Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Headlines:

- Strategy raises $467M while holding Bitcoin steady

- Monaco brings institutional orderbooks to Sei

- RHEA launches private Hyperliquid trading on NEAR

- Jito commits JTX revenue to JTO buybacks and burns

Key Takeaways:

1. Liquidity is improving - but the war escalation adjusted rates concerns.

Net liquidity posted its biggest weekly expansion in months, and onchain flows turned positive across stablecoins, ETFs, and exchange reserves. Against that: Trump reinstated the Hormuz blockade, and oil and yields are climbing again. Real capital is entering crypto into a setup that just turned hostile.

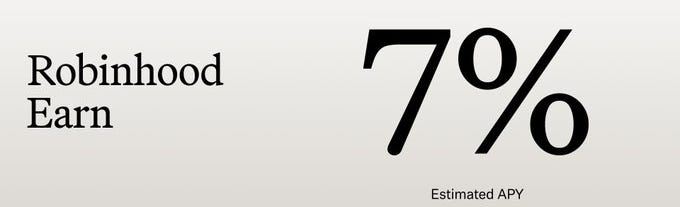

2. Robinhood Chain and Monad are where the yield is.

Robinhood Earn routes USDG deposits into curated Morpho vaults at around 7%, while Monad’s incentivized Aave launch is pushing stablecoin supply yields well into the double digits — subsidies leveraged farmers are already looping.

3. Uniswap benefited the most from Robinhood Chain’s traction.

Within a week of launch, it was doing more volume there than on any chain except Ethereum mainnet, with a governance change now in motion that could matter more than the launch numbers. Morpho is the quieter beneficiary — Robinhood Earn routes deposits straight into its vaults, and protocol fees more than doubled on the week.

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

1A. Traditional Macro

FRED:WALCL-(FRED:RRPONTSYD+FRED:WTREGEN)

Net liquidity: ~$5.98T, +$118.9B WoW (+2.03%). SUPPORTIVE. The largest weekly expansion in months, pushing liquidity back above its moving average. This is the strongest lever crypto has right now, and it explains why the tape held firm through a week of rising yields.

US 2Y yield

US 2Y yield: closed last week at ~4.21%, another grind higher — and it has already added +1.5% to 4.275% this week. TIGHTENING. Two main forces are pushing this: the June FOMC minutes showed officials increasingly concerned about inflation, with markets now pricing at least one hike by year-end, and the collapse of the Iran ceasefire has put oil back into the inflation equation. Rates are no longer consolidating; they are trending up.

Composite: DIVERGING, and rates are winning.

Liquidity expanded sharply while the front end tightened — the two levers pulling directly against each other. Liquidity carried the week, but the 2Y is now trending higher into a live geopolitical escalation, which makes it the dominant force going forward.

The blockade is back, and oil is repricing the war.

Trump reinstated the US blockade of Iranian ships transiting the Strait of Hormuz and demanded a 20% reimbursement on all cargo shipped through the waterway, declaring the US its “guardian” and posting that the strait “will remain OPEN, with or without Iran.”

Iranian vessels are blocked from entering or leaving; everyone else pays the toll. The White House has not explained how the fee would be administered or whether it was communicated to Gulf allies.

The market read it immediately: Brent has surged toward $85, after closing last week near $76.6 and bottoming around $72 in June. Oil spiking is the war signal, and it is the transmission channel into everything else — a toll on a fifth of the world’s seaborne oil is an inflation tax, whoever imposes it.

The critical difference from June: this disruption is US-imposed. Through late June the oil was flowing — CENTCOM escorted more than 800 vessels and 380 million barrels through the strait since early May, and prices had fallen back to pre-war levels. The blockade is what re-armed the supply risk, not an Iranian closure.

And Iran regards any challenge to its authority in the strait as a breach of the interim peace agreement, which raises the odds of renewed attacks on commercial vessels — the escalation loop that took Brent past $100 in the spring.

The contradiction to watch: they are still talking. The strikes, the blockade and the toll are happening alongside an active negotiation track. That is why oil is at $85 and not $110 — the market is pricing a bargaining tactic, not a collapse. It also means the tail is fat in both directions: a deal collapses this into a relief rally, a tanker attack takes it the other way. There is no stable middle.

