On-chain Outlook: Hyperliquid Shows No Sign of Slowing, Base Flips Ethereum DEX Volume, and many more...

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Headlines:

- Babylon proposes native BTC collateral for Aave

- Tangent launches USG borrowing and points program

- New Market Trading exploited through Squid integration

- Hyperliquid removes external oracles from prediction markets

- Bitmor exploited after executor wallet compromise

- Pendle lists Strata srNUSD and jrNUSD markets

- Native Markets begins USDH platform sunset

- Royco Dawn drops fees across all markets

- Solstice opens live Season 1 SLX claims

- Ondo founder Nathan Allman passes away

- Binance renews USD1 yield campaign incentives

- Neutrl adds reserve allocation transparency tools

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

Key Takeaways

Regime: Mixed to Neutral with a hostile edge.

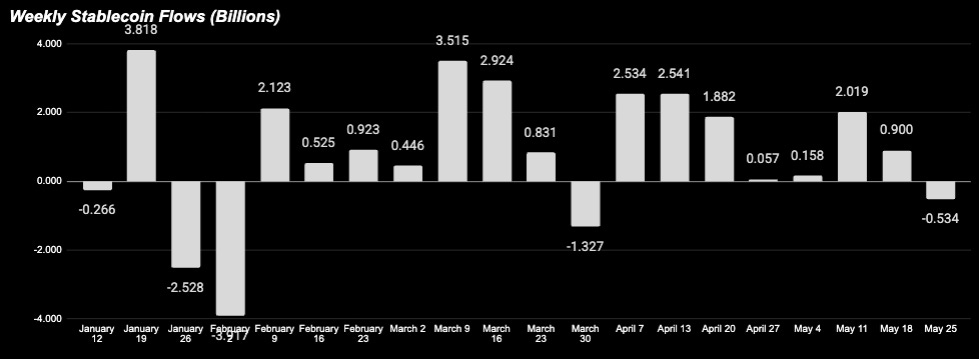

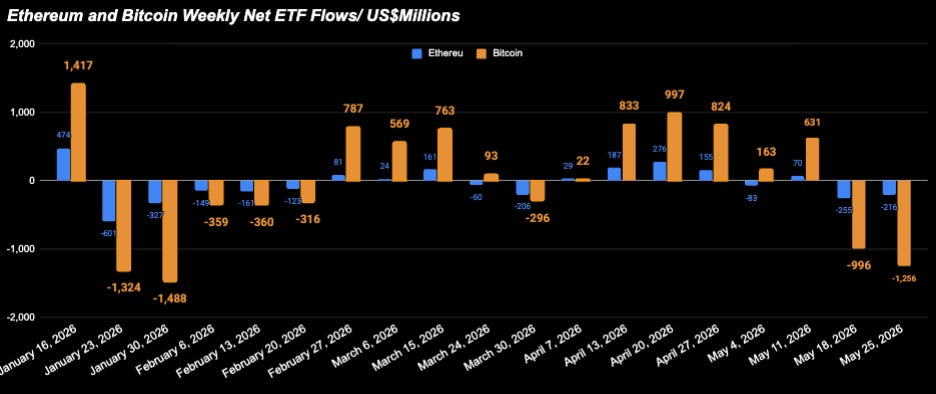

Net liquidity remains supportive but contracted for the first time in months, while rates continue pushing higher with the 2Y at 4.12% (1% weekly change). On-chain stablecoin supply turned negative this week -$534M (-0.17%), the first weekly outflow in two months. Moreover, capital is reacting to the same inflation fears driving the second consecutive week of major ETF outflows (BTC -$1.26B, ETH -$216M).Hyperliquid shows no sign of slowing down.

HYPE rallied +34% this week as Hyperliquid’s AQAv2 rollout shifted USDC into the core quote asset role, driving +$1.26B stablecoin inflows (95% USDC). The larger ~$5B USDC base materially expands the yield-sharing pool funding HYPE buybacks, with estimates pointing to a ~$170M annualized uplift.Base flipped Ethereum on weekly DEX volume for the first time.

Base traded $7.893B over the past seven days versus Ethereum’s $7.433B, with Aerodrome alone accounting for over half ($4B) of Base’s volume. The driver is the combination of Coinbase routing retail flow into Aerodrome’s pools and the AI agent ecosystem (OVPP, Venice AI’s VVV, GAI) building on Base.

Section 1 — Macro + Capital Backdrop

1A. Traditional Macro

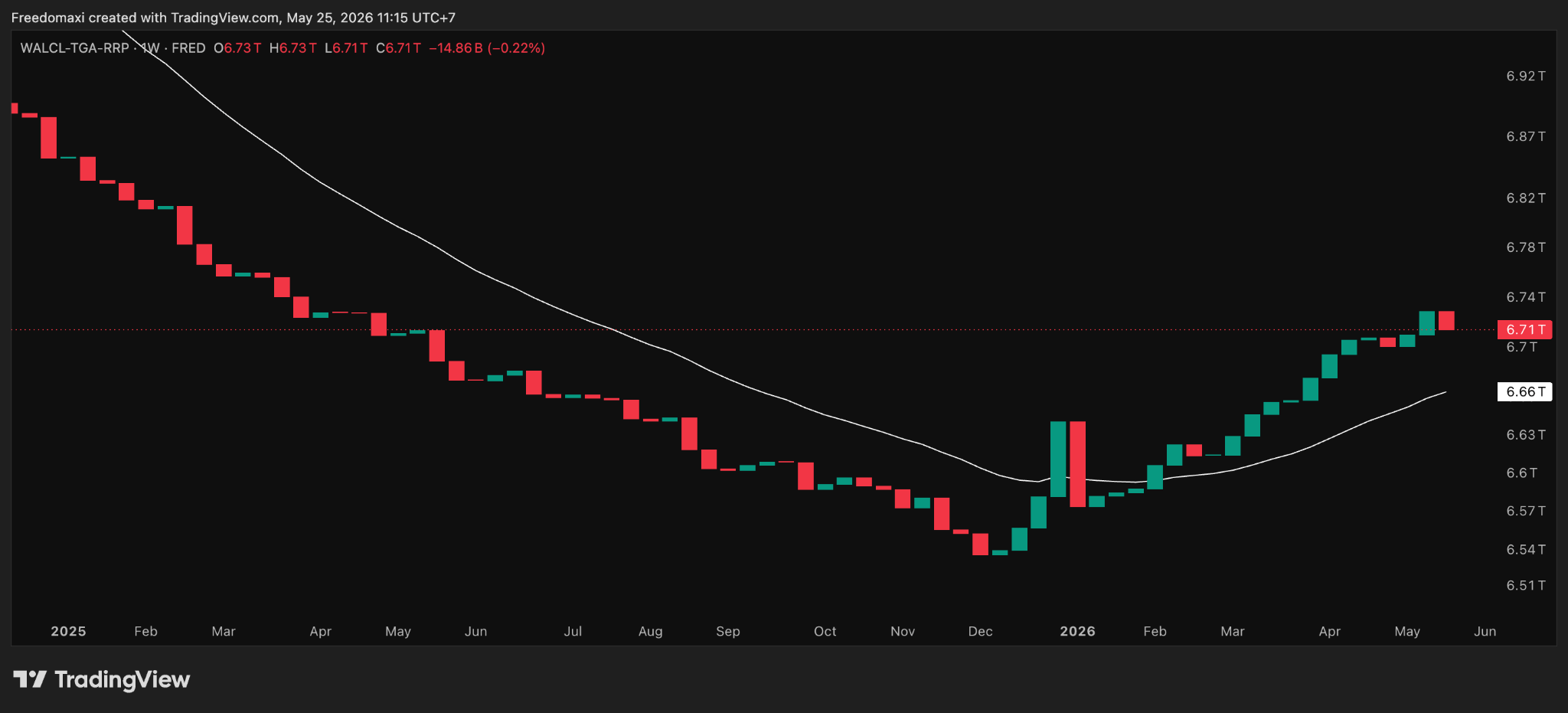

Net liquidity (WALCL-TGA-RRP) vs 20W MA

Still above 20W MA ($6.66T) — MILD HEADWIND. First weekly contraction in months. The structural uptrend remains intact and price is above the moving average, but the momentum that drove the early-May reflation has stalled. Onchain transmission: stablecoin supply turned negative this week.

