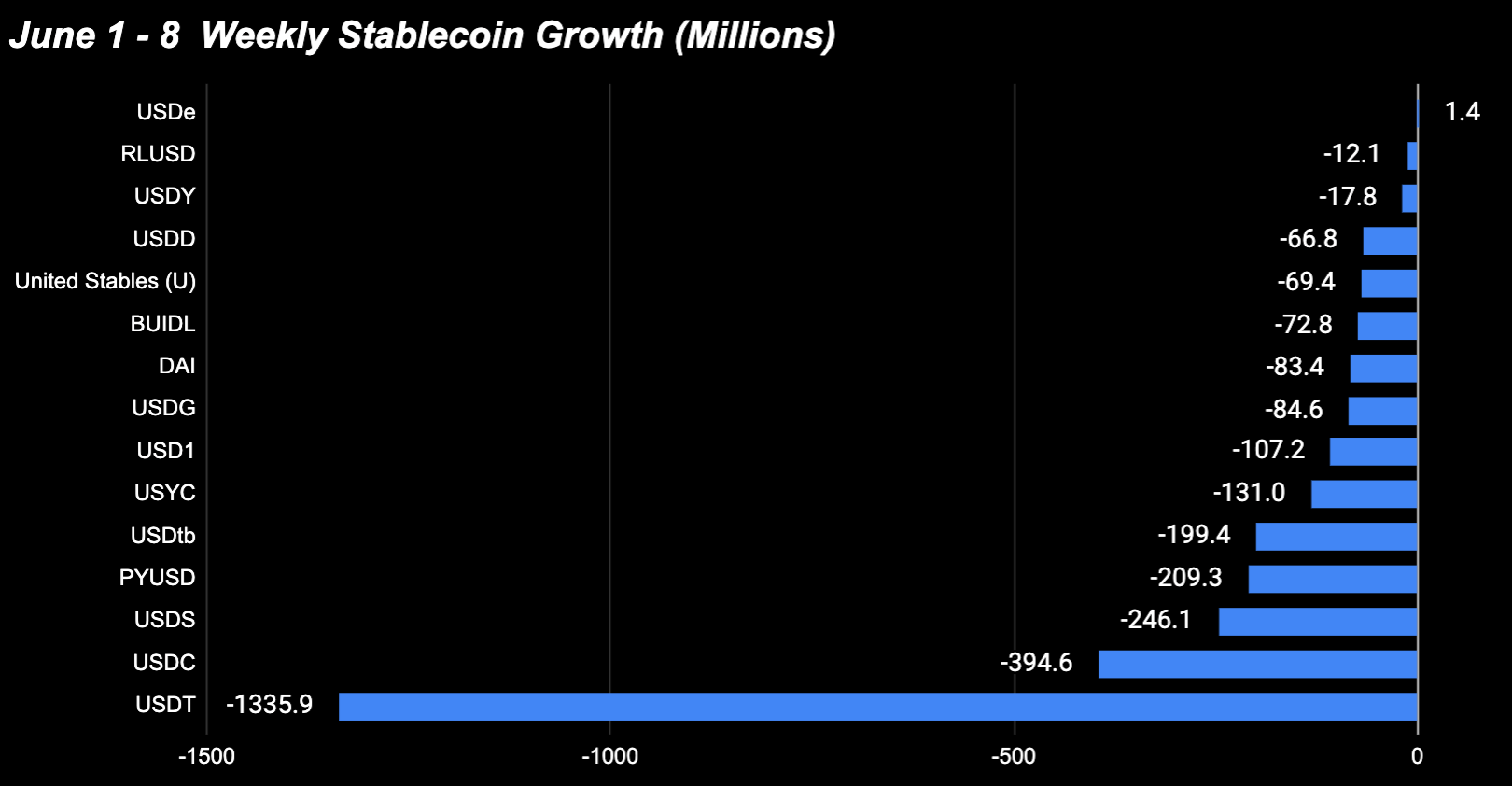

Total stablecoin supply - Accelerating Outflows

Down $3.654B (-1.14%), third consecutive week of outflows and the largest single-week drain in the YTD timeframe. The trend is accelerating, not stabilizing (-$0.53B → -$2.80B → -$3.65B over three weeks).

ETF flows

ETF flows: BTC -$1.722B, ETH -$174M. The institutional bid that carried Q2 remains in retreat. The BTC outflow worsened versus last week’s -$1.416B; ETH outflows (grey bar) eased slightly. Following May’s -$2.3B monthly BTC ETF outflow — the worst of 2026 — the distribution trend has carried into June.

1C. Week-Ahead Catalysts

Wed Jun 11 — US CPI & Core CPI (May).

The week’s pivot for rate expectations; markets watch tariff pass-through.

Thu Jun 12 — US PPI (May), Initial Jobless Claims

Next week: FOMC Jun 16–17 — this week’s CPI sets the tone heading in.

Crypto Specific:

CLARITY Act — still a live regulatory watch after clearing Senate Banking (15-9) with momentum stalled; verify latest before publishing.

