Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Headlines:

- Summer.fi Lazy Summer Vault Exploited

- DeFi Saver Disables Summer Vault Deposits

- BonkDAO Treasury Drained in Governance Attack

- Aave V4 Expansion Proposed on Avalanche

- Spark Proposes Robinhood Chain Integration

- Neverland Boosts Monad Lending Yields

- Ondo Perps Launches With 20x Leverage

- Sky Launches GROVE Token Rewards

- ENS Proposal Targets Governance Revival

Key Takeaways:

1. Macro turned into a tailwind for crypto — for the first time since March.

June payrolls came in soft (57K vs ~115K), pushing out rate-hike bets and finally giving crypto a liquidity backdrop, while the AI trade cracked and crypto outperformed equities. Still a relief rally, not a confirmed turn as stablecoin supply is still contracting and funding has run ahead of spot, so the bounce is leverage-led. June CPI (July 14) is the test.

2. The movers ran on Robinhood — and two catalysts are still ahead.

Lighter, Maple, and Ether.fi all moved on Robinhood’s DeFi launch, the week’s dominant catalyst. The fresher stories are Pyth finalizing a Nasdaq data integration, and Aerodrome is framing an Ethereum mainnet expansion — roughly 10x its addressable market versus Base.

3. The chain story was yield, on two venues.

Monad’s Aave v3 deployment crossed $100M in deposits within 48 hours, with stablecoin lending running ~5–6%; Robinhood Chain’s Morpho vault pays 7% on USDG — or 15–20% looped. The mechanics and the one flow story that survived scrutiny this week are in Section 3.

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

DeFi Token Price Movers - Observations, not trade ideas.

Lighter — LIT, +39% (7d). The top mover, on the Robinhood integration: Robinhood Wallet now offers native in-app perps and tokenized-stock trading powered by Lighter, on a dedicated instance built for Robinhood Chain, using USDG as the quote asset. Their first “Lighter Domain” — a separate execution/liquidity instance per partner. A direct pipe to Robinhood’s retail base.

Ether.fi — ETHFI, +35% (7d). Two drivers. It proposed a dedicated Aave V4 instance on OP Mainnet to power ether.fi Cash — up to $175M in launch assets, GHO integration, 20% revenue share to the Aave DAO. And the fundamental case sharpened: Cash is now 60%+ of ether.fi’s revenue, outweighing the original staking business — the “onchain bank” pivot is showing up in the numbers.

Maple — SYRUP, +20.3% (7d). Same Robinhood catalyst, credit side: syrupUSDG and syrupUSDC went live on Robinhood Chain, and Steakhouse approved syrupUSDG as collateral for the vault behind Robinhood Earn. So Maple’s institutional lending is now a yield source inside the 7% Robinhood product — real new distribution, not just an announcement.

Aerodrome — AERO, +19.7% (7d). No single headline — a steady drumbeat of fundamentals: programmatic buybacks (216K AERO bought and max-locked this week, ~200M to date), ~50% of supply locked at ~3.6-year average, and capital-efficiency wins (MEV-resistant pools, protocol liquidity migrating in). A “the flywheel is working” week rather than a catalyst spike.

Pyth Network — PYTH, +27.6% (7d). Pyth confirmed it is finalizing integration and commercial terms with Nasdaq to bring TotalView market data to the Pyth marketplace, following a teaser that drew stronger interest than anticipated. The network also expanded Pyth Pro coverage across commodity futures, Hong Kong and China equities, and 24/5 US equities. The Nasdaq relationship is the driver.

1A. Traditional Macro

FRED:WALCL-(FRED:RRPONTSYD+FRED:WTREGEN)

Net liquidity: ~$6.72T, above the 20-week EMA. SUPPORTIVE. Liquidity is grinding higher and holding above its moving average — the tailwind that’s been absent for weeks is back. This is the quiet structural support underneath the week’s relief rally: rising liquidity plus falling rate-hike odds is exactly the backdrop risk assets want.

