Spark Gains as Aave Deals with KelpDAO Fallout, and more..

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

In this letter, we bring you the best bottom-up analysis of onchain trends, along with top-down market analysis, helping you find top yield opportunities and position for trends before they happen

1. Broader Market Outlook

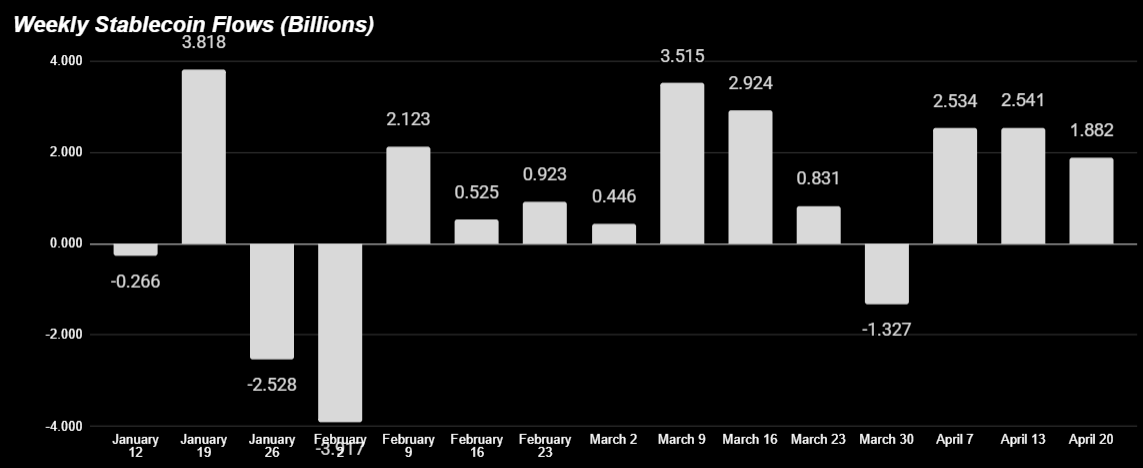

2. Stablecoin Flows, and stablecoin-specific flows

3. Stablecoin flows per chain

4. Perps and DEX Volumes Analysis

5. TVL gainers - for protocols above $100M

6. DeFi token price gainers & their catalysts

Key Takeaways:

1. The Aave WETH crisis is this week’s dominant event

A $292M Kelp DAO bridge exploit locked Aave’s WETH markets at 100% utilization across 5 chains, triggering $8.45B in outflows over 48 hours and $13.21B in total DeFi TVL drop.

Borrow APYs spiked across every major credit protocol. The actionable insight: Yields are high, but check rsETH first and second order exposure before lending this week - and monitor liquidity.

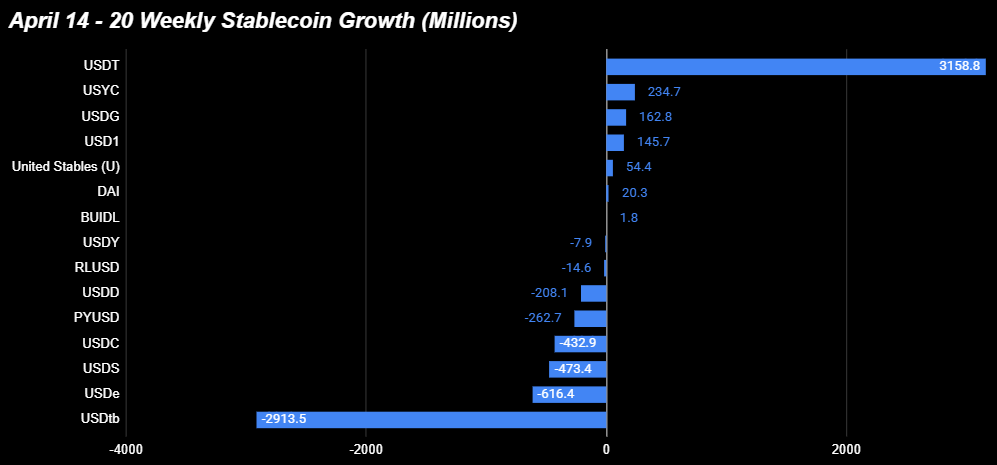

2. Stablecoin rotation has a mixed signal — RWA-backed stables is winning.

Flows are still decent at +$1.8B (+0.53%), USDT absorbed +$3B, as USDS lost $797.5M). Crypto-native stablecoins (USDC, USDe, USDD) all contracted; regulated/backed tier (USYC, USDG, PYUSD, BUIDL) gained $600M+ combined.

