Op-ed: Barbarians at the Gate: How RFV Plays Work in DeFi

-by Brook, Sr. Analyst and Danger, Founder.

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

Today’s News Headlines:

- CLARITY Act passed Senate committee vote

- Bitwise launches Hyperliquid spot ETF

- Upshift launches instant RWA redemption infra

- Hyperliquid transitions primary margin asset to USDC

- Lido resumes EarnETH with full protection

- Kelp reopens rsETH withdrawals and bridging

- Zest Protocol reveals ZEST tokenomics and airdrop

- Euler integrates CoW Protocol execution routing

- Hyperbridge patches forged proof exploit vulnerability

- RISE launches Treasury-backed USDR stablecoin

- Kalshi integrates with Interactive Brokers platform

- Yuzu launches leveraged YZM looping market

In the traditional finance world, when a company’s stock trades below the liquidation value of its assets, activist investors swoop in. They buy up shares, stage a boardroom coup, and force a payout. That playbook has now been ported to DeFi, where it goes by a different name: the Risk-Free Value, or RFV, event.

To understand the stakes, look at what just happened to Gnosis DAO.

The Siege of Gnosis DAO

In early May 2026, activist investors set their sights on Gnosis DAO. The premise was straightforward arithmetic: Gnosis sat on a treasury of roughly $223M, but its native token, GNO, was trading at a 24% discount to its underlying net asset value. The DAO had recently fired its long-time treasury manager Karpatkey (GIP-143, November 2025), and was funneling tens of millions of dollars annually into Gnosis Ltd, the operating company behind Safe, CoW Swap, Gnosis Chain, and Gnosis Pay — with limited revenue to show for it.

A community member known as Wismerhill submitted GIP-150, calling for a “one-time, opt-in pro-rata treasury redemption.” The argument: GNO trades at a persistent and widening discount, Gnosis Ltd has become a structural cash sink, and holders deserve the option to exit at NAV. The proposal sparked the same philosophical battle every RFV event sparks — is this a vital accountability mechanism, or an opportunistic attack on long-term builders?