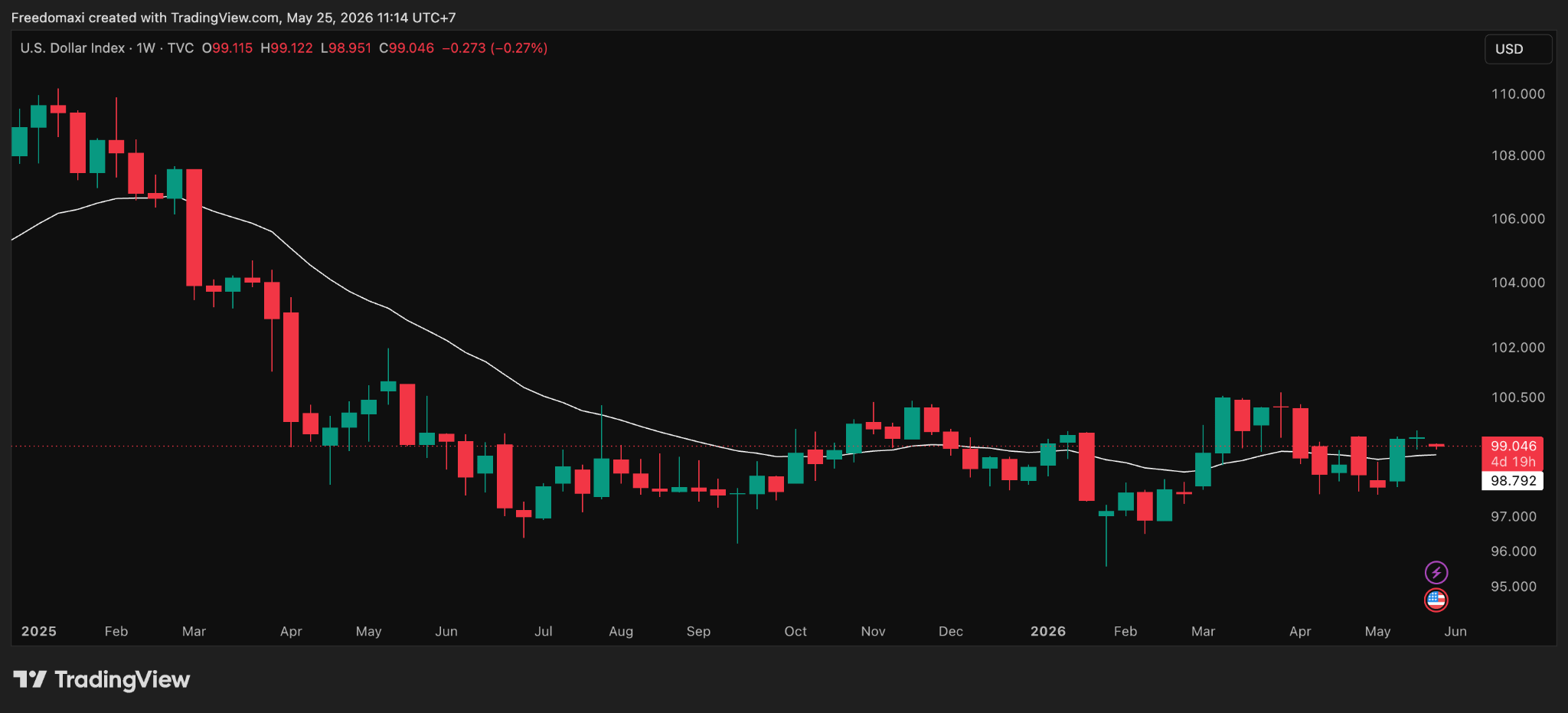

DXY vs 20W MA

DXY: 99.05, -0.27% WoW. Just above 20W MA (98.79) — NEUTRAL. Dollar weakened slightly but is hovering at the moving average. Not a directional signal either way. The DXY ranged 97-100 for most of the past nine months and remains there.

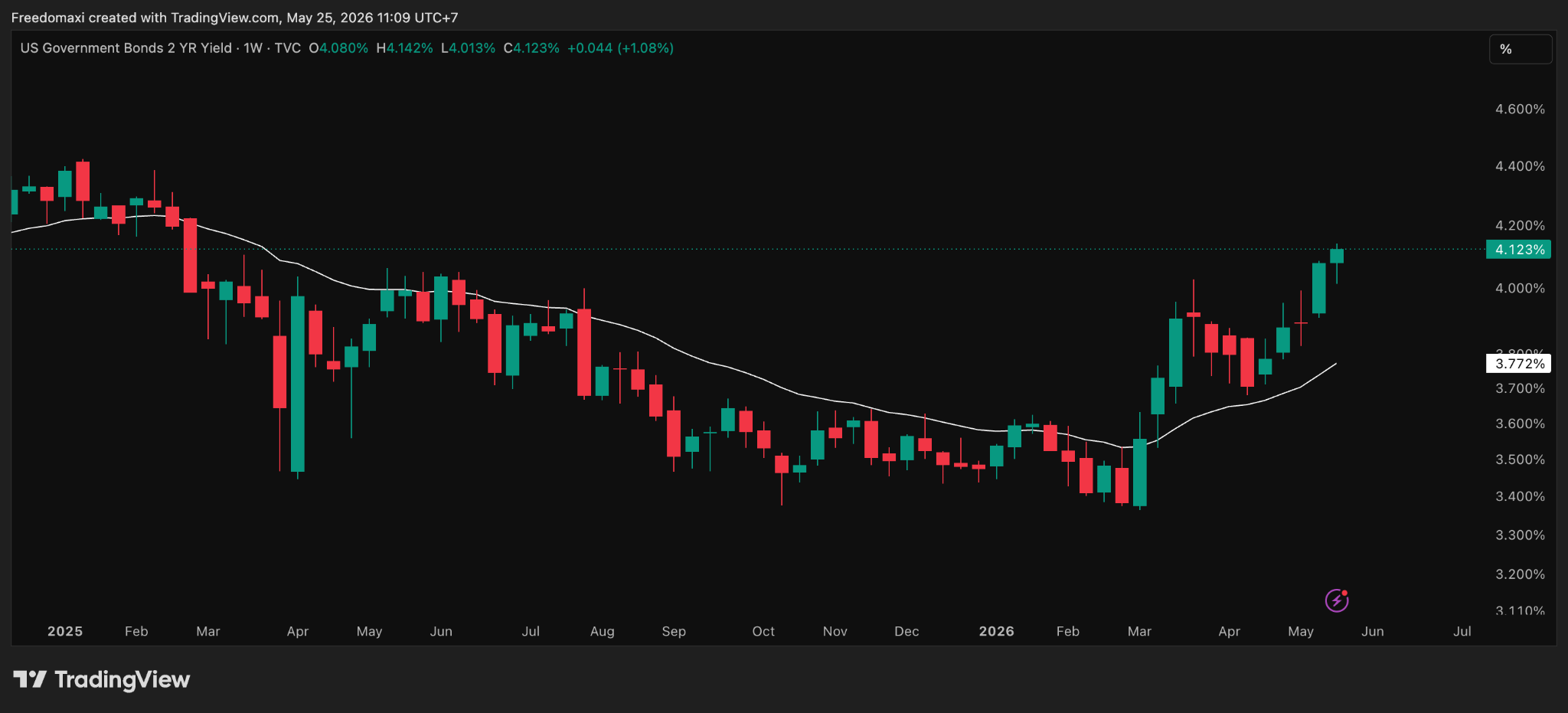

US 2Y yield vs 20W MA

US 2Y yield: 4.123%, +1.08% WoW. Above 20W MA (3.772%) — HOSTILE. The 2Y is now ~35bps above its 20W MA and continues to climb after April CPI at 3.8%. T-bills at ~4.1% risk-free are compressing the spread against curated vault yields. The bond market is repricing for a longer pause.