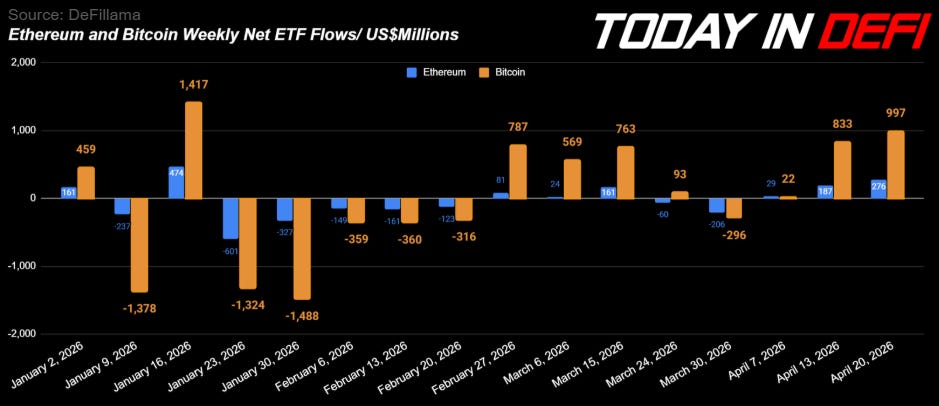

3. ETF flows hit a 13-week high during the chaos — institutions front-running 29 April FOMC?

BTC +$997M, ETH +$276M. Combined $1.27B, second straight week of $1B+ combined inflows. Happening during the Aave crisis and Hormuz tensions.

⚠️Kelp DAO’s rsETH Exploit:

KelpDAO’s rsETH bridge was drained for ~$292M via a LayerZero configuration flaw, allowing an attacker to mint ~116,500 unbacked rsETH (~18% of supply) by forging cross-chain messages with no ETH backing.

The attacker deposited the unbacked rsETH into Aave, Compound, and Euler, borrowing ~$236M in WETH before the protocol paused.

Bad debt:

Aave: $177M–$196M

Compound: ~$39M

Euler: <$1M

Whether bad debt will actually hit depositors is still being worked out.

First order effects

Aave WETH pool hit 100% utilization → withdrawals halted

~$8.45B exited Aave within 48 hours

Total DeFi TVL fell ~$13.2B

AAVE dropped 18%

Contagion spread quickly, with 20+ protocols pausing LayerZero bridges as a precaution. Cross-chain impact remains uncertain, as rsETH backing across 20+ networks is now in question, with no confirmed loss distribution plan yet.

Second-order effects:

Stablecoin borrow rates are surging as users exit Aave WETH positions by borrowing stables, pushing utilization near 100% across markets.

Leverage strategies have flipped to negative carry, forcing widespread unwinds that further drain liquidity and reinforce the rate spike.

USDe supply fell ~$600M as high borrow rates make Ethena leverage unprofitable.

The actionable takeaway

⚠️ Liquidity is thin in lending markets this week. High yields on supply are real, but they come with real bad debt risk — you could end up stuck, same as the Aave WETH suppliers. Make sure you know what you’re lending against, or just avoid lending this week until liquidity returns.

The cleanest playbook:

Don’t enter new lending positions on any protocol or market with rsETH or second order exposure until there’s a clear reconciliation and bad debt resolution

If you’re already stuck in Aave WETH, consider Fluid’s redemption protocol or 1inch’s secondary market exit

Watch USDe supply next week as the leading indicator — when that stabilizes, credit markets are healing

Spark, LPing, and fully backed RWA plays (regulated stables, T-bill-backed) are safer yield venues this week

Exit options for stuck WETH lenders

If you’re trapped in Aave’s WETH pool, two venues opened up:

Fluid launched an aWETH Redemption Protocol — lets Aave ETH lenders exit directly into wstETH or weETH. $1B initial capacity, supported by Lido and Ether.fi.

1inch enables swapping aEthWETH for WETH on the secondary market at a ~2% discount

Trading Calendar 🗓️

Mon–Tue — Retail Sales (March), rescheduled from April 16. The first demand read covering the period after the oil-price spike. A soft print reinforces the slowdown narrative.