Source : tradingeconomics.com

Section 2 — Onchain Risk Regime

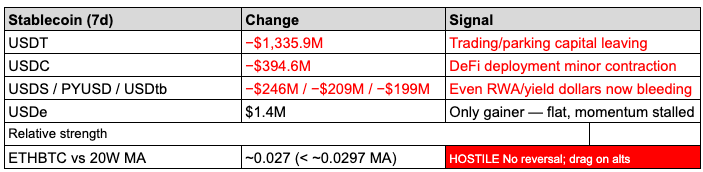

This week’s stablecoin data is a clean risk-off signal for the second week running: the two largest stablecoins contracted hard together, and this time the bleed reached the yield-bearing and RWA-backed names too.

USDe +$1.4M - the only stablecoin with positive growth, but still effectively flat.

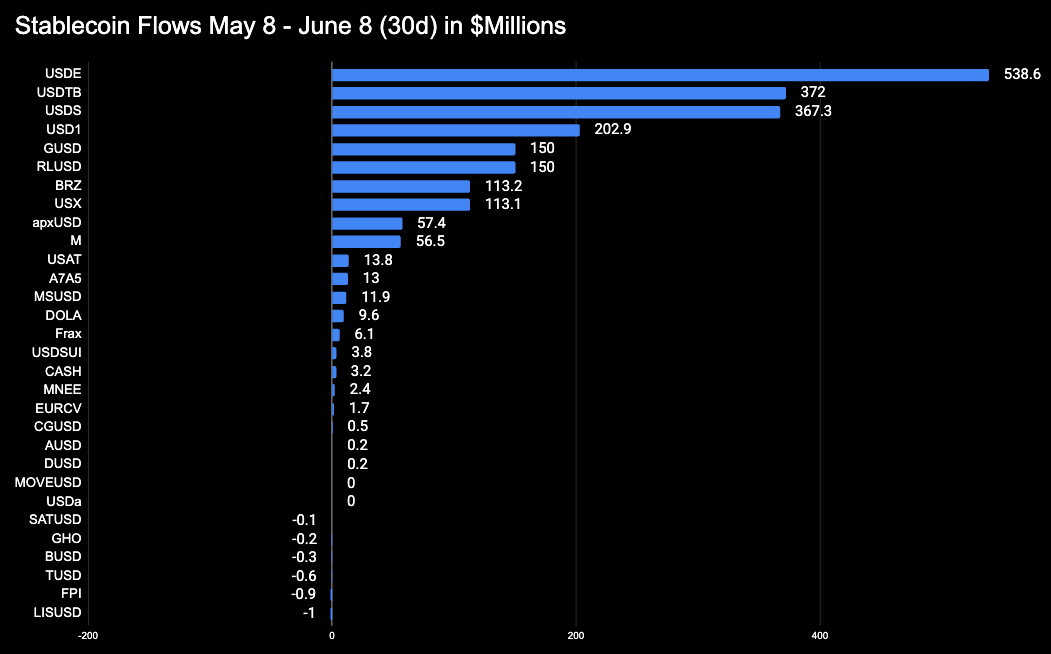

30d context: USDT and USDC structural bleed confirmed — not a this-week story. The growth over 30 days concentrated entirely in yield-bearing and RWA-backed dollars (USDe +$539M, USDtb +$372M, USDS +$367M). Transactional capital leaving, yield-seeking capital staying.

The signal: USDT (trading and parking capital) and USDC (DeFi deployment capital) leaving together is broad de-risking, not rotation. When capital rotates between venues, one of the two usually grows; both contracting means money is leaving crypto, not moving within it. The deeper tell this week is that the RWA and yield-bearing dollars that held up last week — USDtb, USYC, BUIDL — are now bleeding too, but the 30d trend suggests that this is only a cool down when looking at the 30d trend

USDe was the only gainer at +$1.4M, but that is essentially flat — Ethena’s basis trade has stopped attracting fresh capital this week rather than leading it.