1B. Crypto Capital On-Ramp

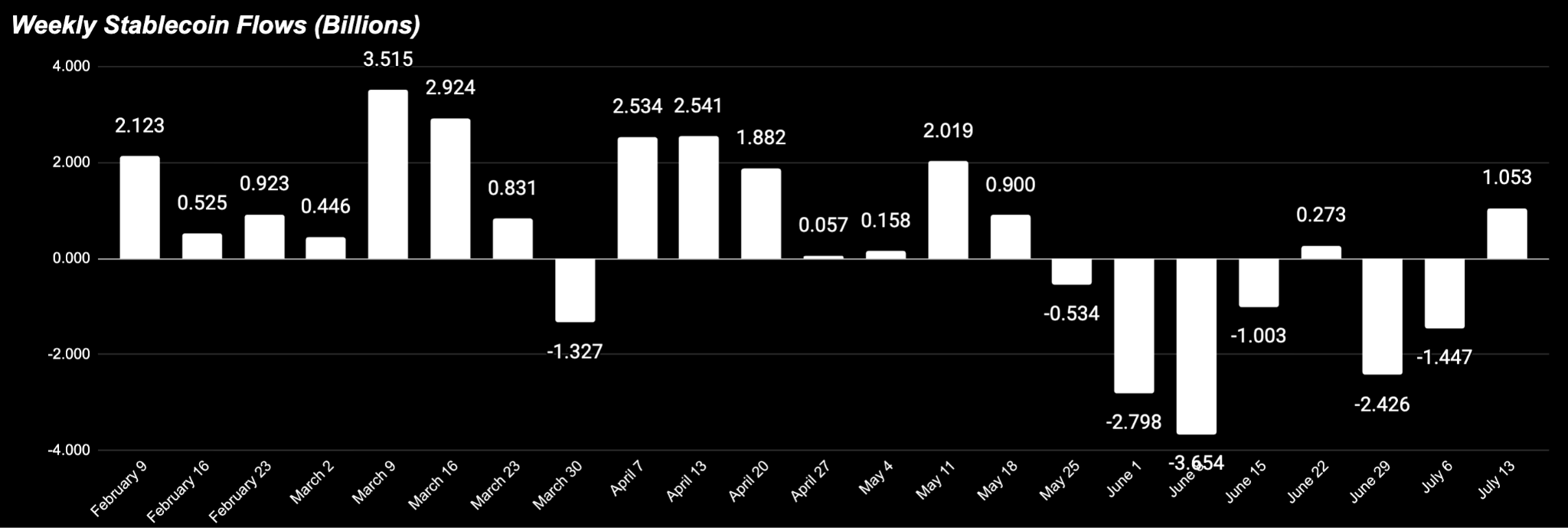

Total stablecoin supply 7d change (level + WoW)

Total stablecoin supply: $312.3B, +$1.05B WoW (+0.34%). EXPANDING — the first meaningful inflow since May. The base is growing again after five of the last six weeks of contraction. At +$1.05B this is the largest weekly inflow since May 11, and a decisive break from the June bleed (−$3.65B at its worst). Unlike last week’s rally — which we flagged as leverage-led, running on no fresh capital — new dollars are now actually entering the system. That’s the missing ingredient showing up.

BTC and ETH Exchange Flows (Net Reserve, NOT net flows per day)

Exchange flows — accumulation on both assets. Bitcoin reserves fell to ~2.711M and are now below the 21-day average, meaning coins left exchanges through the week even as price held around $62–64K.

Ethereum is the stronger signal: reserves dropped sharply from ~15.55M to ~15.40M, a steep decline, and it happened while ETH rallied to ~$1.78K. Price up plus reserves down is the textbook accumulation setup — buyers taking coins off exchanges into strength rather than selling into it. Both charts point the same way, and it’s the cleanest exchange-flow read we’ve had in weeks.

ETF flows

ETF flows — the streak broke and the bid returned. Inflows totaled $510M across three consecutive sessions in early July, ending the 10-day, $2.73B outflow run. July 6 alone drew $265.7M, with BlackRock’s IBIT taking $209.4M and Ethereum ETFs adding $20.7M. The composition matters — IBIT leading is the institutional signal, not retail dip-buying. Some analysts read it as capital rotating out of an overheated AI trade back into oversold crypto ETFs.

Onchain Regime read - Improving

For the first time in months, the three capital-ramp signals — stablecoin supply, exchange reserves, and ETF flows — are all pointing the same direction, and it’s up. This is the real story of the week: the macro backdrop deteriorated (rates up, dollar up, crypto lagging tech), yet the money actually moving into crypto turned positive.