Mon–Tue, Apr 28-29 — FOMC meeting. Markets pricing a 98% probability the Fed holds at 3.50-3.75%. The surprise risk is hawkish language on oil pass-through inflation.

The geopolitical whipsaw, round 2

BTC and risky assets responded positively even though uncertainty looms on Iran-Israel’s ceasefire agreements. The difference this time is that the market has already seen this movie once. Positioning is tighter, leverage is cleaner, and ETF flows are doing heavy lifting on the bid.

Which brings us to the one data point worth flagging:

ETF Flows — Highest Inflows in 13 Weeks.

Weekly spot ETF flows: BTC +$997M, ETH +$276M. Combined $1.27B — second straight week of $1B+ inflows. The narrative “institutions front-run the Fed” is playing out in real time. This is happening during a geopolitical shock. That’s the signal.

1. Stablecoin Flows

Weekly flow: +$1.8B (+0.53%). The third consecutive positive print on April, after April 7 ($2.5B) and March 2 ($2.5B). Broader views are still positive since it’s only a minor step down from two straight $2.5B+ weeks.

The headline number hides a bigger story. Underneath, there’s a large rotation happening:

USDT led with +$3B — its largest weekly print of the year. When the biggest fiat-backed stablecoin absorbs this much flow during a risk-on week, it usually means capital is deploying.

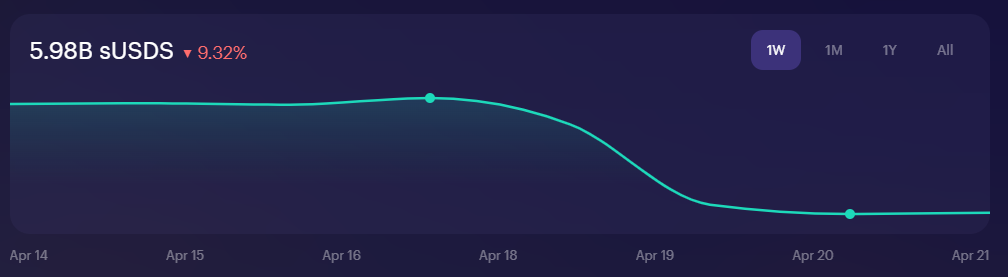

USDS lost $473M. This is the move of the week. Sky went from leading inflows in early April (+$593.9M on April 7) to the largest weekly outflow on the entire chart.

sUSDS supply contracted by almost $700M. Large withdrawals from sUSDS — the standard Sky savings product historically means a risk-on stance, as usually sUSDS becomes the main destination for stable and proven yields

USDe supply is cratering as a direct consequence on KelpDAO’s exploit. Ethena’s synthetic dollar dropped $616M this week — the third-largest stablecoin outflow. Farmers leverage up on sUSDE both for direct yield and for Ethena’s “Liquid leverage” farming program — which is now unprofitable.

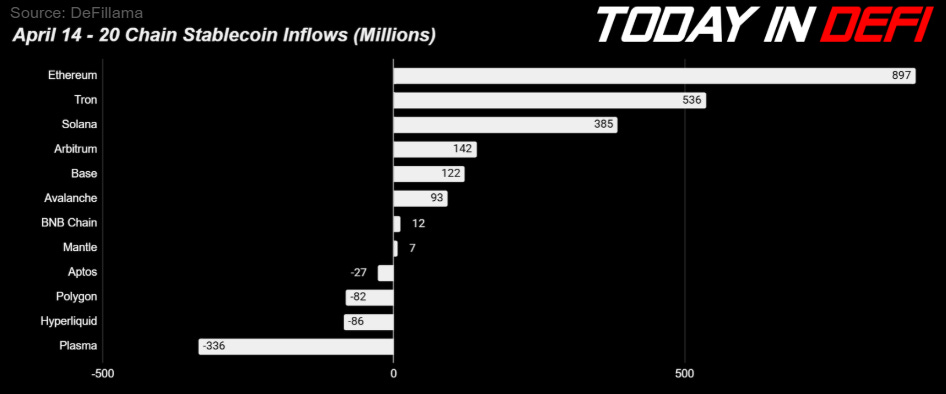

2. Stablecoin Flows Per Chain✅

Ethereum led with +$897M. Flat vs last week ($966M). The pattern holds — ETH keeps absorbing institutional flows regardless of market conditions.