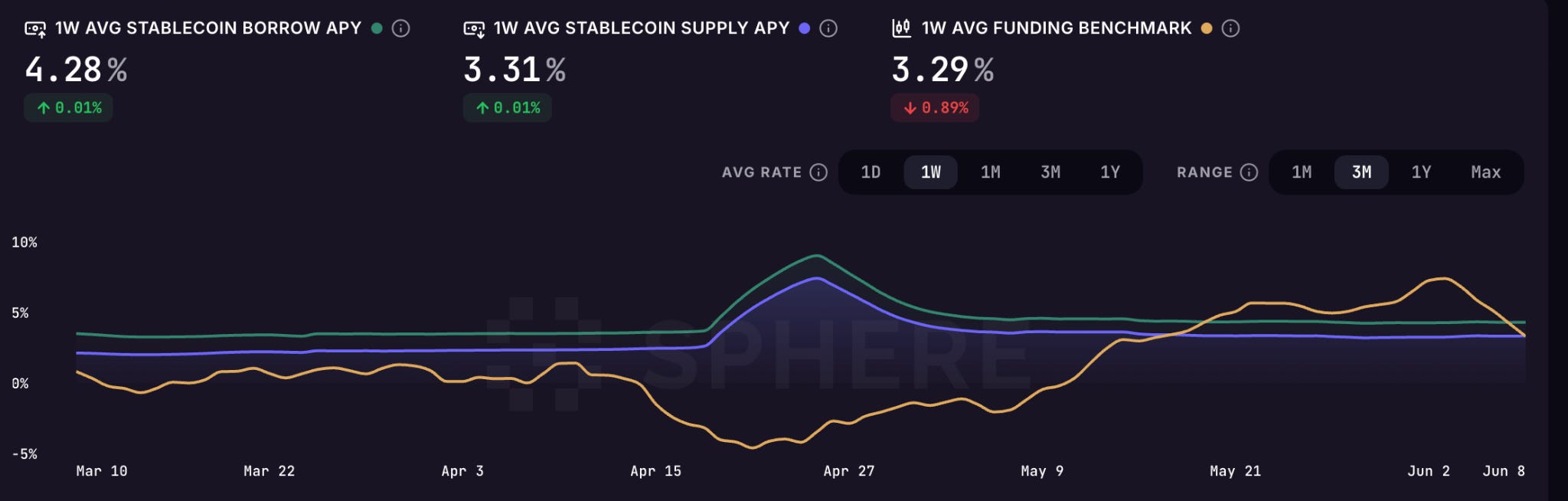

Aave / Sphere Rates — CALM, FUNDING Falling

Aave / Sphere Rates — funding flips from greed to fear

Borrow APY: 4.28% (+0.01%)

Supply APY: 3.31% (+0.01%)

Funding benchmark: 3.29% (-0.89%)

Lending rates are flat — no forced unwind pressure in spot markets. The move that matters is funding, which fell 0.89% to 3.29% and is now below the borrow rate for the first time in weeks. The spread has flipped from roughly +2.0% last week (funding 6.25% over borrow 4.25% = greed) to about -1.0% this week (funding below borrow = fear).

Per the framework: a large positive spread (Funding > Borrow) signals greed/caution; a negative spread (Funding < Borrow) signals fear/opportunity and often appears near local bottoms. Leveraged longs that were dominant last week have been flushed in a single week. This is now a contrarian fear/opportunity zone, not a greed warning — the one signal in this edition that leans constructive rather than defensive. Worth watching for confirmation.

ETH to BTC Ratio

ETHBTC at ~0.027 , below the 20W MA (~0.0297) and showing no signs of recovery. ETH continues to underperform BTC with no reversal in sight — no signal to overweight ETH within the crypto sleeve, and a drag on altcoins broadly.

Verdict: Onchain regime RISK-OFF. Both USDT and USDC contracted for a second week, the risk-off now reaching RWA/yield dollars, USDe flat, leverage flushed out, ETH still bleeding against BTC. Capital is defensive — but the funding flip below borrow is the one early contrarian tell to watch.

Section 3 — Chain Comparison

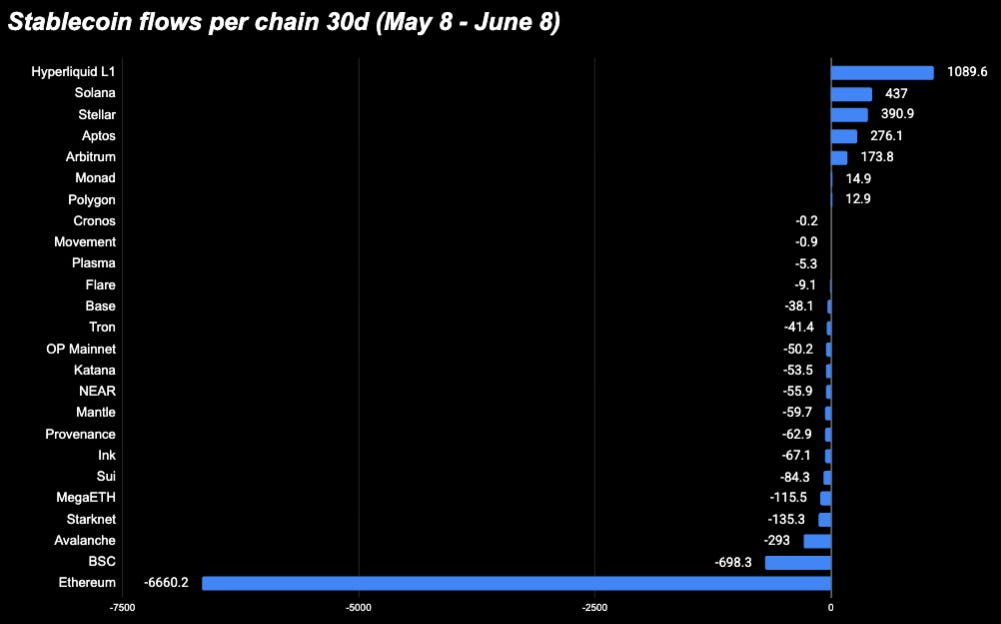

3A. Stablecoin flows by chain

Solana — The Mint-Driven Headline +$369.3M (+2.42%)

The largest absolute gain of any chain, but mostly mechanical: a 500M USDC Circle mint over June 2–3 drove it (USDC +$436.5M), partly offset by USDT (-$47.5M). Fresh mints inflate supply on issuance — the inflow only counts once that USDC deploys into Solana DeFi (Kamino, Jupiter) rather than sitting idle.