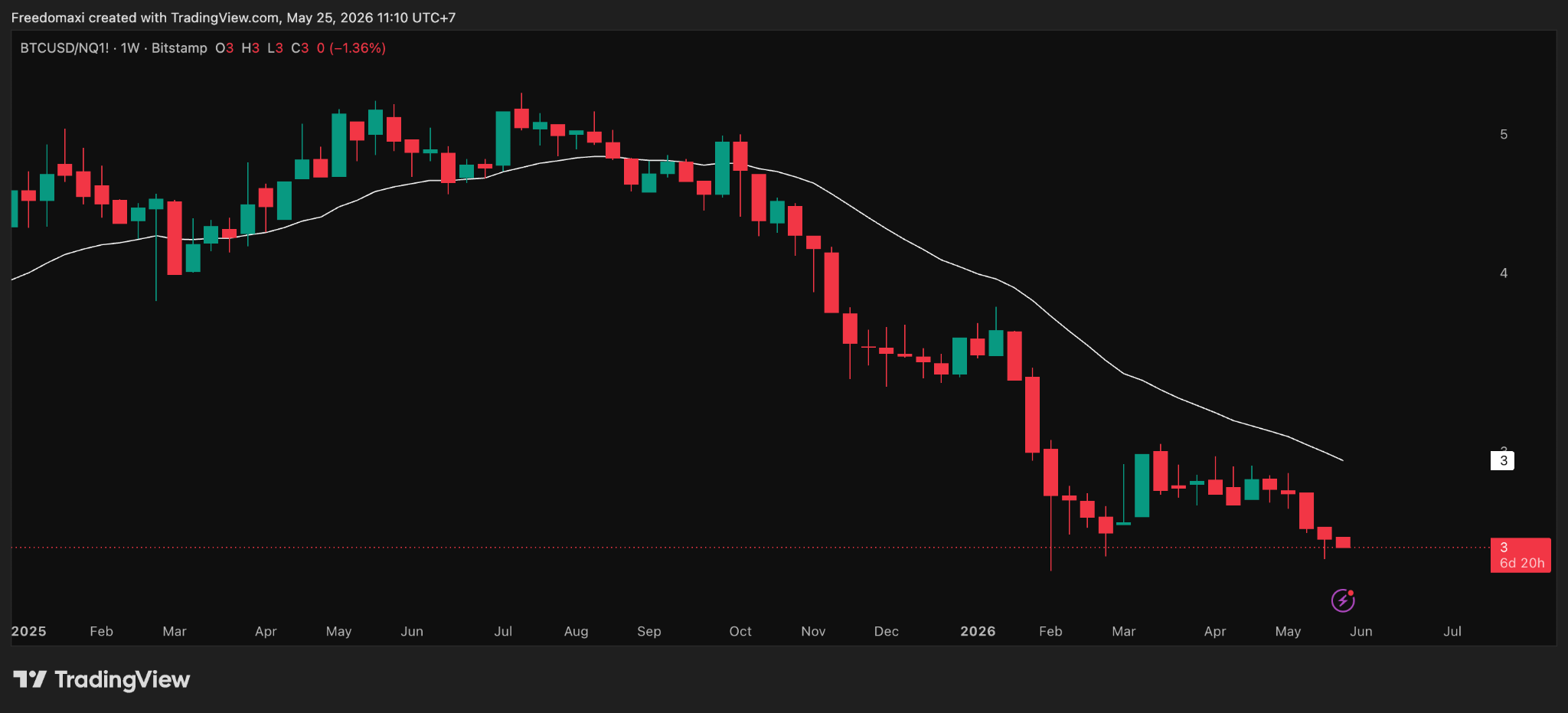

BTC/NQ ratio vs 20W MA.

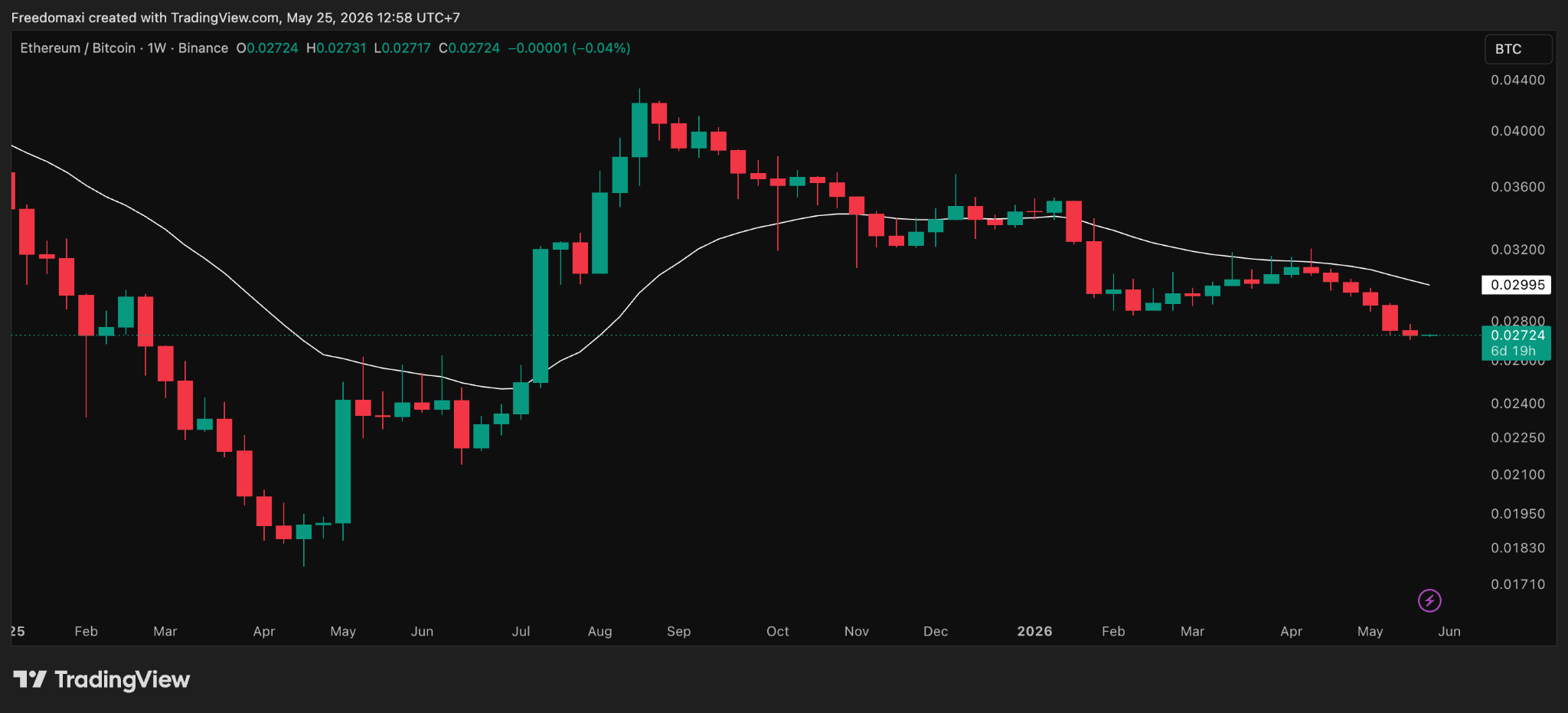

BTC/NQ ratio: ~2.65, still falling. Below 20W MA — HOSTILE. BTC underperformance regime confirmed since the October liquidation event. ETH/BTC ratio at 0.02724, also below its 20W MA (0.02995) — ETH heavily underperforming, no signs of recovery. Capital within crypto continues to favor BTC over alt-L1s and ETH.

Composite: 0 supportive, 1 neutral, 3 hostile. Liquidity finally stopped doing the heavy lifting this week. The supportive signal weakened while every other indicator continued pressing against risk.