Tron +$536M keeps its place as the emerging-markets dollar rail. USDT expansion on Tron explains most of this directly — when USDT grows $2.78B in a week and Ethereum takes a big chunk, Tron naturally takes the second-largest share.

Solana +$385M. Down from $545M last week. Part of this is the Drift exploit still weighing on borrowing yields, part is general risk-off. The xStocks still leads TVL growth on Solana, Loopscale, and Kamino loops are still live, but new capital is coming in more slowly.

Now the negatives worth talking about:

Plasma: -$336M (23.3%). The biggest outflow on the board. Plasma is a newer stablecoin-focused chain that had been pulling in flows on launch incentives. A $336M weekly drop suggests either incentives ran out, a large user withdrew, or early positioners are rotating into more established yield venues.

Source link: [DeFillama]

Important Notes for Chains:

Although some chains are seeing strong stablecoin inflows similar to Ethereum, Arbitrum, Tron, and Solana, significant risks still loom over lending and borrowing markets on Aave, Euler, Compound, and other credit protocols. This includes Fluid, which is also being affected by concerns around rsETH as collateral.

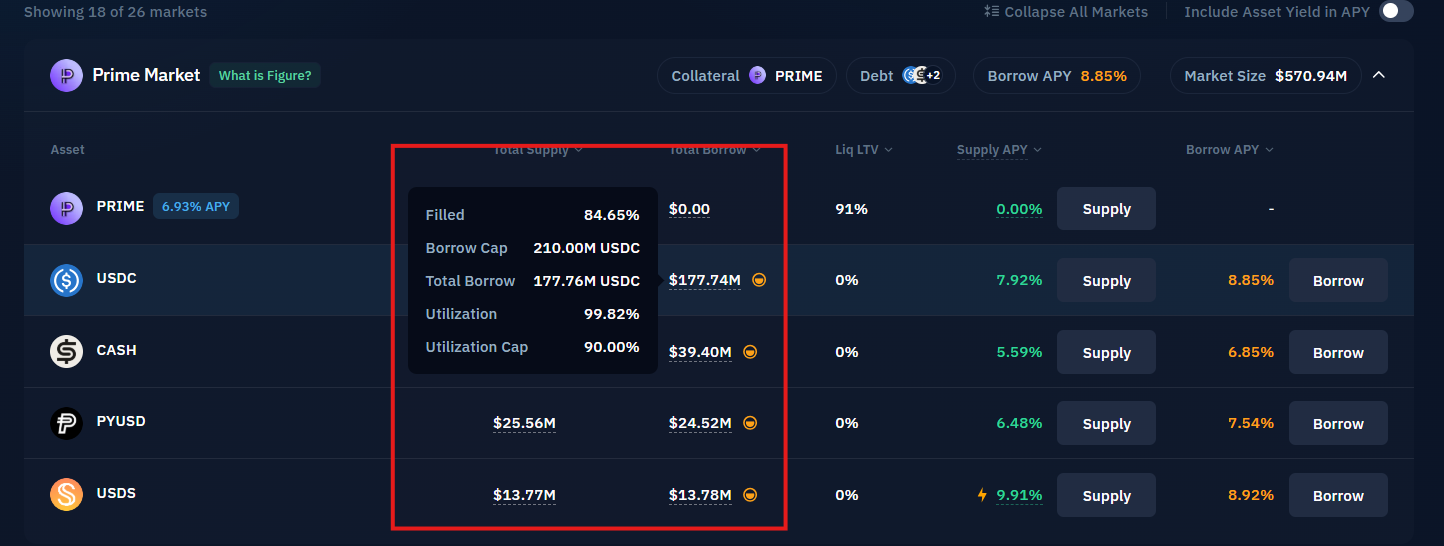

Most credit protocols are facing the same issue: stablecoin liquidity is drying up. Borrow rates have spiked due to high utilization. This is not limited to Aave, Compound, and Euler — borrowing rates on Solana’s largest credit market, Kamino, are also under pressure. USDC borrowing on Kamino has reached a 99.82% utilization rate, pushing borrow APY above 8%.