XRPL — The RLUSD Settlement Rail +$102.1M (+15.47%)

pure single-token settlement story: RLUSD is 99% of XRPL's stablecoin supply, and its gain mirrors RLUSD leaving Ethereum (-$153.7M) — Ripple deliberately splitting Ethereum as the DeFi hub from XRPL as the payments rail. Mastercard named RLUSD among its regulated settlement stablecoins on June 3, and Ripple is expanding RLUSD access across Turkey's ~$200B crypto market.

Ripple has simultaneously expanded RLUSD access in Türkiye via partnerships with BiLira (stablecoin issuer + exchange), Bitexen (multi-jurisdictional infrastructure across Turkey, MENA, South Africa, Europe), and Bitlo. Turkey facilitates approximately $200B in annual crypto transaction volume — the largest in MENA. The rollout targets corporate treasury operations, liquidity management, and cross-border payments under Turkey’s 2024 CMB licensing framework.

Stellar — USDC Surge + Three-Layer Institutional Buildout +$59.3M (+8.0%)

The week's strongest 30d trajectory (+95.7%), driven entirely by USDC (+$63.9M) while Ondo's USDY base stayed flat. The catalyst stack is institutional: MoneyGram launched MGUSD on June 2, Circle's CCTP went live in May (making Stellar USDC fully fungible), and RWA transfer volume is up 317% over 30 days.

Aptos — The Payments Story Matures +$72.3M (+3.99%)

Steady accumulation (30d +13.27%), not a spike. The driver is a new regulated MENA–Africa B2B payment corridor (Aptos Foundation + HashKey + Daya, June 4) — real settlement capital that stays onchain as long as corridors are active, not speculative DeFi flow.