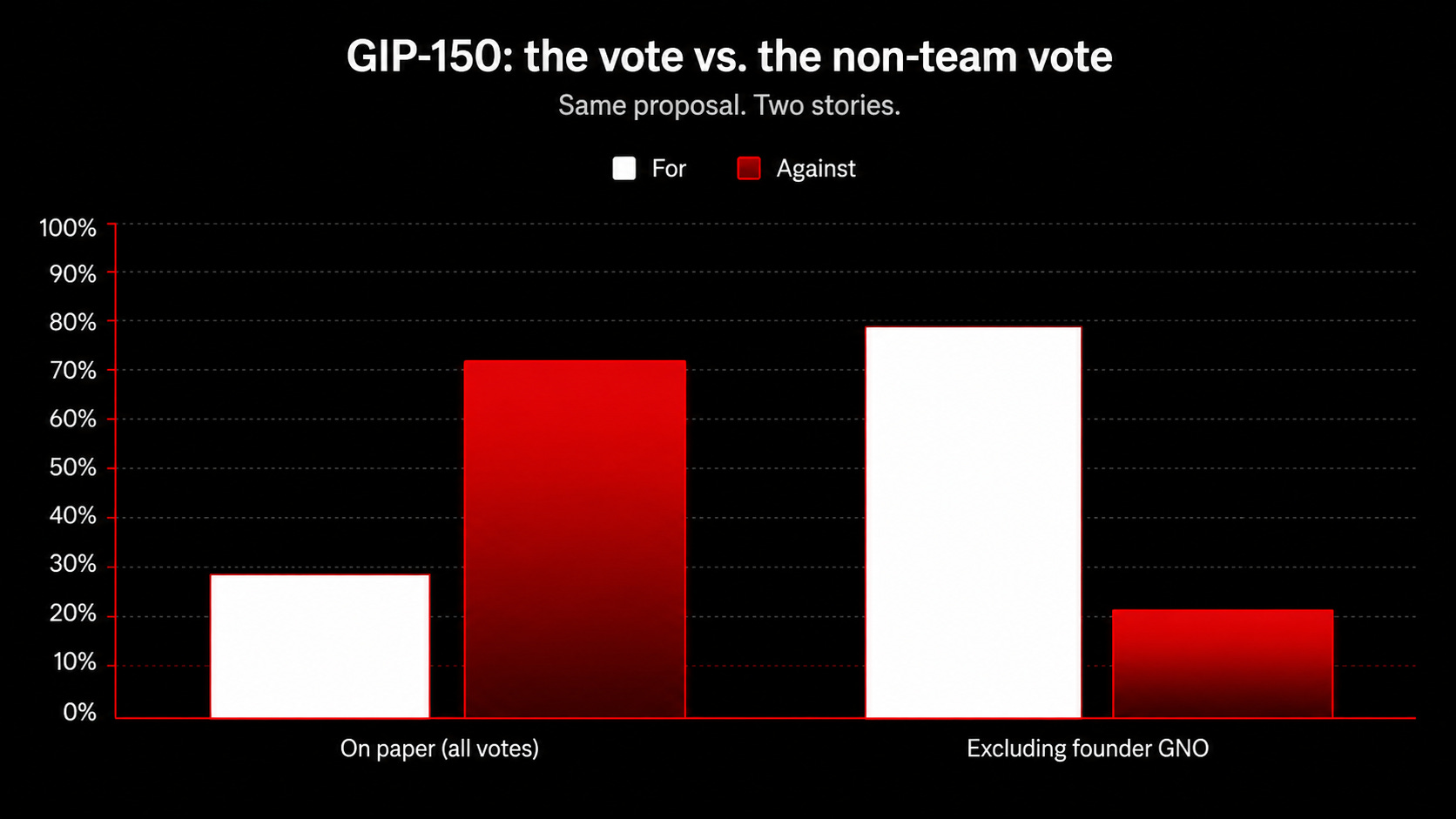

The vote closed on May 13, 2026. The headline result: rejected, 71.87% Against to 27.86% For, with 601,800 GNO cast (over 8x the quorum threshold).

But that headline obscures what actually happened.

What Is Risk-Free Value?

In crypto, RFV refers to the baseline, liquid value of a protocol’s treasury divided by the eligible supply of its governance token. When a token’s market capitalization falls below the dollar value of the assets it backs, the token trades at a discount. An RFV event is triggered when investors attempt to force the DAO to open its treasury and allow holders to burn their tokens for a pro-rata share of the underlying assets — capturing the spread, eliminating the discount, and disciplining whatever spending pattern created the gap in the first place.

The mechanism only works if the math is honest. Three valuation traps recur:

Circulating vs. fully diluted supply. Treasury divided by circulating market cap will almost always look like a discount; treasury divided by FDV is the only honest comparison, because unvested tokens have equal claim on the treasury once they unlock.

The DAO’s own token as treasury. Many DAO treasuries are dominated by holdings of the DAO’s own governance token. Counting those as backing creates a circular reference — the token is partially backed by itself.

Illiquid venture marks. Off-chain venture positions are typically marked at the operator’s internal valuation, which is unverifiable and often stale.

The cleanest RFV signal is treasury excluding the DAO’s own token, valued at on-chain liquid prices, compared against fully diluted valuation. Anything else either flatters the discount or hides it.

The Gnosis Blueprint

Looking under the hood of GIP-150 shows how a sophisticated RFV mechanism is actually designed. The Gnosis DAO treasury targeted by the activists comprised:

Liquid Positions (~$190.5M): $100M ETH, $1.5M BTC, $50M stablecoins, $35M altcoins, $4M RWA tokens.

Illiquid Positions (~$25M): Venture investments, marked at internal valuations.