1B. Crypto Capital On-Ramp

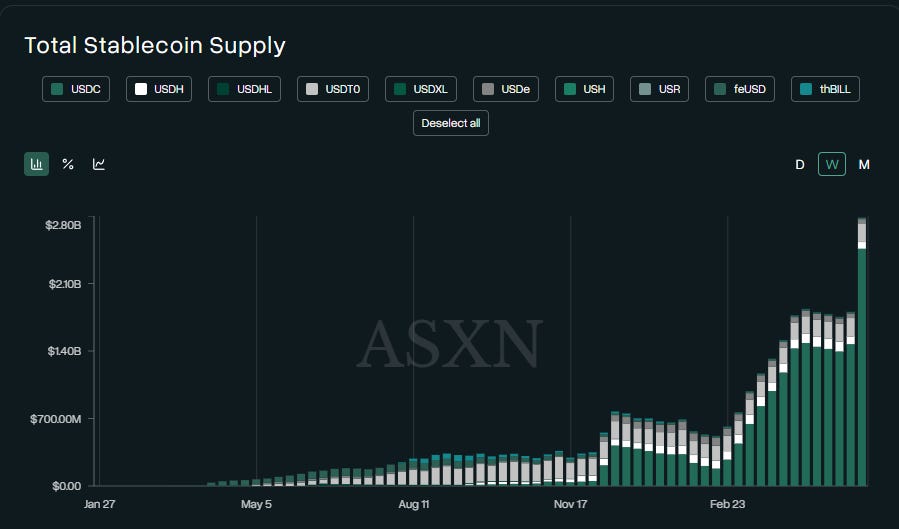

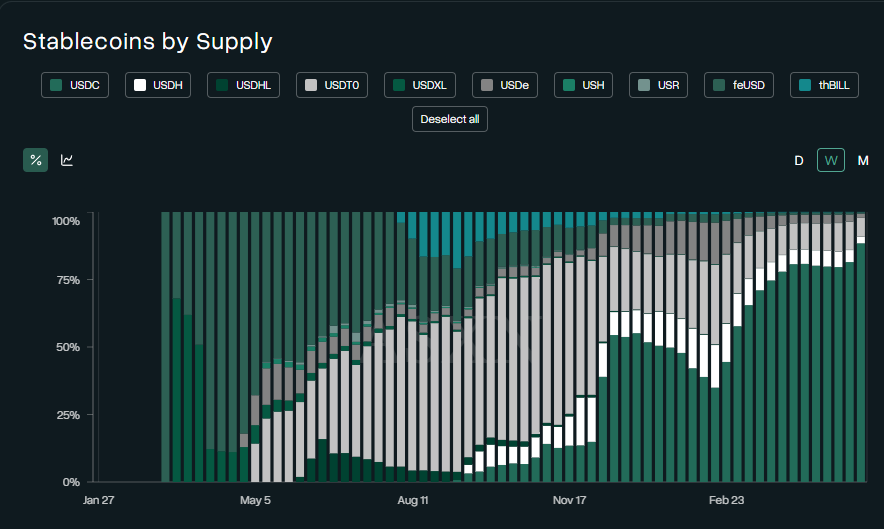

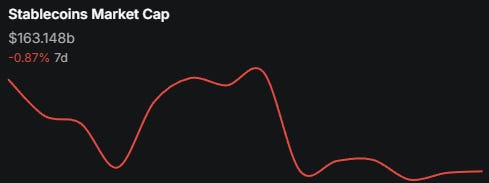

Total stablecoin supply (level + WoW)

Total stablecoin supply: -$534M (-0.17%). First weekly outflow in two months. After +$2.019B (May 11), +$900M (May 18), and now -$534M, the deceleration has fully tipped into a contraction. Not extreme — context: a -0.17% weekly move is normal market noise — but the direction matches the macro signal.

USDC vs USDT (deployment vs parking signal)

USDC: -$508M (-0.66%). Minor in % terms, but the second consecutive week of contraction. USDT: -$304M (-0.16%) — equally minor. Both are notable rather than meaningful.

ETF flows

ETF flows: BTC -$1,256M, ETH -$216M. Second consecutive week of major institutional outflows after the May 18 PPI shock. Combined -$1.47B vs last week’s -$1.25B. The 5-week BTC ETF inflow streak that ran through April is now a 2-week outflow trend.

1C. Week-Ahead Catalysts —

Wednesday May 27 — FOMC minutes from the April 29 meeting (Powell’s final FOMC, 8-4 split vote, most dissents since 1992). Markets will read how hawkish the committee inherited by Warsh actually is. NVDA earnings the same day — direct test of whether institutional capital keeps rotating tech > crypto.

Thursday May 28 — Q1 GDP (2nd estimate) after the first estimate showed slight contraction. Initial Jobless Claims, Pending Home Sales.

Friday May 30 — April Core PCE (Fed’s preferred inflation gauge). The pivot point for the week — a hot print extends the rate-hike pricing and the ETF outflow trend; a cooler print could reset expectations.

Crypto-specific:

CLARITY Act cleared the Senate Banking Committee on May 14 (15-9 vote) and now needs 60 votes on the Senate floor. Polymarket prices the 2026 floor vote at 64% probability, 61% signing odds. Source: Polymarket.

SEC tokenized equity pilot — innovation exemption sandbox expected “in the coming weeks” per Atkins.

Token unlocks — quiet week ahead. Sui has a $50M+ unlock June 1, Aptos next on June 12. The major May L2 cluster (APT/STRK/ARB) already cleared earlier this month.

Verdict: NEUTRAL with hostile edge. The structural story isn’t broken, but every non-liquidity signal is now pressing against risk. Friday’s PCE is the pivot.

Section 2 — Onchain Risk Regime

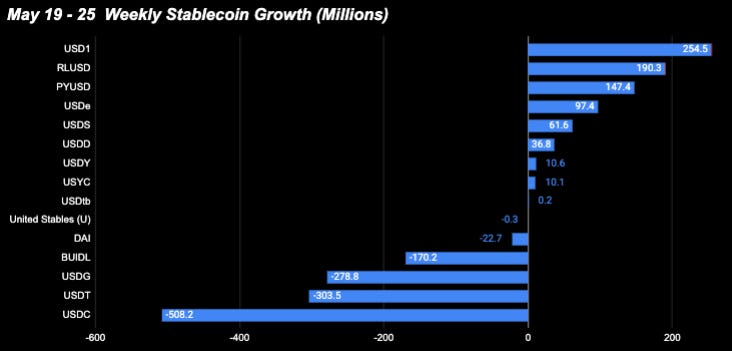

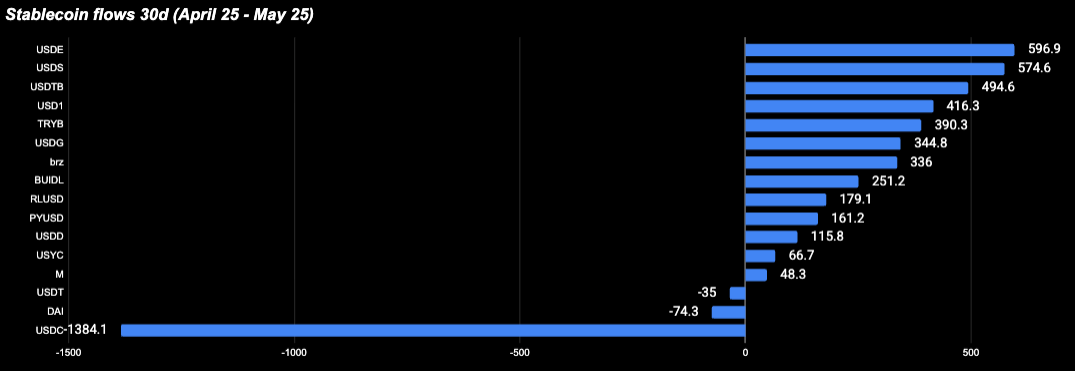

USDe is the largest 30d gainer at +$597M. Even though this week’s +$97M was a sharp slowdown from prior weeks, the basis trade has been the dominant capital absorber over the past month. The deceleration is real but the structural story is intact.

USD1, RLUSD, and PYUSD lead this week’s growth — and the 30d data shows these are sustained trends, not single-week prints. USD1 +$416M over 30d, RLUSD +$179M, PYUSD +$161M. RLUSD’s growth specifically tracks XRPL activity rather than Morpho/Sentora curated vaults. Payment-utility stablecoins have been quietly building all month.

USDG -$278M and BUIDL -$170M look severe this week, but 30d is still positive (+$345M and +$251M respectively). These are sharp single-week reversals on top of an otherwise growing base — the leverage loop cooling rather than a structural exit. Worth monitoring whether the reversal extends or stabilizes next week.

USDC -$508M extends the structural bleed: -$1.38B over 30d. This is the cleanest sustained outflow trend in the data. USDC has been contracting all month, the deployment capital signal hasn’t recovered.

USDT -$304M this week but only -$35M over 30d — essentially flat at the monthly level. Not a meaningful contraction, more like a single-week pause.

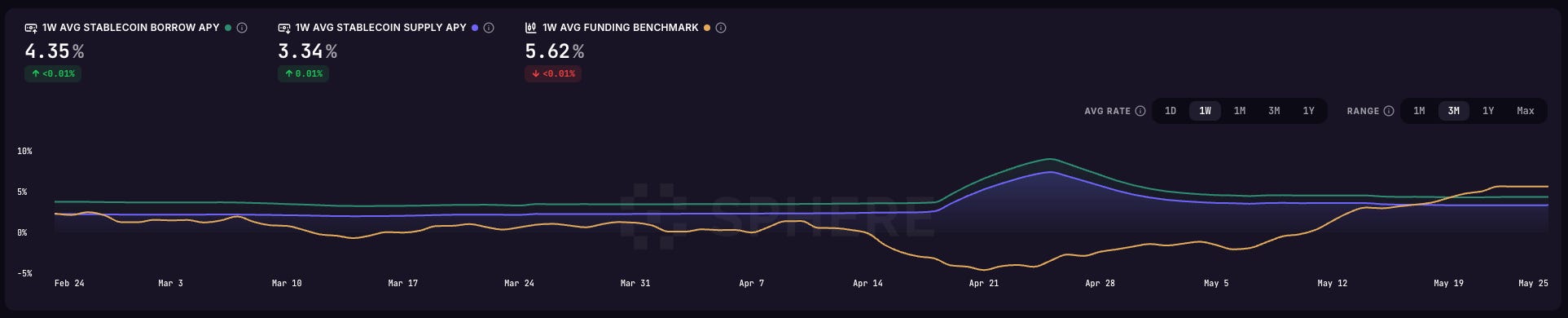

Aave / Sphere Rates — CALM, FUNDING RISING

Borrow APY 4.21% (-0.03% WoW), supply APY 3.21% (-0.01% WoW), funding benchmark 5.73% (+1.67% WoW).