1C. Week-Ahead Catalysts

June CPI — Tuesday, July 14. The single most important print on the calendar, and it lands tomorrow. ING expects headline prices to fall month-on-month on the plunge in gasoline prices, which could push markets toward pricing a long Fed pause rather than a hike this year.

But that forecast was written before oil jumped 5% this week — and the Fed’s focus is on wages, which accelerated to 3.5% year-on-year. A cool print revives the pause case; a hot one cements the hike.

Section 2 — Onchain Risk Regime

Individual Stablecoins Flows

The transactional giants turned positive — but only just, and only on 7d. USDC (+$365.5M) and USDT (+$25.2M) both posted weekly inflows, their first in weeks. But the 30-day picture shows how thin that turn is: USDT is still −$2.60B and USDC −$1.49B over 30 days. So this is week one of a reversal, not a trend. USDC did the real work; USDT’s +$25M is a rounding error on a $185B base. Treat it as stabilization, not re-acceleration.

BUIDL is the week’s story, and it’s a step change. BlackRock’s tokenized Treasury fund added +$640.9M in seven days — against +$663M over thirty. Effectively the entire monthly gain landed this week.

BUIDL is BlackRock’s USD Institutional Digital Liquidity Fund, issued by Securitize, backed by cash and short-term US Treasuries, paying daily dividends to holders. It is not a transactional dollar — investors must be verified by Securitize and buy with USDC.

Two distinct uses drive it: institutions parking idle cash onchain to earn Treasury yield, and — increasingly — posting it as trading collateral. BUIDL is accepted as collateral on Binance (off-exchange), Deribit, and Crypto.com, letting institutional traders margin leveraged positions while still earning yield on the asset. As Securitize’s CEO put it, the fund is evolving from a yield token into market infrastructure.

Aave / Sphere Rates

Funding ticked down from the top. The current funding benchmark sits at 5.90%, −0.23% on the week — the first decline after four straight weeks of climbing. But the level is what counts: at 5.90% versus a 4.28% borrow rate (supply 3.28%), funding remains well above borrow.

Leverage is still expensive and perps are still crowded long. The marginal cooling is healthy — froth easing rather than building — but the caution flag from last week stands. This is a market where longs are still paying up.

ETH/BTC Comparison Chart

ETHBTC closed +0.9% last week, the 2nd consecutive green weekly candle and a continuation of the strongest stretch of ETH outperformance against BTC in months. Right now, the candle is testing right at the 20-week moving average — the first time the ratio has reached that line since the downtrend began in the spring.

Verdict: Onchain regime — IMPROVING

With real capital behind it. Unlike last week’s leverage-only bounce, the flows are now genuine: supply expanded, USDC turned positive, BUIDL drew $640M, and reserves fell on both majors. The caveat is unchanged — funding still sits above borrow, and BUIDL’s inflow may itself be financing that leverage.

Section 3 — Chain Comparison

3A. Stablecoin flows by chain

The week's dominant theme was RWA tokenization, which surfaced across stablecoin flows, derivatives positioning, and protocol growth. The key catalyst was Securitize's July 2 NYSE listing, accompanied by the tokenization of roughly $295M of SECZ equity on Solana and Avalanche. At the same time, BlackRock's BUIDL expanded rapidly on Avalanche, helping drive one of the largest capital inflows of the week.

Stablecoin supply rose $1.14B (+0.37%) to $311.7B, while DeFi TVL remained largely flat at $73.6B. The largest flows were a roughly $2B USDT migration from Ethereum to Tron, but this was issuer-driven treasury management rather than organic demand.

Meanwhile, leveraged yield structures continued to contract. Ethena USDe (-$488M), the Sky/Spark ecosystem (~-$1.05B combined), and MegaETH (-$496M stablecoins) all saw significant outflows, suggesting capital continues rotating out of incentive-driven yield strategies and into institutional products.

Monad: +$40.3M (+8.3%) — an incentivized Aave V3 launch converting subsidies into a stablecoin-looping venue.

The inflow is modest relative to the catalyst behind it. Aave launched V3.7 on Monad on July 2 and surpassed $100M in deposits within 48 hours, backed by a major incentive package: $15M in Monad liquidity incentives, a 10M GHO commitment from the Monad Foundation, and 500K GHO from Aave DAO.