The redemption math: 1,304,047 GNO eligible (excluding Gnosis Ltd’s holdings, on the grounds that Ltd already receives DAO funding directly), $190.5M of liquid value, $146 implied liquid redemption value per share. GNO traded at $132 during the vote, creating a clear arbitrage spread. For illiquid positions, redeeming holders would receive a gLTD-CLAIM token representing a future claim on venture realizations — a structurally elegant way to give exiting holders proportional exposure to assets that can’t be liquidated on-chain.

The opt-in design is what made the proposal distinct from earlier RFV plays. Non-participants keep their GNO and retain full economic exposure to whatever Gnosis Ltd builds going forward. Participants get out at NAV. The redemption isn’t a wind-down — it’s a release valve.

That design didn’t survive contact with the founders.

The Founder Vote

The clean 28/72 rejection looks decisive until you look at where the “Against” votes came from. Per Wismerhill’s post-vote analysis, the 432.5k GNO Against tally included roughly 385k GNO controlled by Gnosis Ltd cofounders — votes cast by the same individuals who serve as Ltd executives and whose operational latitude the proposal was designed to constrain.

The arithmetic, attributed to Wismerhill: subtract that 385k from the Against side, and the result among non-Ltd-affiliated holders flips to roughly 78% in favor. The founder GNO is held in personal wallets and is mechanically eligible to vote; nobody disputes that. The question is what conclusion to draw when the entire margin of defeat — and then some — comes from the votes of the people the proposal would have placed limits on.

DeFi analyst Ignas, who voted Against despite acknowledging the underlying logic, captured the steelman of the opposition: “In this case almost every DAO and projects beyond Hyperliquid and Tron should be shut down and Treasuries returned to token holders.” His concern was contagion — if Gnosis’s redemption passes, every DAO trading below NAV becomes a target, and protocols with real users like Gnosis Pay and Circles get defunded as collateral damage. That’s a defensible position from someone holding the token through the next cycle.

What’s harder to defend is what came next.

In the days following the vote, Gnosis leadership signaled a higher operational spending envelope for the next funding cycle, while rebuffing engagement on exit mechanisms or NAV-floor protections. The framing was that defeat of GIP-150 represented a mandate to continue current operations unchanged. Reading a result in which 78% of non-team holders signaled they want a path to realize NAV as authorization to increase spending is, charitably, a creative interpretation. Wismerhill has publicly given leadership one week to engage before filing a follow-up proposal.

A History of RFV Battles

Gnosis isn’t the first DAO to face this dynamic. Outcomes range from massive activist paydays to scorched-earth defenses.

Rook DAO (2023): The Raid

DeFi analyst Ignas famously labeled Rook’s situation a “slow rug” — $6.1M in annual spending on 22 contributors (nearly $300k each) while protocol volume collapsed 78%. Holders revolted, forced a shutdown, and unlocked the treasury for distribution. ROOK rallied 5x as holders claimed their payouts. The protocol died; the holders won.

FEI / Tribe (2022): The Graceful Exit

After a devastating hack and regulatory pressure, Tribe DAO chose pragmatic dissolution. The vote returned $220M to token holders. At the time of the vote, TRIBE traded at a $66M market cap; the decision to dissolve revalued the token to $128M. Holders trading well below book value were made whole almost overnight.

Aragon (2023): The Nuclear Option

Aragon — ironically, a protocol that built DAO infrastructure — bypassed its own decentralization to fend off a coordinated activist push led by Arca. Rather than letting holders capture funds through on-chain governance, the team unilaterally repurposed the treasury into a grants program and transferred funds to a centralized Swiss association. The defense worked tactically and failed strategically: the project shut down by late 2024, and ANT holders ultimately redeemed for ETH anyway. Aragon destroyed its own DAO to ensure the raiders lost, then died.

Beefy Finance (2026): The Proactive Shield

Facing a Binance delisting in April 2026 that pushed BIFI below intrinsic NAV, Beefy DAO acted before a vote was even needed. Through Snapshot, the DAO authorized its Treasury Council to conduct discretionary BIFI buybacks whenever the token traded below calculated fair value, funded by protocol revenue.