BTC/NQ ratio

BTC/NQ ratio: first meaningful green candle since early March. IMPROVING — the highlight. This is the week’s standout. After months of crypto underperforming tech, the ratio finally turned up, and the driver is exactly the divergence in Key Drivers: crypto rallied on the dovish jobs data while the Nasdaq sold off on the AI/chip unwind. It’s the first real sign since March that capital is rotating back toward crypto relative to equities — one candle, not yet a trend, but a genuine shift in direction.

The jobs report cracked the hawkish narrative.

June nonfarm payrolls rose just 57K versus ~115K expected, with April and May revised down by 74K combined. Although unemployment dipped to 4.2%, it was driven by labor-force participation falling to its lowest level since March 2021, while the household survey showed 507K fewer people employed.

The weak labor data eased pressure on the Fed, pushed Treasury yields and the dollar lower, and prompted markets to price out a September rate hike—providing the liquidity tailwind crypto had been waiting for. The move was reinforced a day earlier when Fed Chair Warsh said inflation risks had eased, helping Bitcoin reclaim $61K even before payrolls were released.

Another overhang disappeared. Strategy (MSTR), the largest corporate Bitcoin holder, secured roughly 26 months of dividend coverage with $2.55B in cash, the option to sell up to $1.25B of BTC if needed, and $2B in authorized buybacks. The move eased concerns that a prolonged Bitcoin downturn could force large BTC sales, removing a key market overhang. MSTR rose 7–10% on the announcement, reflecting improved confidence rather than expectations of new Bitcoin purchases.

Bottom line: the Fed narrative softened, the AI trade cracked, ETF outflows finally reversed, and Strategy removed a major forced-selling concern. For the first time since March, macro conditions turned into a tailwind for crypto instead of a headwind.

Composite: liquidity supportive, rates consolidating (no longer actively tightening), and crypto outperforming equities for the first time since March. A clear improvement from last week, where every lever pointed against crypto — the backdrop has flipped from headwind to tentative tailwind.

1B. Crypto Capital On-Ramp

Total stablecoin supply 7d change (level + WoW)

Total stablecoin supply: −$1.45B (~−0.4%). CONTRACTING, but easing. Still negative, though a clear improvement from last week’s −$2.43B, and once again the drain is concentrated in the two transactional giants, USDT and USDC.

ETF flows

ETF flows — still negative, but sharply improving. Spot ETFs saw Bitcoin −$231M, Ethereum −$29.9M, and Solana +$5.5M for June 29–July 5 — still a net outflow, but a fraction of last week’s −$2.06B, and the 10-day, $2.7B outflow streak broke mid-week with a +$222M inflow on July 2. The first real sign institutional selling is abating, with Solana back to small inflows.

1C. Week-Ahead Catalysts

June CPI — Tuesday, July 14. The soft-labor read means little if inflation stays hot — a cool CPI extends the relief rally and cements the “hikes are off the table” case; a hot one revives them and likely reverses this week’s move.

Section 2 — Onchain Risk Regime

Individual Stablecoins Flows

USDGO added $113.7M (+15.24%), the fastest-growing dollar in the set for a second consecutive week, driven by yield-farming incentives. Note that USDGO is a separate, newer token from Paxos’ USDG, the stablecoin Robinhood integrated — different issuers and different products, despite the similar tickers.

Robinhood’s chain is integrating USDG as one of its main transactional stablecoin. BUIDL (BlackRock) added +$42.9M and AUSD +$8.9M (+4.89%), the tokenized-yield tier quietly compounding.

The drain, again, is the transactional and the recently-hot: USDT −$1.67B and USDC −$713M led the outflows — the same two giants behind the total-supply contraction in Section 1 — while RLUSD −$186M (−11.65%) and USDS −$267M gave back ground.

Aave / Sphere Rates

Funding crossed above the borrow rate: 6.28% vs 4.23% (supply 3.20%). The four-week climb completed — leverage longs are now expensive, perps are relatively crowded with longs. Historically, funding above borrow is a caution, not a buy: it shows up after a bounce, not before one. Read it as “don’t chase” — the rally is leverage-led, not spot-led.