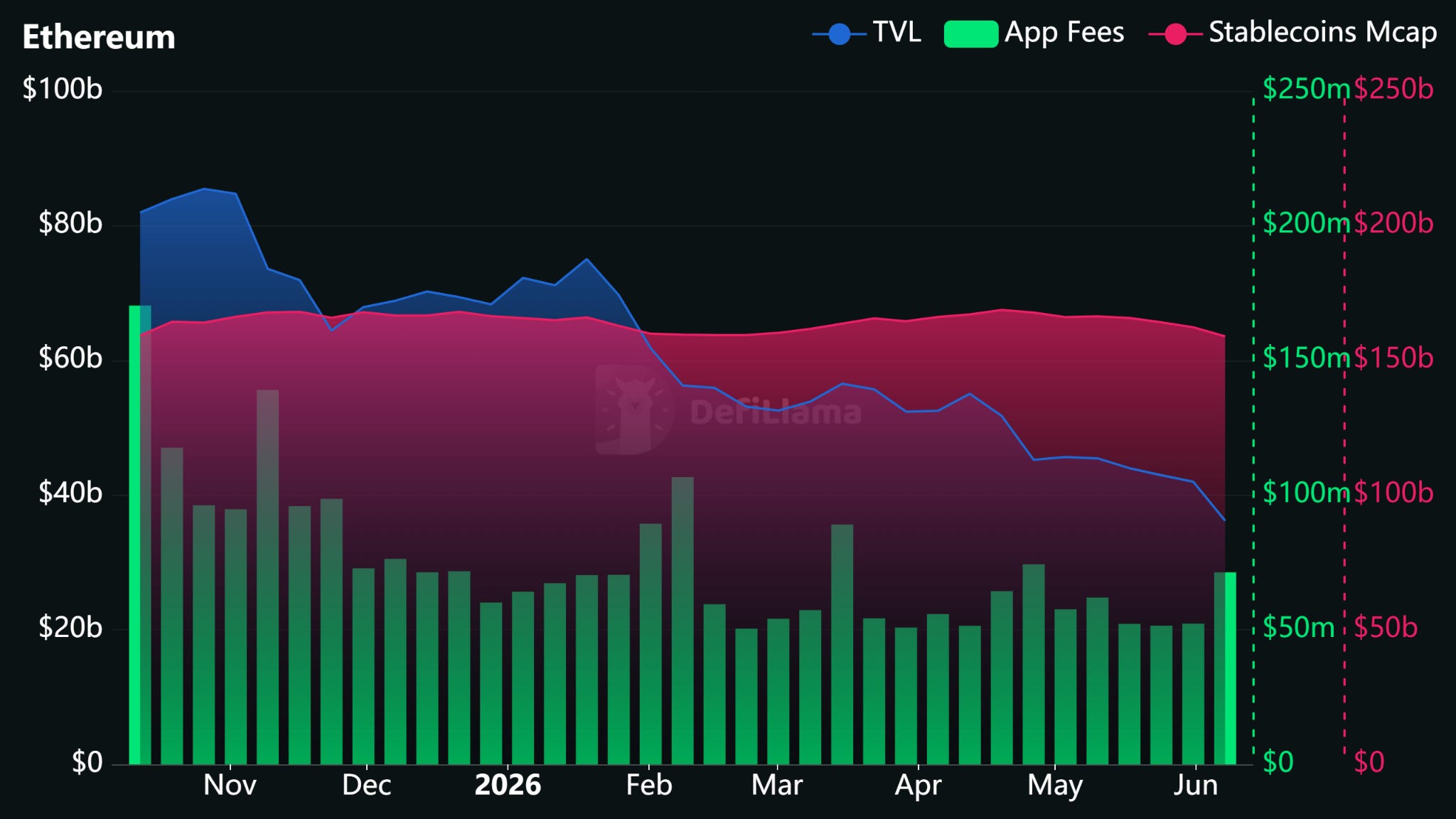

Ethereum — The Multi-Vector Donor −$3.43B (−2.11%)

Its worst stablecoin week of Q2 and 71.9% of all chain outflows

USDT: $80,042.9M (50.4% share), −$1,098.8M (−1.4%) — migrating to Tron and CEX custody

USDC: $48,450.0M (30.5% share), −$717.1M (−1.5%) — redistributing to Solana (Circle mints), Base, Hyperliquid

USDS: $8,083.9M (5.1% share), −$246.6M (−3.0%) — DeFi demand softening

PYUSD: $1,825.8M (1.1% share), −$190.6M (−9.4%) — broad PayPal contraction concurrent with Mastercard announcement

USDF: $1,183.3M (0.7% share), −$203.3M (−14.7%) — institutional stablecoin rebalancing

RLUSD: $931.1M (0.6% share), −$153.7M (−14.2%) — deliberate migration to XRPL settlement rail

apxUSD: $390.6M (0.2% share), −$133.9M (−25.5%) — largest proportional loss among synthetics

Ethereum’s DeFi protocol layer continues generating dominant app fee revenue — the highest of any chain. But the stablecoin float is a capital allocation decision, and capital is migrating to purpose-built chains: perpetuals margin (Hyperliquid), payment corridors (XRPL, Stellar, Aptos), and L2 execution venues (Base, Arbitrum). The 30d (−4.90%) and 7d (−2.11%) are directionally aligned across every major token category: this is structural, not episodic.