Borrow and supply rates are essentially flat — no forced unwind pressure, lending markets are calm. The notable change is funding rising +1.67%, meaning more longs dominant in the market. Speculative leverage is rebuilding selectively while spot lending stays quiet. Source: Sphere.

Supply APY at 3.21% is now ~91bps below the 2Y at 4.12% — spread compression continuing. Base Aave yields are not competitive with T-bills, the structural engine behind capital migrating to curated vaults.

ETHBTC vs 20W MA

ETHBTC at 0.02724, 20W MA at 0.02995 — ~9% below the moving average. The multi-year downtrend that started in 2024 remains in force. No signal to overweight ETH within the crypto sleeve.

Section 3 — Chain Comparison

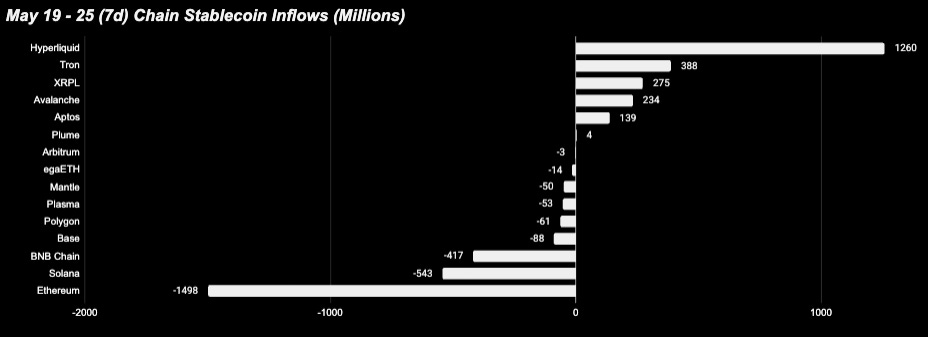

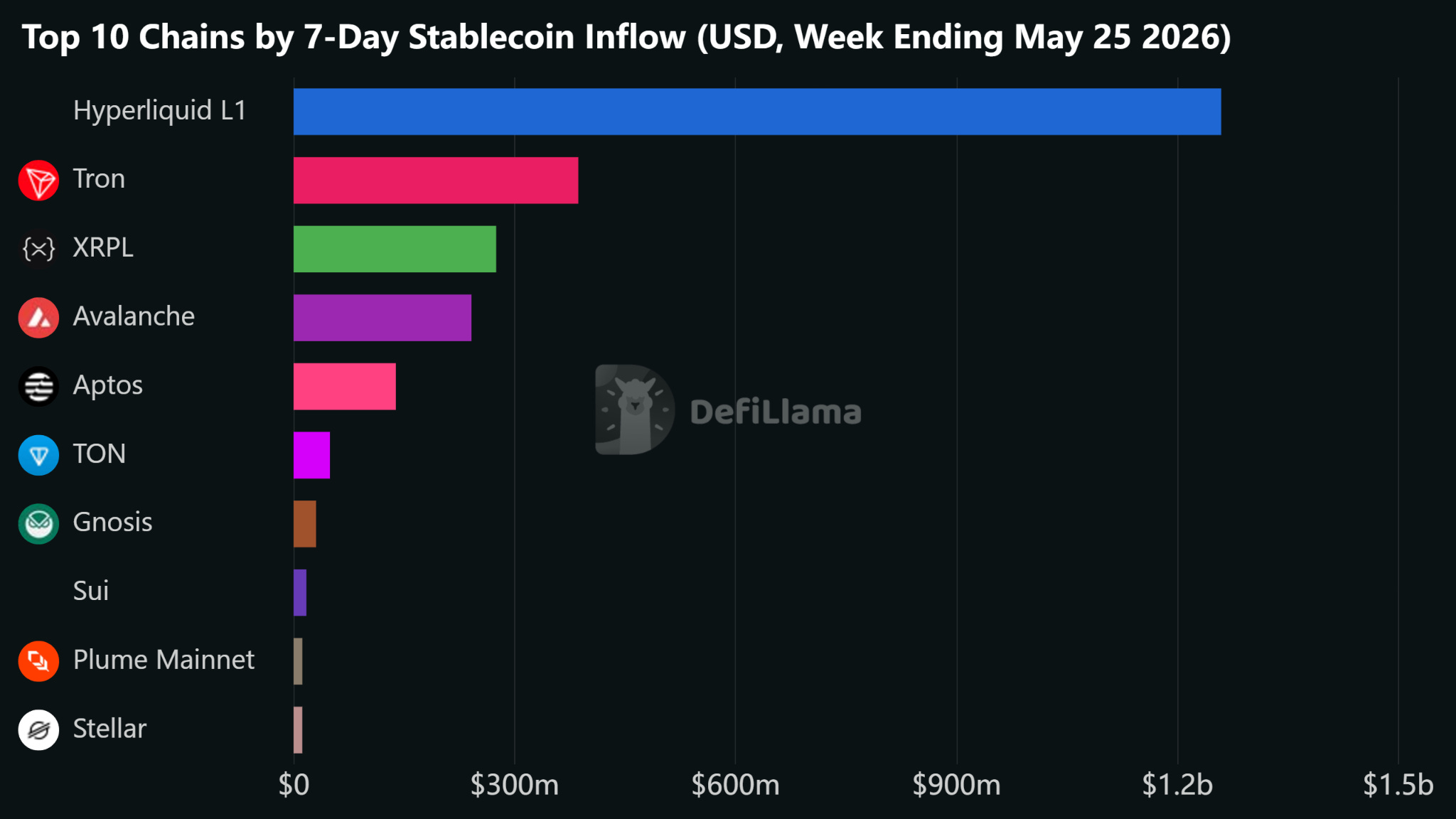

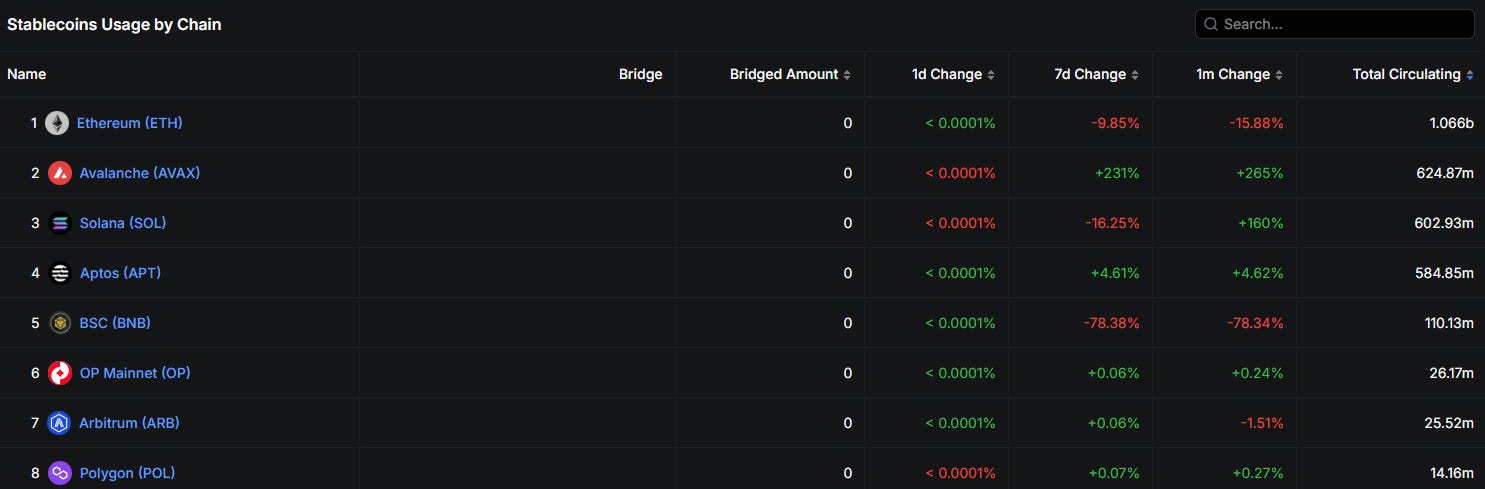

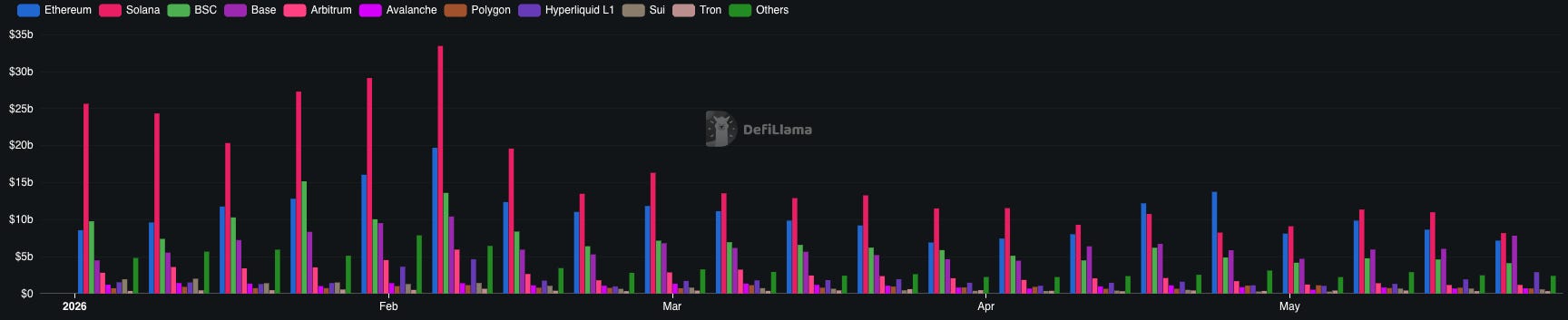

3A. Stablecoin flows by chain

1. Hyperliquid L1 — The AQAv2 Structural Re-Rating

Hyperliquid absorbed +$1.26B in stablecoins this week (+2.27% 7d), and the 30d context confirms this is acceleration. The 7d run-rate is actually faster than the 30d monthly average — this is a building trend, not a reversal.

The composition is almost entirely USDC: 95.3% of Hyperliquid’s stablecoin pool is USDC, with $1.27B net USDC inflow this week alone (+24.41% 7d, +38.61% 30d). This is a mechanically driven inflow, not organic market speculation. The trigger was AQAv2, announced May 14 — Coinbase (treasury deployer) and Circle (technical deployer/CCTP) both committed to USDC as the Aligned Quote Asset across HIP-1 through HIP-3, with HIP-4 (outcome markets) pending a future network upgrade.

The structural implication is stark: USDH (the prior native stablecoin) is being wound down with feeless conversions. It’s down -15.0% this week. USDe is also contracting, -8.48% 7d — traders are consolidating to USDC-only margin. The ~$5B USDC base now generates a structurally larger yield-sharing pool; people estimate this could represent a ~$170M incremental annualized buyback uplift for HYPE vs. the prior ~$100M USDH base.

2. XRPL — RLUSD as the New Settlement Rail

XRPL pulled in +$275M this week (+61.77% 7d, +68.12% 30d). The supply composition confirms this is 100% a single-token story: RLUSD at $679M + TBILL at $40M represent virtually the entire $725M on-chain supply — USDC and USDT are absent.