ETHBTC vs 20W MA

ETHBTC printed its biggest green weekly candle in months, pushing back up toward its 20-week moving average after months of grinding lower. ETH outperformed BTC (the +5% sessions during the jobs-data rally), and because ETHBTC is a rough risk-appetite gauge for the whole alt complex, a move this size gives alts room to run.

It’s still testing the 20W MA rather than clearing it, so it’s not yet a confirmed regime change — but it’s the most convincing step toward one since the spring.

Verdict: Onchain regime — IMPROVING, but leverage-led.

The constructive signals are real: ETHBTC’s strongest candle in months points to alts getting room, and the price tone flipped up with macro. But the composition is the catch — funding crossed above the borrow rate (a historically cautionary, crowded-long reading), and stablecoin supply is still contracting, so the bounce is running on leverage rather than fresh spot capital. A real improvement in direction, but a crowded one: alts have room, yet the setup rewards patience over chasing.

Section 3 — Chain Comparison

3A. Stablecoin flows by chain

DefiLlama’s raw chain-level stablecoin rankings for the week showed dramatic movement — Polygon appearing to add $1.64B (+14.5%), Plasma appearing to shed 18% of its base.

Almost none of that is real dollar flow. It is a byproduct of summing stablecoin token units across currencies with wildly different per-unit values — yen-pegged JPYC and lira-pegged TRYB alongside dollar stablecoins — which turns a modest local mint or burn into an apparently enormous headline number.

After deduplicating and re-denominating every mover to actual USD value, the picture is far more modest: most “gainer” and “loser” chains moved single-digit percentages.

Two stories survive scrutiny as genuine, dated events: Ripple’s deliberate rebalancing of RLUSD issuance from Ethereum toward the XRP Ledger, and Hyperliquid’s coordinated wind-down of its native USDH stablecoin in favor of USDC. Everything else in this week’s raw rankings is better read as issuance mechanics, incentive-driven float, or measurement artifact rather than organic demand growth.

Monad: Aave V3 Incentive-Subsidized Borrow Costs Keep Lending Yield Attractive

Monad’s stablecoin lending market benefits from the combination of Aave v3’s recent deployment on the chain alongside syrupUSDC’s presence on the same chain. Live Merkl incentive rewards on Aave v3 Monad for USDT, USDC, and AUSD supply are currently helping to keep borrowing costs low, which in turn supports attractive economics for syrupUSDC lending on top of that base. Average stablecoin lending APY on Aave v3 Monad is currently running approximately 5–6% with the max syrupUSDC loop ROE ~20%.

Robinhood Chain: The Morpho Vault Behind Robinhood Earn’s Yield

The relevant venue here is the Morpho vault underlying Robinhood Earn. Users can post syrupUSDG, USDe, or spUSDG as collateral to borrow USDG from that market and loop the position for amplified yield. Separately, users can supply USDG directly through the Robinhood app into the same vault for a simpler, unlevered 7% APY.

Collateral-side yields are currently: syrupUSDG approximately 4.6%, USDe approximately 4.5%, and spUSDG approximately 4.2%. Return on equity for the looped strategy is currently in the 15–20% range, reflecting the spread between the 7% USDG supply rate and the sub-5% cost of the collateral assets used to borrow against, before accounting for looping leverage.

Polygon: The Headline Number Was Almost Entirely a Currency-Unit Artifact

Polygon topped the raw gainer list at +$1.64B (+14.5% week-on-week) — a number that does not survive contact with the underlying token-level data.

The real driver was a single JPYC mint on June 30 that moved supply from 2.27B to 3.07B units in one day — a step change in unit count, not organic growth. At roughly $0.006 per unit, that ~800M-unit mint is worth approximately $4.9M, not the billions implied by summing raw token counts across currencies with different face values.

Once re-denominated to USD and deduplicated for tokens double-counted under two parallel identifiers, Polygon’s actual weekly picture is: USDC +$50.4M (+2.8%), USDT +$9.3M (+1.0%), JPYC +$4.9M, offset by DAI −$33.2M (−5.5%) — for net real growth of approximately +$28M, roughly 1.7% of the originally reported figure.