The opportunity is clear. Merkl rewards currently boost supply yields to roughly 14.4% on USDC, 6.7% on USDT0, 8.1% on AUSD, and 7.3% on GHO, creating borrowing costs below comparable Ethereum and L2 markets. This has attracted leveraged farmers using assets such as syrupUSDC and sUSDe as collateral, borrowing subsidized stablecoins and looping positions to capture both collateral yield and WMON emissions.

Tron & Ethereum: ~$2B USDT Reallocation

Tron gained $2.3B while Ethereum lost $2.1B, largely due to a coordinated Tether treasury operation. Tether burned roughly $2.5B USDT on Ethereum and later minted $1B on Tron, shifting supply toward its preferred payments rail.

For traders, the more important signal is that Ethereum USDC still grew by $361M, suggesting this was a stablecoin composition shift rather than capital leaving Ethereum altogether. The trend modestly strengthens Tron’s settlement dominance while slightly reducing Ethereum’s USDT collateral base.

Spotlight · Robinhood Chain

The constructive case is early participation in a distribution-rich, regulated-brand ecosystem: alarge existing customer base, tokenized equities across more than 120 markets, established protocols already deployed, and a yield structure combining USDG rewards, Ethena-linked returns, and Lighter points, with a potential future token as optionality.

The offsetting risks are specific: headline metrics are incentive-inflated; the airdrop thesis is unconfirmed; the network operates on a single Robinhood-run sequencer; and stock tokens are unavailable in the United States, the company’s home market.

The relevant precedent appears in Section 3: MegaETH’s stablecoin base contracted by approximately 80% this week — roughly two months after its token generation event — when leveraged liquidity routed through Aave withdrew.

Robinhood Chain’s $294.6M of stablecoins resting above $161M of deployed TVL has a comparable bootstrap profile. The appropriate framing is incentive-dependent early positioning with a defined view on the token and incentive timeline, rather than a durable allocation.