On May 20, Ripple executed its largest-ever single RLUSD mint: $200M on XRPL simultaneously with a $100M burn on Ethereum (largest single ETH burn on record), leaving a net $90.8M outflow from Ethereum’s RLUSD supply. This isn’t an isolated event — XRPL’s RLUSD supply has doubled in 60 days (from ~$300M in late March to ~$690M per web data, confirmed directionally by our $679M on-chain figure). Ethereum RLUSD is now being treated as the DeFi/liquidity hub while XRPL is the settlement/payments hub — a deliberate strategic bifurcation.

Ripple Prime’s institutional partnership with EDX Markets positions RLUSD as a potential settlement and collateral asset in regulated institutional trading infrastructure. A cross-chain bridge launched in April 2026 connecting XRPL, Ethereum, and Cardano enables the scale of these flows. The 30d trend (+68.12%) is consistent and building — this is structural repositioning by Ripple, not one-time rebalancing.

3. Avalanche — Institutional Camouflage

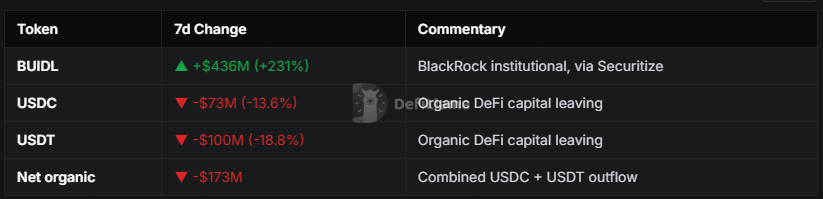

Avalanche’s headline +$253M 7d (+13.20% 7d, +8.62% 30d) is a technically accurate number that tells a completely misleading story.

The +$253M headline is entirely attributable to BUIDL (+$436M) more than offsetting -$173M of organic stablecoin departure. BUIDL on Avalanche is now a $625M position, driven by Securitize’s new mining actions.

The directional signal: Avalanche is gaining institutional RWA flows while losing organic DeFi capital. The 30d data supports this interpretation — the +8.62% 30d gain is smaller than the +13.20% 7d spike, meaning the BUIDL surge accelerated sharply this week. BlackRock filed two additional tokenized fund structures (BRSRV and BSTBL, targeting $10B+ combined) on May 8 — Avalanche is likely positioned as a deployment chain when those clear SEC approval (earliest ~late July 2026).

4. Ethereum — The System Donor

Ethereum is the origin of the week’s flows.

Token-level decomposition (7d):

USDC: -$1.22B (-2.40%) — migrating to Hyperliquid (AQAv2) and Base (Centrifuge deRWA USDC demand)

USDT: -$519M (-0.63%) — migrating to CEX rails and purpose-built chains

Combined outflow: -$1.74B in just USDC + USDT this week

This is not a liquidity crisis — Ethereum’s DeFi protocols still generate the highest app fees of any chain ($43.2M 7d). It is a structural migration: stablecoins are moving to chains with native yield infrastructure (Hyperliquid AQAv2), institutional rails (XRPL/Avalanche BUIDL), and lower-fee execution venues (Base).