By repurchasing discounted tokens and holding them as non-circulating supply, Beefy closes the NAV gap continuously, on its own terms. The mechanism removes the economic incentive for an RFV raid by structurally preventing the discount from widening.

Beefy’s response is instructive because it’s the holder-friendly answer Gnosis leadership chose not to give. Activate a buyback program funded by protocol revenue. Commit to closing the NAV gap. Show holders that operational spending and value accrual aren’t in zero-sum tension. That response defuses an RFV raid because it removes the discount that creates the arbitrage. Gnosis’s response — more spending, no exit, no buyback floor — leaves the discount in place and the structural setup unchanged.

The Take-Home for Token Holders

RFV events function as DeFi’s immune system. Project teams understandably hate them — these proposals constrain operational discretion and put builders’ jobs at risk. From the team’s perspective, they look like raids.

From the token holder’s perspective, the calculus is different. An RFV proposal has two possible outcomes, both of which leave the holder structurally better off:

The proposal succeeds: holders capture the discount directly through redemption.

The proposal fails: a credible threat has been established, and serious teams respond with buybacks, dividends, or other NAV-closing mechanisms (the Beefy response). Teams that refuse to respond face follow-on proposals and ongoing accountability pressure.

The losing outcome for holders is when teams respond like Aragon — destroying the DAO to ensure the activists lose — or like Gnosis appears to be responding, by interpreting a 28/72 defeat as a mandate to spend more. In both cases, the underlying problem (capital trapped at a discount, controlled by entities that don’t credibly answer to holders) doesn’t get resolved.

Where the Next Raids Land

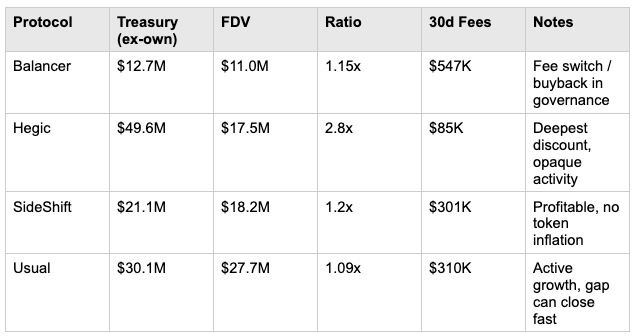

Per current DefiLlama data, several protocols sit clearly in RFV territory — treasury (excluding their own token) exceeds fully diluted valuation, meaning the non-own-token assets alone are worth more than the entire diluted market cap.

The standout candidates as of May 2026:

Balancer is the standout. With $112M TVL, $547k in 30-day fees, and a long-running governance discussion around fee switches and BAL buybacks, the catalyst is identifiable and the discount is modest enough that a credible buyback program could close it cleanly.

Hegic is the most extreme at 2.8x, but options-protocol opacity and modest fee run-rate make it deep value or value trap depending on whether options volume recovers.

SideShift is the cleanest profile of the group: working business, clean treasury, durable revenue, no token inflation.

Usual is the most dynamic entry — the RFV gap is small enough that it could close in either direction quickly.

Watch list — approaching the threshold rather than across it: Overtime (0.72x) and Badger DAO (0.57x).

The pattern that makes an RFV trade actionable rather than just a sitting discount: governance discussions around fee switches, buyback programs, or revenue distribution. The protocols above with active fee accrual and live governance debate (Balancer, Usual, SideShift) carry better risk/reward than the zombies (QiDao at 5.3x but zero fees, ETH Strategy at 1.3x but no fee accrual).

The threat of an RFV raid keeps the industry honest. It reminds teams that operational discretion isn’t unlimited, that builders ultimately work for holders, and that capital trapped at a discount belongs to the people who funded it. Gnosis just demonstrated what happens when a DAO with concentrated founder voting power tries to interpret a clear holder signal as endorsement of the status quo. The next move belongs to Wismerhill & Chud — and the holders they’re organizing.

For sponsorships, questions, or news tips, reach us at: support@todayindefi.com

Stablecoin LP for 21% APY

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.