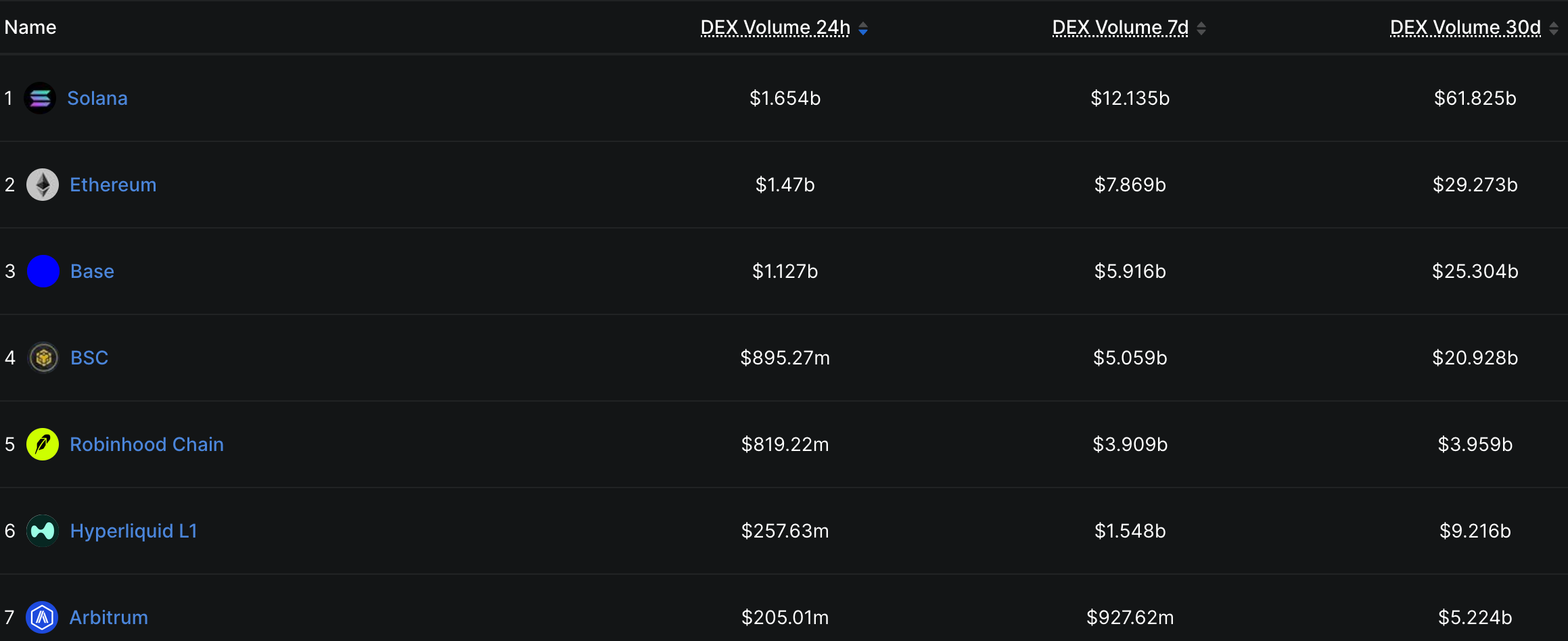

3B. Structural Shifts- DEX Volumes

Robinhood Chain remains the week's dominant launch venue.

On the yield side, Robinhood Earn routes USDG deposits into Steakhouse-curated Morpho vaults with projected yields around 7%, positioning Morpho as a core piece of the chain's financial stack. Morpho Blue's fees rose 143.8% WoW to $11.4M, reinforcing the shift toward curated-vault lending models even as Aave tightened risk parameters through supply- and borrow-cap reductions.

Trading activity tells the same story. Robinhood Wallet users can earn 2x Lighter points against an 11M LIT allocation, creating a direct incentive to trade on-chain. Speculative attention remains concentrated in Robinhood Chain memecoins, led by CASHDOG and CASHCAT, though the chain's elevated volume-to-liquidity ratio highlights the risks of chasing launch-phase momentum.

The venue impact is already visible in DEX flows. Uniswap V3 volume rose 79% WoW and V2 volume jumped 1,003%, with Robinhood Chain accounting for the majority of V2 activity and more than half of V3's volume. More important than launch-week volume, however, is governance: on July 8, Uniswap advanced a proposal to extend the UNIfication buyback-and-burn mechanism to V4 pools, a development worth tracking as fee generation increasingly shifts toward newer deployments.

RWA Derivatives: Positioning Is Catching Up To The Narrative

The strongest conviction trade this week was RWA-linked derivatives. Ostium’s open interest climbed 73.8% WoW to $285.5M, alongside 31.1% TVL growth, while Ondo Perps added 42.6% to reach $26M in open interest.

What’s notable is that this growth aligns with the broader tokenization story discussed elsewhere in the report. Product issuance, capital inflows, and trader positioning are all moving in the same direction. Rather than RWA enthusiasm being confined to treasury funds, traders are increasingly expressing that view through leveraged products.

Perpetuals activity overall remains concentrated on Hyperliquid, which continues to host roughly $15B of open interest across Hyperliquid Perps and tradeXYZ, despite softer fee generation during the week.

Section 4 — Project & Protocol Discovery

4A. Token Price Movers - Observations, not trade ideas.

edgeX — EDGE, +29% (7d). A cluster of product news: a restructuring adding engineering, risk, and product hires; a roadmap toward RWA trading pairs and leveraged ETFs, and a native USDC deposit campaign paying 4% APR in USDC plus 3% in EDGE. Incentive-led as much as fundamental.

Lido — LDO, +10% (7d). wstETH is now live on Robinhood Chain via Chainlink CCIP, carrying its Ethereum staking rewards across, with direct staking and deeper integrations flagged as next. Distribution into Robinhood’s retail base.

Uniswap — UNI, +13% (7d). The clearest read on Robinhood Chain’s traction: Uniswap crossed $250M+ in protocol volume there within a week of launch, then did $500M in a single day — 10x the prior day, and more than any chain except Ethereum mainnet. Uniswap TVL on the chain passed $30M. Separately, Uniswap now routes through Sky’s LitePSM, clearing DAI/USDS/USDC legs at parity.

4B. TVL Gainers Ranked by absolute $ inflow.

The Securitize complex: +$776.0M aggregate — the week’s defining growth event.

BlackRock’s BUIDL (+$640.9M, +21.0%, to $3.69B) and VanEck’s VBILL (+$135.1M, +238.4%, to $191.7M) are both issued via Securitize, and their combined weekly gain constitutes the largest capital formation in DeFi this week; Securitize’s other listed funds (Apollo credit, tokenized CLO) were flat, so the aggregate is attributable to these two products.

Because both are money-market funds redeemable at approximately $1 NAV, the entire gain is net-new subscription capital with no price component — the highest-quality growth on the board, corroborated by fee income (BUIDL +108% week-over-week; VBILL +137%).

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.