Polygon does have a live payments narrative in the background — Visa’s multi-chain stablecoin settlement pilot and Polygon’s “Open Money Stack” rollout both fall in or near this window — but no source ties either directly to this week’s USDC or JPYC movement. Treat that context as background, not a confirmed catalyst for this specific week’s number, pending a dedicated check.

Ethereum & XRP Ledger: One Confirmed Rebalancing Story, One Broad Retreat

The market had speculated that Ripple was deliberately shifting RLUSD issuance away from Ethereum toward its native ledger. That story checks out — and independent verification adds useful precision the original data pull didn’t have.

Ethereum’s broad retreat (−$5.17B weekly decline) is confirmed as spread across USDT (−$991M), USDC (−$726M), USDS (−$254M), USDTB (−$184M), and USD1 (−$151M) — a market-wide stablecoin pullback on Ethereum, not a single-issuer event. RLUSD’s contribution to that Ethereum decline is a real but small share of the total move.

The RLUSD/XRPL flip is confirmed, with an important nuance the original draft didn’t capture: it is substantially engineered, not organically driven. RLUSD crossed over to hold a larger balance on XRPL than on Ethereum for the first time around June 24–25. But Ripple burned approximately $539M of RLUSD across both chains over the trailing month, and roughly 75% of that burn came off Ethereum specifically — meaning the “flip” happened predominantly because Ripple drained the Ethereum side, not because new external dollars arrived on XRPL.

RLUSD’s total supply is actually down roughly 11% from its early-June peak near $1.8B. The timing lines up with two regulatory catalysts: RLUSD’s Japan launch with SBI Group (June 24, pending JFSA approval) and a preliminary MiCA CASP license from Luxembourg (June 23) — both plausible motivations for Ripple to consolidate issuance on its own ledger ahead of new regulated distribution.

3B. Structural Shifts- DeFi Categories by TVL

The week’s onchain activity reflected price appreciation and isolated deals rather than broad structural conviction.

Perpetuals contracted sector-wide, with 19 of the top 30 venues down over 30 days and the three largest — Hyperliquid, Aster, and Lighter — negative on both fees and volume.

Lending TVL growth was largely a function of ETH’s 12.4% weekly move: every major lender except Dolomite grew less than collateral appreciation alone would predict, implying deposits likely fell in unit terms.

The genuine strength was concentrated in institutional credit. Centrifuge (+317% weekly fees) closed a Kraken Custody integration for its Janus Henderson CLO fund and brought a New York Life fixed-income strategy onchain; Maple (+107%) closed its warehouse facility with Kraken; and Spiko (+692%) launched its Solana fund with Coinbase’s stablecoin rails. All three are dated, verified transactions — though together the three protocols hold under 17% of RWA TVL, a cluster rather than a wave. Maple is the one name in the dataset where fundamentals are outrunning the token.