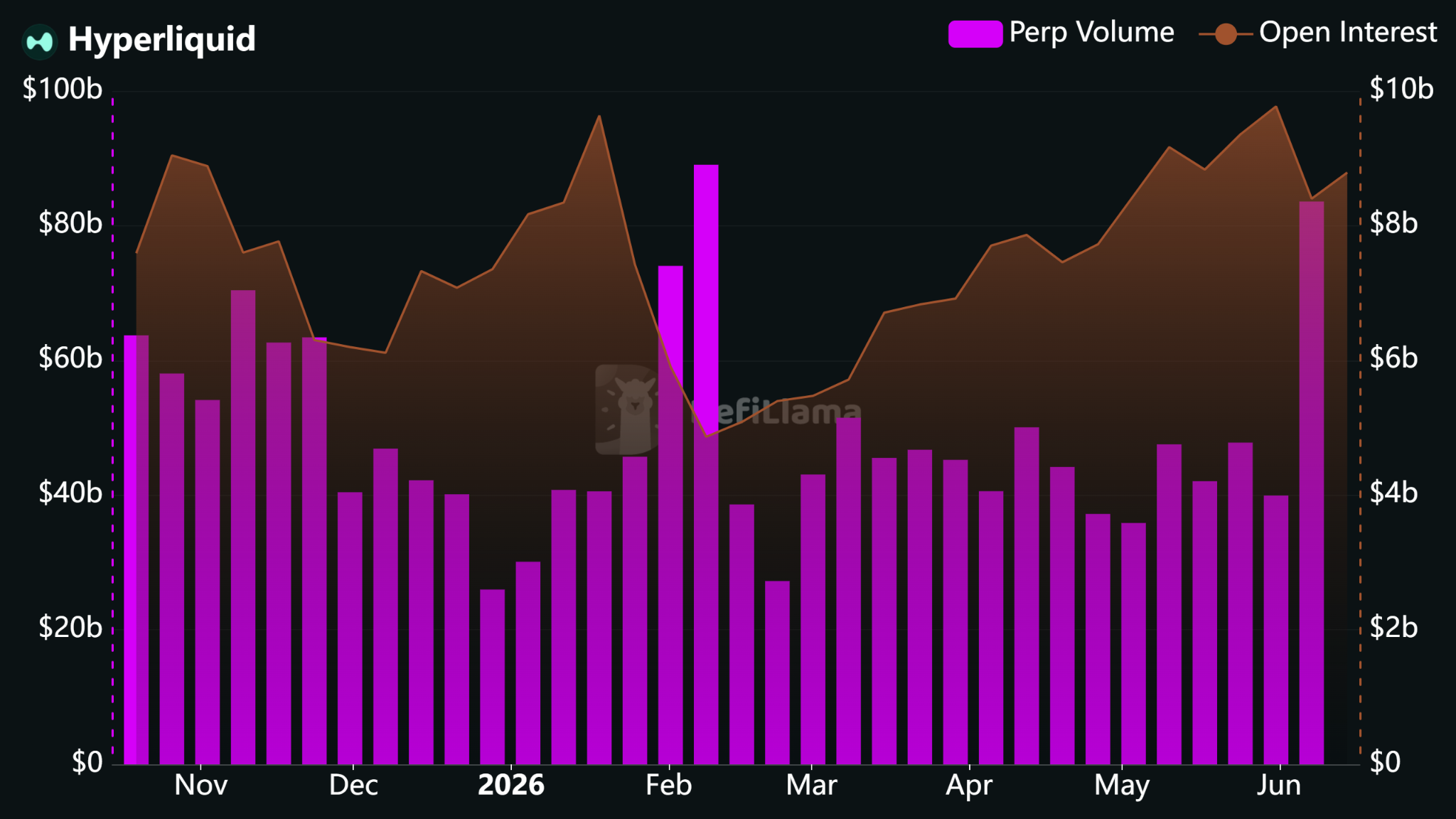

Hyperliquid — The Post-AQAv2 Plateau −$127.9M (−1.94%)

Hyperliquid’s 7d loss is a deceleration, not a reversal. The 30d (+20.22%) remains among the strongest structural trends in the tracked universe.

USDH’s decline is fully scheduled. Felix deprecates USDH vaults June 12, Native Markets terminated effective June 18, and Hyperion DeFi (NASDAQ: HYPD) is unwinding $28.7M in HYPE agreements.

The USDC outflow (−$129.5M) reflects risk-off deleveraging: with Fear & Greed at 23 and BTC-led product outflows at $1.67B , perpetuals traders reducing position sizes is the expected behavior. Less active margin deployed → USDC exits the vault. This is not a reversal of AQAv2 — it is a consequence of the macro environment.

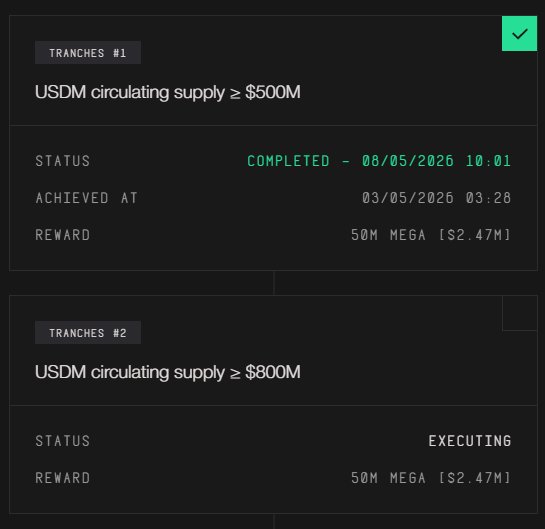

MegaETH — The USDM KPI Squeeze −$19.9M (−3.00%)

The headline −$19.9M is 100% USDM. USDe is expanding.

USDe (Ethena): $430.6M (67.1% share), +$15.7M (+3.77%) — growing

USDM (MegaETH native): $205.7M (32.1% share), −$34.1M (−14.21%) — the entire outflow

USDM is MegaETH’s native yield-bearing stablecoin, developed with Ethena and indirectly backed by BlackRock BUIDL via USDtb . It sits at the centre of MegaETH’s token unlock mechanics: one of three KPI conditions unlocking 53.3% of the remaining MEGA token supply requires a 30-day average USDM supply of $500M.

At −$34.1M this week, USDM is moving away from the KPI target, not toward it. MEGA has fallen approximately 73% from its April 30 ATH — and the USDM contraction reflects positions originally deployed to accumulate MEGA points/yield now unwinding as post-launch incentives decay.