While high lending or supply rates may appear attractive for >8%, it is important to note the increased risk of bad debt. This means suppliers may not be able to recover their funds if borrowers are unable to repay their loans.

3. DEX Volumes Analysis

DEX volume worth highlighting: Base out-traded BSC for the second straight week ($6.71B vs $6.18B). The Aerodrome-Velodrome merger (Q2 2026) gets more valuable every week Base holds this lead — AERO captures 100% of DEX fees via ve(3,3). [LINK TO AERODROME]

Solana is also worth noting: weekly volume dropped to $10.5B from much higher February highs ($27-33B). Solana DEX volume is still second in absolute terms, but the slowdown is real.

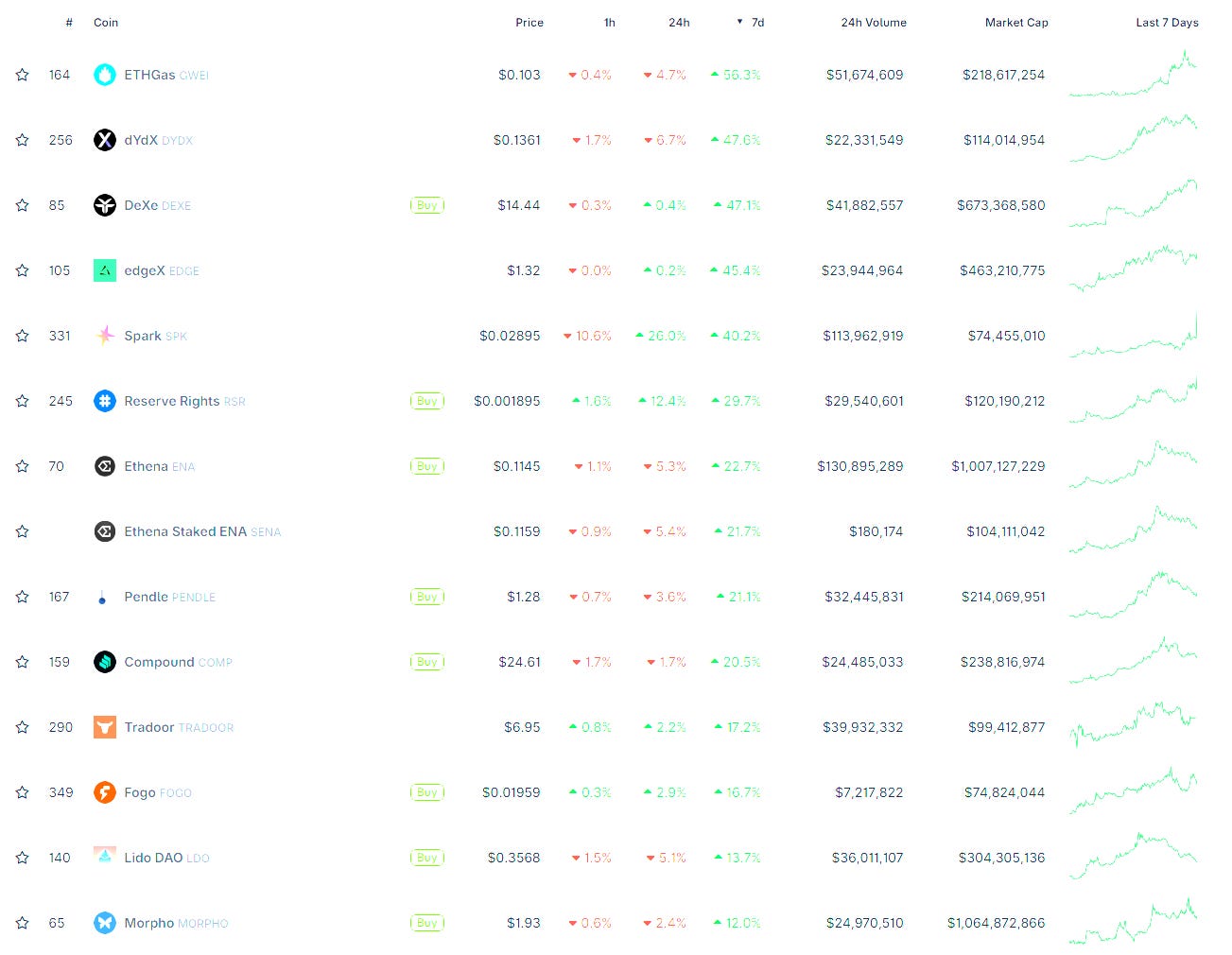

4. DeFi token price gainers & their catalysts

$DYDX (+47.6%) — WTI oil perps listing at the perfect time

The biggest driver: dYdX listed WTI oil perps. Given that the entire week is pricing the Hormuz situation and oil is the dominant global macro trade right now, this is possibly the best-timed product launch in DeFi this quarter. Traders who want 24/7 access to oil exposure — without traditional futures hours — now have an onchain venue. Hyperliquid doesn’t have this yet.