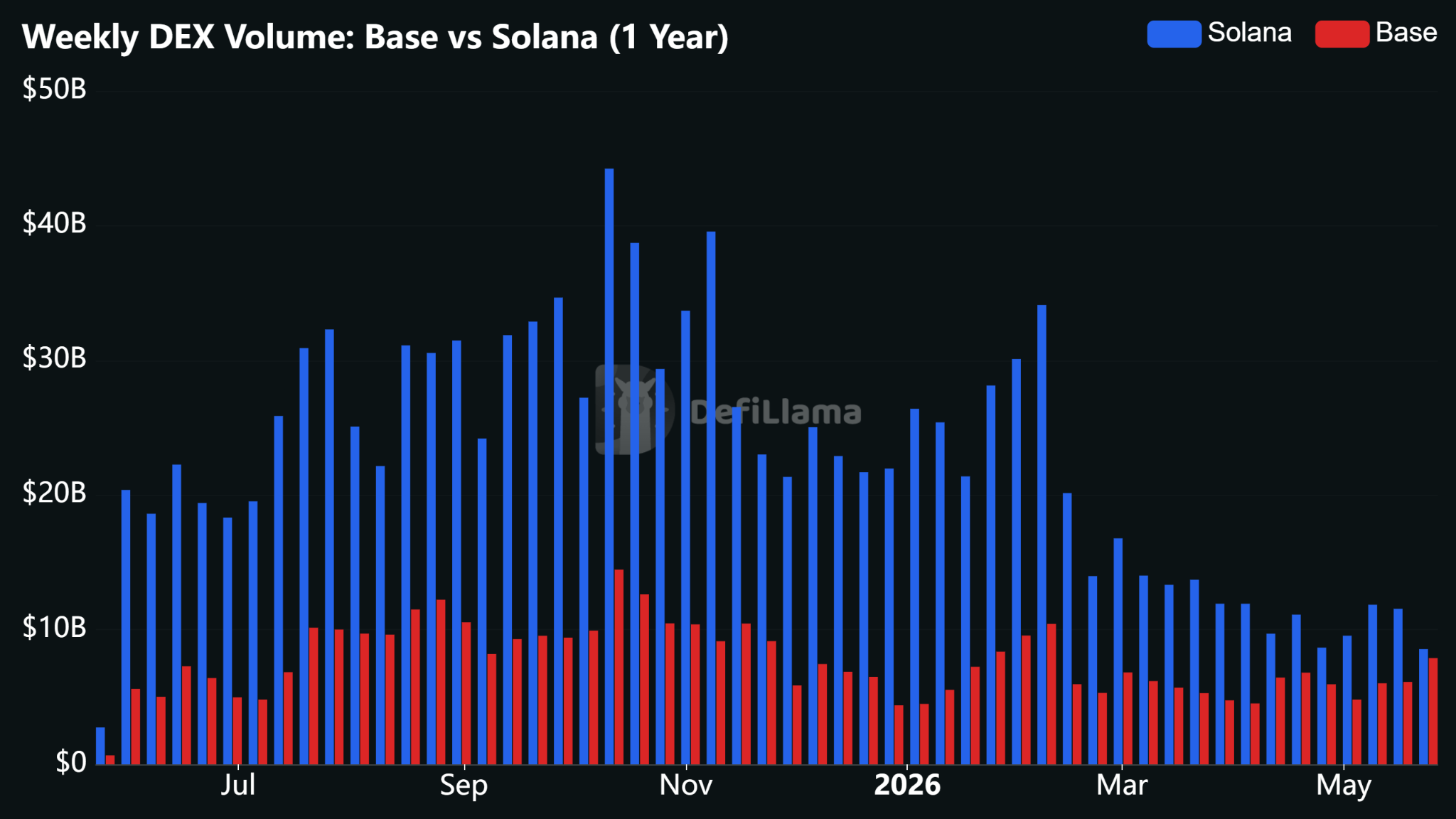

3B. Structural Shifts — Base DEX Volumes Flip Ethereum

Base flipped Ethereum on weekly DEX volume for the first time — $7.893B vs $7.433B. Last week we framed this as a possibility; this week it landed. The 30d still shows Ethereum ahead ($37B vs $25.8B), so this is a recent acceleration rather than an established pattern. Base is on track to outpace Solana next.

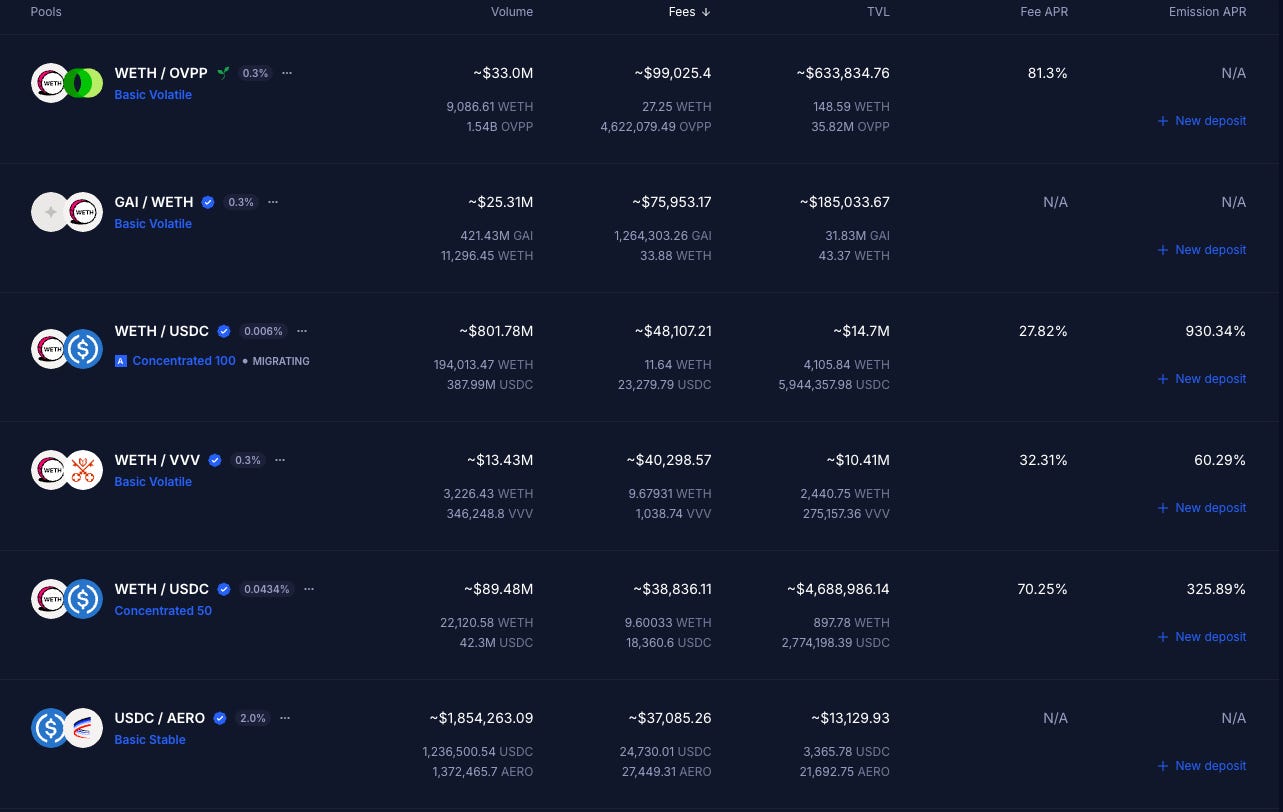

Aerodrome doing $4B of Base’s $7.893B (50%+ of total Base DEX volume). The top pools that generated the most volume on Aerodrome tell the structural story:

WETH/OVPP — $32.92M volume, 81.23% Fee APR

USDC/AERO — $1.85B volume (massive)

WETH/VVV (Venice AI) — $13.35M volume, 32.98% Fee APR

WETH/USDC concentrated pools — strong volumes

Base’s DEX volume is now powered by Coinbase retail flow into Aerodrome + AI agent ecosystem (OVPP, VVV/Venice AI, GAI) + AERO positioning ahead of the Aerodrome-Velodrome merger in July. That’s structurally different from BSC’s PancakeSwap meme-token speculation.

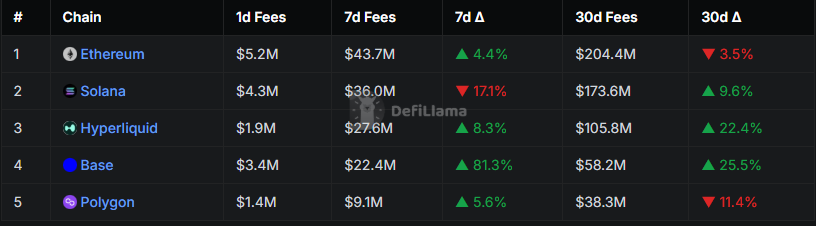

Ethereum DEX volume has been decelerating three weeks running while Base steadily climbed. Ethereum’s story is structurally different. Chain fees crashed -46.99% 7d to $2.48M — the lowest of the major DEX chains by raw fee level. But app fees are $43.2M 7d, the highest of any chain.

The split is meaningful: Ethereum’s L1 gas market is compressing as users move execution to L2s and specialized chains (the Dencun upgrade effect persisting), but the DeFi protocol layer sitting on Ethereum’s settlement layer — Aave, Uniswap, Curve, etc. — continues generating dominant revenue.

Ethereum is transitioning from a “chain where you pay gas” to a “chain where DeFi protocols generate revenue.” The 30d DEX volume trend (-16.7%) confirms the execution migration is ongoing.

Section 4 — Project & Protocol Discovery

4A. Token Price Movers — Top 5-7 from CoinGecko DeFi, brief catalyst attribution each. “Observations, not trade ideas.”

4A. Token Price Movers - Observations, not trade ideas.