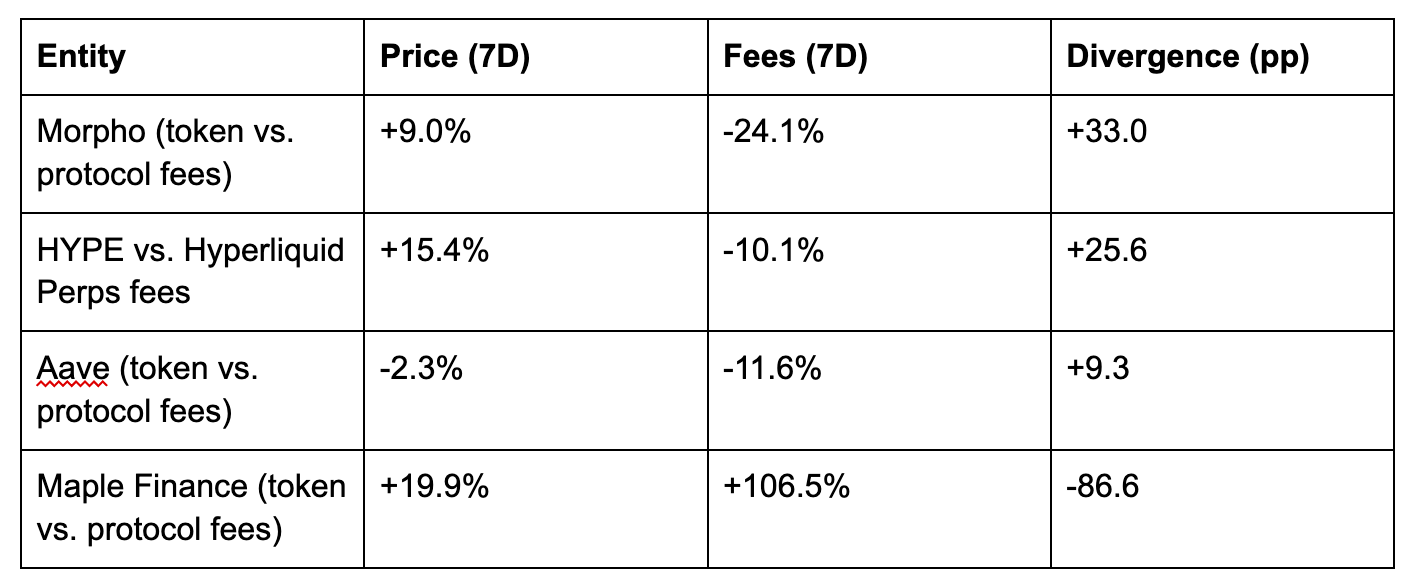

Price vs. Fundamentals: Where the Gap Is Widest:

The widest gap between price and fundamentals is in HYPE, up 15% while Hyperliquid’s fees decline 10%.

A positive divergence indicates the token price is outpacing underlying protocol fee generation; a negative divergence indicates fees are outpacing price. Maple is the one case in this table where the fundamentals are outrunning the token price — in every other row, the price is ahead of what the underlying business is currently doing.

Ahead: DTCC’s tokenization pilot — Russell 1000 constituents, major ETFs, and Treasuries — begins limited production trades this month, with BlackRock, Goldman Sachs, JPMorgan, Circle, and Ondo in the working group.

Section 4 — Project & Protocol Discovery

TVL Gainers ($50M+ filter) — Ranked by absolute $ inflow.

A broad crypto rally — ETH, SOL, and HYPE all up double digits on a 7-day basis, BTC up mid-single digits — lifted nearly every staking and lending protocol’s headline TVL this week. That makes this a poor week to take gainers rankings at face value: repricing of existing collateral and genuine new deposits look identical on a bar chart.

This week’s clearest growth story is not retail incentive farming but institutional distribution rails going live in the same seven-day window — Robinhood Earn, MetaMask’s Money Account, and Aave’s own Monad anchor-tenant deployment all launched within days of each other, each backed by verifiable press releases and on-chain data.

I. Lending & Money Markets — the cluster with the clearest real catalysts

This is the most convincing bucket on the screen, anchored by a single event: Robinhood Earn went live July 1, 2026, built as a multi-protocol credit stack rather than a single-venue product.

Morpho (+7.84% 7D, +$517M). Robinhood Earn routes eligible U.S. users’ USDG deposits into a Morpho Vault curated by Steakhouse Financial, with Robinhood Chain serving as settlement layer; borrowers post collateral via Spark, Ethena, and Maple to draw the USDG that generates depositor yield. The launch follows a $175M raise for Morpho Association on June 9, co-led by Paradigm, a16z, and Ribbit Capital — total funds raised across the round now exceed $250M with Apollo Funds, Circle Ventures, and VanEck also participating — explicitly framed by Morpho as accelerating its position as core credit infrastructure for mainstream retail platforms.

Spark (+1.66% 7D — the smallest mover in the group despite sharing the same catalyst). Spark is a borrower in the Robinhood Earn stack rather than a direct destination for user deposits, which likely explains the muted TVL response relative to Morpho. Spark holds roughly 20% of ecosystem TVL among yield-bearing stablecoin-backing assets on Robinhood Chain, with its spUSDG asset the largest such asset at approximately $11M as of July 3 — a modest base that leaves this catalyst mostly still ahead of it rather than behind it.

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.