$edgeX (+45.4%) — Token utility expansion via Guardian Committee RFC

The real catalyst this week is the Edge Chain Guardian Committee and $EDGE Staking Framework RFC published April 15. This is a material utility expansion for the token beyond just fee discounts. Key elements:

DPoS staking + delegation — $EDGE holders can delegate to node operators

Top operators by stake form the Guardian Committee each epoch — committee handles data guardianship and cross-chain withdrawal approvals

Protocol revenue share for stakers (proportional to stake, subject to final reward rules)

Vested tokens can stake immediately — don’t have to wait for unlock, which removes a common reason tokens sit idle

Onchain governance in Phase 3 — full governance rights come later [LINK]

This matters because it gives $EDGE real economic utility. edgeX was already capturing the “perps DEX that isn’t Hyperliquid” trade on pure volume growth — now the token has staking revenue, committee economics, and a governance roadmap attached. That’s a fundamentally different investment case than just “high-beta to Hyperliquid.”

⚠️ Risk: This is an RFC (request for comment), not final implementation. Timing and final parameters could change based on community feedback.

$SPK (Spark) (+40.2%) — Buyback mechanics + vindication on risk management

Spark is Sky Protocol’s capital allocator. Three drivers this week, and the third is the biggest:

First buyback cycle completed April 6 — 572K USDS used to repurchase 26.6M SPK, directly cutting circulating supply.

Binance Wallet Spark Season 2 Vault launched March 26, giving out 7M SPK rewards through May 9 — active promotional pipeline.

Spark’s conservative risk policy got vindicated during the Aave illiquidity crisis. Following the Kelp DAO rsETH bridge exploit, Aave’s ETH markets locked up at 100% utilization across Mainnet, Arbitrum, Plasma, Mantle, and Base. Spark stayed liquid.

Their head of risk (Monet Supply) pointed out that Spark deprecated rsETH in January and kept a high max-rate on SparkLend ETH — a choice that cost them significant revenue to Aave over the past year, but means SparkLend has ample liquidity for ETH withdrawals right now, while Aave doesn’t.

⚠️ Risk: SPK has a 10B token max supply with only ~2.5B circulating. Every unlock is dilutive unless the buyback scales with emissions.