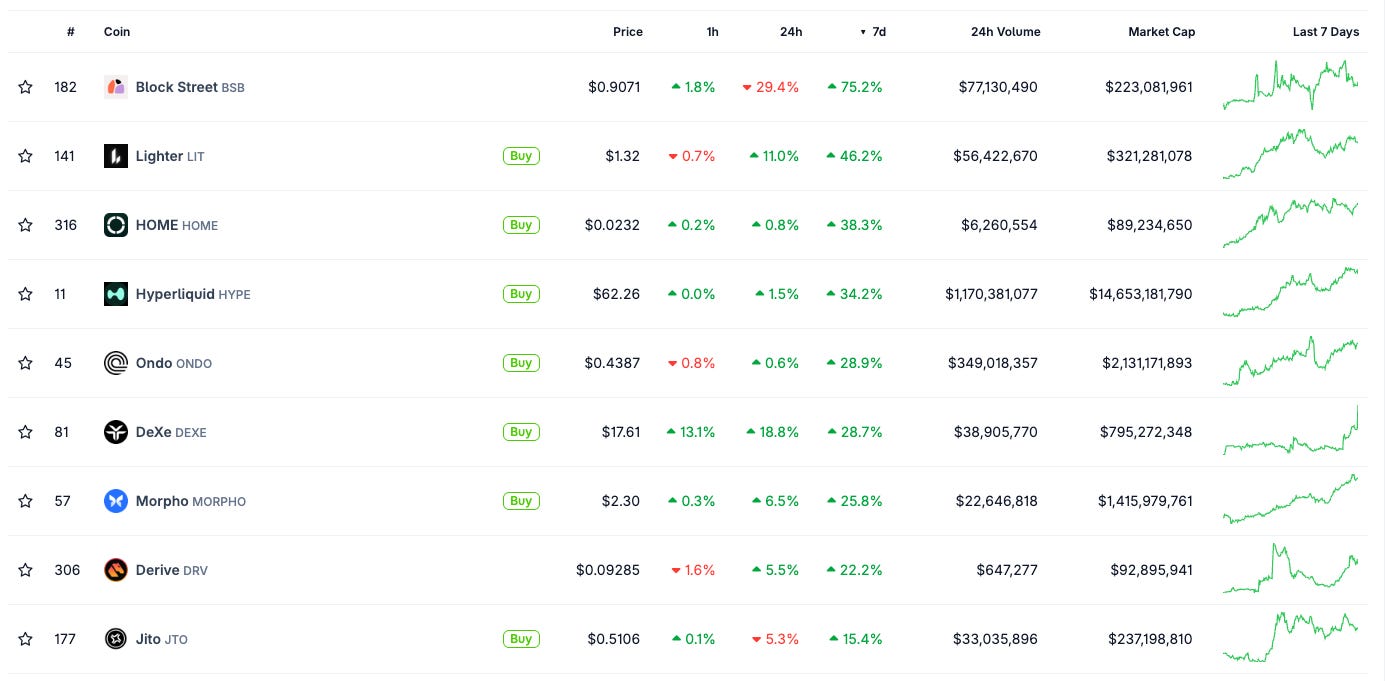

$HYPE +25.4%, $13.37B cap.

The dominant large-cap signal this week. The catalyst stack from last week’s AQAv2 with Coinbase + Circle staking HYPE, The AQAv2 deal shares ~90% of cost-adjusted yield back to Hyperliquid. At $5B base(from DeFillama), this brings the estimated the $137M–$160M annualized revenue (before any growth in USDC supply) will be used for $HYPE buybacks

RWA open interest on Hyperliquid hit $2.6B ATH, as trade.xyz launched a SpaceX Pre-IPO Perpetual market (IPOP) on May 18.

HYP ETF launched on NYSE (May 15), pulling ~$70M of inflows + 10% annual fees are allocated to HYPE buys

a16z-linked wallet accumulated 2.11M HYPE (~$91M)

⚠️ Watch the unstaking queue. 7.51M HYPE unlocks over the next 7 days, with May 28 being the largest day at 4.02M tokens matured. Top 5 wallets account for 46.8% of all unstaking. Concentrated supply hitting at once is a near-term risk. Whether bearish depends on who the top wallets are.

Sources: Hyperliquid X, Derive X.

$LIT (Lighter) +24.7%, $312M cap.

Lighter launched RFQ on RWA markets in beta on May 21 — letting traders enter and exit larger RWA positions with lower slippage and better pricing through market maker quotes. Plus a Tealstreet integration giving Tealstreet traders direct Lighter market access.

Source: Lighter X.

$MORPHO +25.8%, $1.38B cap.

The Aave-to-Morpho migration narrative is still working, and this week brought concrete structural expansion:

Morpho launched live on Tempo (Stripe’s enterprise stablecoin payments L1) on May 18. Stripe’s enterprise users (DoorDash, Coastal Bank, others) can now lend idle stablecoin balances directly into Morpho through Tempo. Gauntlet and Sentora are the day-one curators. This is a real distribution channel — not just a chain deployment.

Wintermute added as a vault curator on Morpho.

The narrative remains: Aave’s structural issues are sticky, Morpho continues to capture migration capital, and the protocol now has Stripe-grade enterprise distribution.

Source: Morpho X.

$JTO +15.4%, $237M cap.

The Solana DeFi sentiment continues to support JTO. JTX (the trading app Jito is building) keeps shipping. The newer catalyst this week is Upshift, a vault infra platform originated on EVM, launches on Solana, with sJitoSOL as the first multi-strategy vault (targeting 6% APY, curated by Sentora). JitoSOL is also now available on Telegram Wallet at ~16% APY with a 10% bonus.

Sources: Jito X, Upshift X.

Other Trending Narratives

Privacy is having a moment.

NEAR +58% 7d and ZEC (Zcash) +27% 7d ($11B cap). NEAR is boosted by Rhea FInance launching perps on NEAR, while ZEC continues it’s structural increase.

AI infrastructure tokens continue their structural run.

VVV (Venice AI) +40% 7d and GRASS +69% 7d. Connects to the Base DEX volume story in Section 3 — VVV’s WETH/VVV pool on Aerodrome was a meaningful contributor to Base’s DEX volume flip of Ethereum. AI agent and AI infrastructure tokens have been gaining share consistently for weeks now.

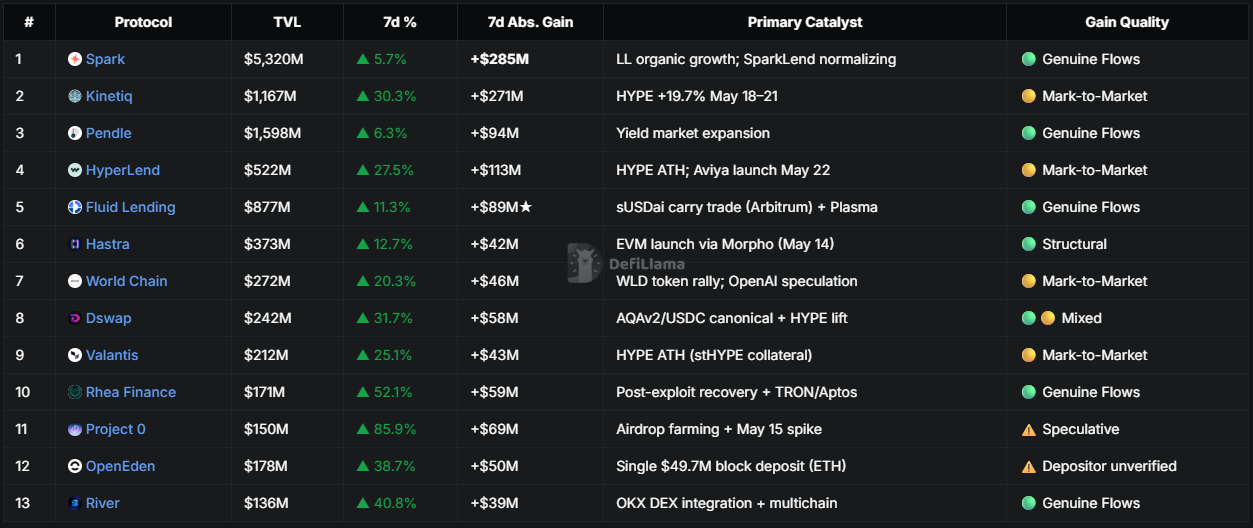

4B. TVL Gainers ($50M+ filter) — Ranked by absolute $ inflow.

The Hyperliquid Mark-to-Market Wave: $426M in Seven Days

Four Hyperliquid-native protocols collectively added $426M in TVL over seven days. The caveat is equally large: this is overwhelmingly HYPE price appreciation, not new capital.

HYPE moved from $45.63 on May 18 to $54.62 on May 21 (+19.69% in three days), then consolidated at $62.13 by May 25. These protocols hold HYPE-denominated assets; their USD TVL is a token price chart in DeFi clothing.

Kinetiq

+$271M The dominant HYPE liquid staking vault. A counterfactual isolating price effect vs. net flows shows implied net new deposits of just +$3.1M against a $271M reported gain. The remaining $268M is pure mark-to-market. Kinetiq is a HYPE price proxy, not a growth story.

HyperLend

+$112.5M The counterfactual is more revealing here: implied net flows of −$16.2M — users were actively withdrawing even as headline TVL rose, because HYPE’s price move fully masked the outflows. Aviya (HyperLend’s institutional fixed-rate credit facility) launched May 22 — a genuine product development, but too early to show in this week’s TVL.

Valantis

+$42.5M stHYPE-based vault, mechanically correlated to HYPE. No independent catalyst identified.

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.