3B. Structural Shifts

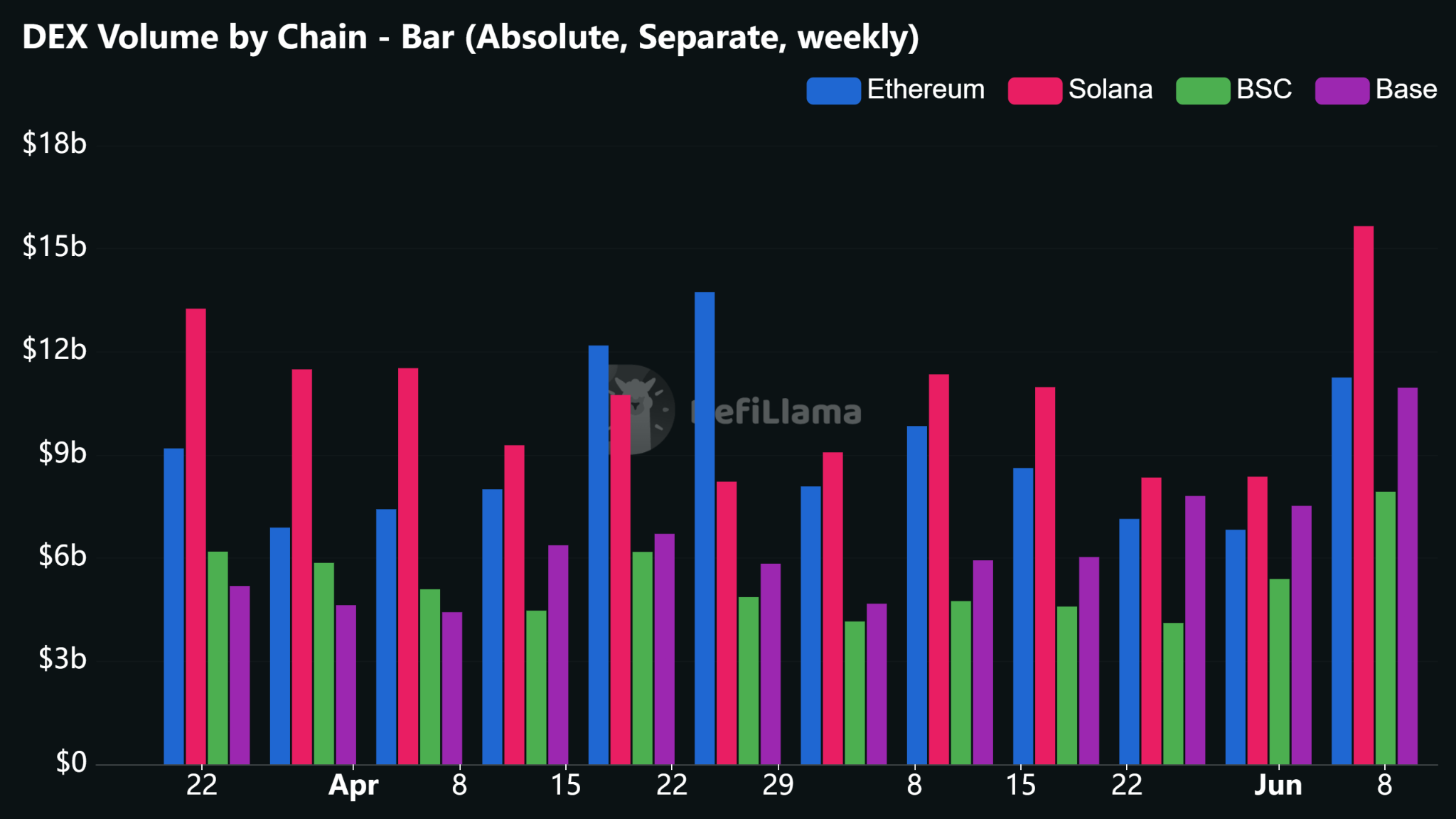

Solana — $16.3B (+83.3% 7d, +12.8% 30d). The week’s largest DEX venue, and the volume is now institutional rather than speculative. Jump Crypto’s BisonFi PropAMM did $3.0B (+177%) at spreads reportedly tighter than centralized exchanges, while Manifest’s zero-fee order book ($2.0B) is 87% stablecoin-to-stablecoin settlement. Memecoin activity is down ~62% from its peak — execution and cross-stablecoin flow have replaced it as the demand driver.

Base — $11.1B (+44.7% 7d, +32.7% 30d). Base is now within $719M of flipping Ethereum, at 93.9% of its weekly DEX volume. Aerodrome supplies the BTC/ETH liquidity backbone (51% of Base volume), while Uniswap V3 surged +180% on a wave of AI agent token launches — the sharpest protocol-level move on any chain.

Ethereum — $11.8B (+66.5% 7d, −20.2% 30d). The 7-day pop masks a negative 30-day trend. Volume rose while stablecoin supply fell -2.1%, meaning traders are recycling existing balances rather than bringing in new capital — recovery, not inflow.

BSC — $8.1B (+45.7% 7d, +5.2% 30d). The jump is campaign-driven (HOME fantasy-sports tournament, Binance Wallet DeFi Hub), not organic — the staircase volume pattern gives it away. The two genuine signals underneath: Lista DEX (+541% 30d on liquid-staking pairs) and Ondo’s tokenized-Treasury volume ($349M, +53.6% 30d).

4A. Token Price Movers - Observations, not trade ideas.

$DRV (Derive)

Derive, the leading onchain options protocol, posted a record fee week of ~$140K — its highest without incentives YTD, which the team frames as pure organic growth — on ~$707M of weekly volume (ETH taking a larger share than prior weeks) and $28.7B cumulative.

Options are highly traded in a high-volatility market, demand for hedging and optionality rises rather than falls.

The supporting stack is dense: DRV listed on Coinbase this quarter, scored 37/40 on Blockworks’ Token Transparency Framework, has V3 targeted for September and four new listings slated for June, and just integrated NautilusTrader, an open-source engine that lets systematic traders research, backtest, and run live execution against Derive’s spot, perps, and options from one model.

$BABY (Babylon)

A BTCfi catalyst that ties directly into our recurring Aave thread. Babylon brought native Bitcoin-backed borrowing live on public testnet with Aave v4, powered by its Trustless Bitcoin Vaults.

The mechanic is the point: users post BTC as collateral and borrow without giving up custody, wrapping, or bridging — a step toward native Bitcoin credit markets rather than synthetic BTC exposure. This is testnet, not mainnet, so it is a forward catalyst, not live revenue. Source: Babylon X.