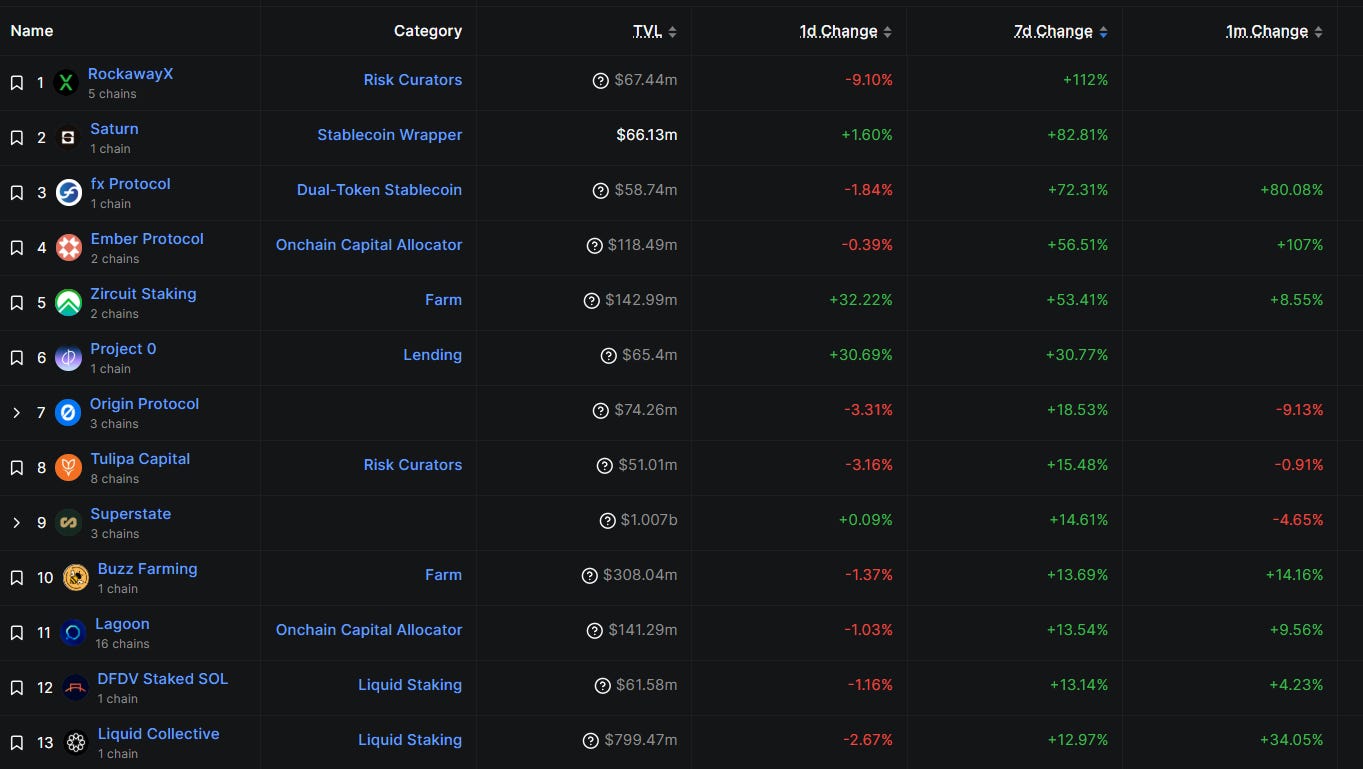

5. TVL gainers + Protocols Worth Farming

Ember Protocol — $118.49M TVL, +56.51% weekly (+107% monthly)

Ember doubled in 30 days, and this week’s catalysts explain why. Three product launches stacked on top of each other:

Ember ACRED launched on April 13. eACRED is onchain access to the ACRED private credit fund, with each eACRED backed 1:1 by underlying ACRED. Live on Ethereum and Sui, with integrations across Pendle.

Pendle integration for 3 Ember vaults (April 14). Fixed-rate exposure now available on:

eACRED — RWA private credit (10% average APY)

eEARN — opportunistic stablecoin strategies (6.% avg APY)

eTHIRD — Third Eye basis trade vault, delta-neutral, allocating to MON and ENA basis (5% avg APY)

This is the clearest “product-market fit in private credit” story in DeFi right now. Every integration (Pendle, NAVI, Symbiotic) compounds distribution. If RWA private credit continues to grow as a category — and $23.6B in tokenized RWAs says it is — Ember is positioned to capture a disproportionate share.

⚠️ Risk: Private credit has counterparty and duration risk that most DeFi users aren’t used to. Read the ACRED fund terms before depositing.

Superstate — $1.007B TVL, +14.61% weekly

Crossed $1B milestone this week as Superstate launched FundOS, an onchain fund infrastructure enabling asset managers to deploy mutual funds, ETFs, and private funds with real-time settlement, 24/7 flows, and DeFi integrations.

The TVL increase is pushed by institutional adoption for USCC, Superstate’s carry fund that maximizes yields across crypto cash-and-carry trades across the Bitcoin basis, Ether basis (including staking Ether), and U.S. Treasury securities.

Buzz Farming — $308.04M TVL, +13.69% weekly (+14.16% monthly)

Buzz Farming collaborates with well-known BTCFi projects such as Babylon, Lombard, and Bedrock, as well as prominent blockchains, offering users a variety of multifaceted profit strategies. Users can conveniently select and operate investment strategies through Buzz Farming. Pure Bitcoin deposits push the TVL increase into strategies, mainly airdrop farming on other third-party protocols mentioned above.

⚠️ Risk: Farm-category protocols often have TVL that’s highly tied to token emissions. If emissions slow, TVL can drop fast.

Smaller protocols Worth Farming:

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.