$JTO (Jito)

A structural Solana story more than a single-event catalyst. Jito’s BAM infrastructure and its plugins are pushing Solana execution to the point where recent research argues SOL-USDC now executes materially better than centralized exchanges, with price improvement beginning to spread to BTC and other pairs. The protocol is also leaning into JTX - Jito’s new unified on-chain trading app for Solana

$LAB

Context, not a catalyst. Included to explain the week’s most violent move, not as anything to chase. LAB, the token of a multi-chain AI trading terminal, ran up sharply on a protocol-level buyback program, then collapsed 77% within two hours on June 2, from a peak of $27.96 to approximately $6.

On-chain investigator ZachXBT and others allege that insiders control over 95% of LAB’s supply, with vesting reportedly altered to extend the rally and major unlocks scheduled for July and August 2026.

A buyback flywheel on a thin, concentrated float is reflexive in both directions — it is exactly the profile we skip when there’s no durable catalyst.

Sources: ZachXBT, CoinMarketCap.

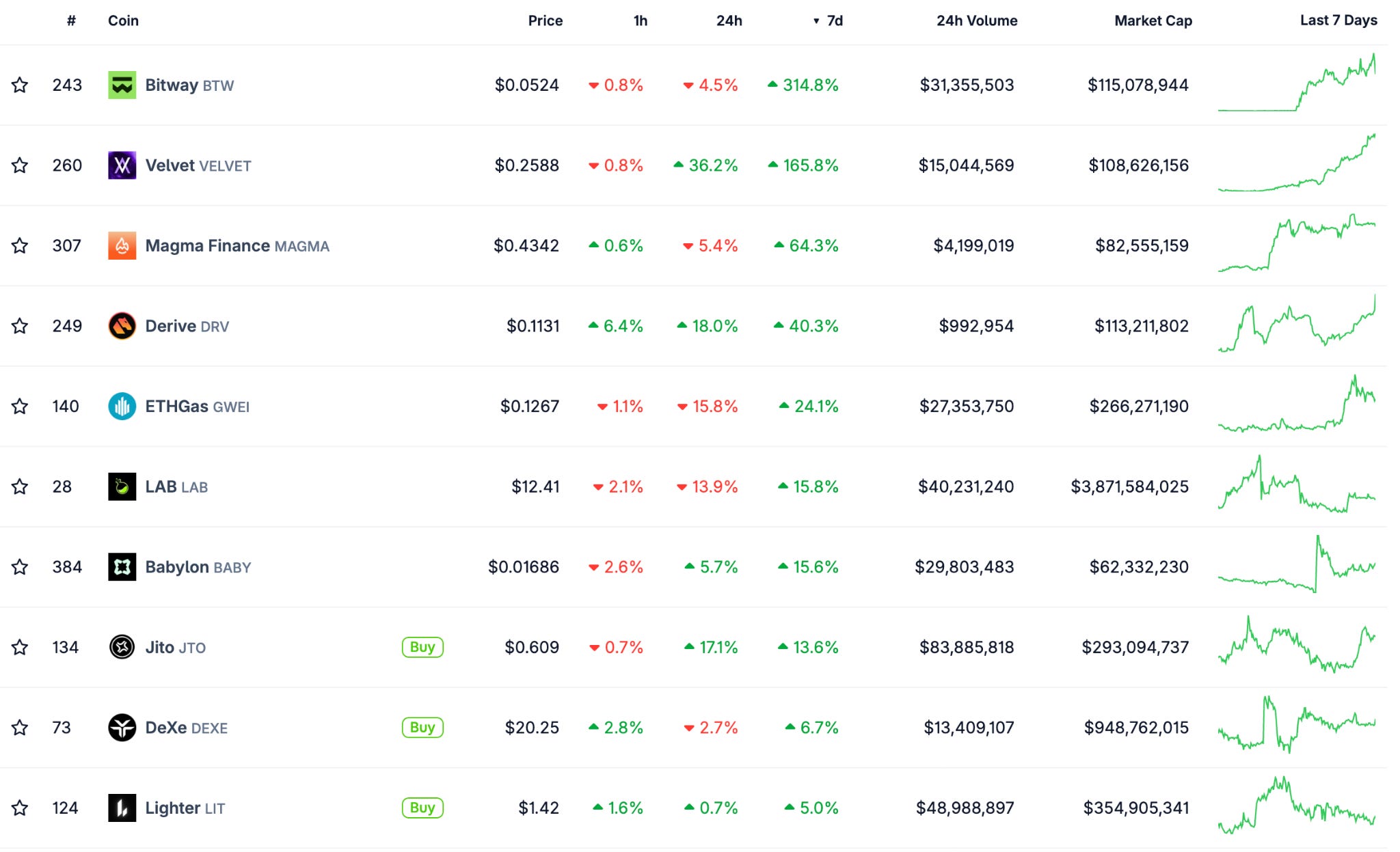

4B. TVL Gainers ($50M+ filter) — Ranked by absolute $ inflow.

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.