US-Iran Deal Lifts Risk Sentiment, Ethena & Ether.fi's Genuine TVL Increase - Onchain Outlook

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Today’s News Headlines:

- Ventuals shuts down after doing $650m volume

- InfiniFi boosts siUSD Pendle rewards

- Saturn launches Morpho USDC vault

- Tangent enables sUSG collateral looping

- Ondo Perps lists SpaceX contracts

- Thetanuts exploited for ~$2m, attacker offers whitehat fund return

$25,000 USDC Up for Grabs — DeFi Saver Season 1 Is Live

DeFi Saver just launched its first-ever rewards campaign, and the prize pool is real. Trade Hyperliquid perps or run Boosts and Repays on Aave, Spark, Morpho, and more. Your score combines volume with profitability, so good traders win, not just big ones. Season 1 runs until June 22nd. Top spot takes 7,500 USDC.

<Join Season 1 on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

Key Takeaways:

1. Risk on regime is slowly improving

The Iran-US framework deal (signed digitally on June 14) knocked oil down 6% to below $80, dropped short-term rates, and the dollar and crypto vs. equities were favorable in the same week. Still improving rather than risk-on: stablecoin and ETF outflows are shrinking but haven’t turned positive, and Wednesday’s FOMC + Friday’s signing are the confirmation points.

2. This week’s inflows came from institutional rails.

The capital that moved chose tokenized assets, yield, and settlement infrastructure over speculation, concentrating on X-Layer, Aptos, and Solana. Solana was the highlight: rising as a stablecoin settlement venue, with tokenized-equity volume growing while the broader market pulled back.

3. Ethena and ether.fi led on real flow.

The cleanest project signals were genuine capital, not price. Ether.fi’s TVL gain was 75% real inflow, and both pushed into tokenized credit. Two of DeFi’s biggest names are converging on the same trade.

Section 1 — Macro + Capital Backdrop

1A. Traditional Macro

DXY: 99.52, weekly down candle (-0.29%).

The dollar printed a down week driven by reduced safe-haven demand as the Iran deal firmed up — when geopolitical risk fades, the dollar safety bid unwinds. A softer dollar removes a background headwind for crypto.

BTC/NQ ratio: first green weekly candle after 6 weeks of red.

Crypto outperformed the Nasdaq last week for the first time since the underperformance regime began. One green candle isn’t a trend reversal, but after six consecutive red weeks, it’s the first sign of relief in the BTC-vs-equities rotation.

The macro picture turned this week, and the driver is one story: the Iran-US deal.

After more than three months of conflict that closed the Strait of Hormuz, the two sides digitally signed the framework deal agreement on June 14, with a formal memorandum of understanding set to be signed in Switzerland on Friday, June 19. The deal ends the fighting, reopens the Strait, and commits Iran to abstain from producing nuclear weapons.

The Strait carries roughly a fifth of the world’s oil and LNG supply — its closure was the single biggest macro overhang of the past quarter, driving oil up, inflation expectations higher, and the Fed into a hawkish hold since March. Its resolution unwinds that chain.

Oil fell hard — Brent dropped 6% to below $80 and WTI to $79, both the lowest since March 10. Lower oil cools the inflation picture that has kept rates elevated, which is why this single geopolitical event is rippling through every macro indicator above.

Composite read: risk-on building, with Friday's signing as confirmation.

1B. Crypto Capital On-Ramp

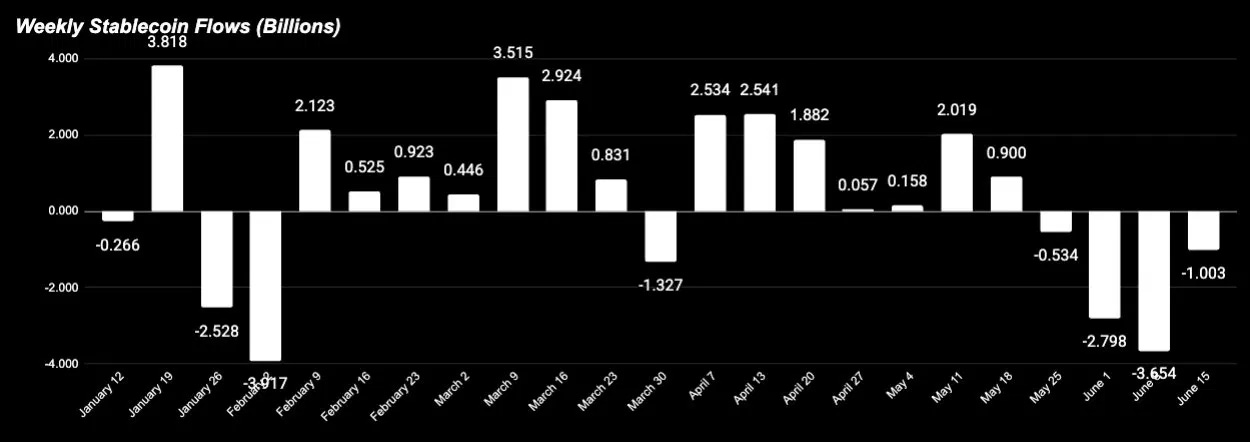

Total stablecoin supply 7d change (level + WoW)

Total stablecoin supply: -$1.0B (-0.3%). Still net negative, but a major improvement from last week’s -$3.6B drawdown. The outflow is shrinking fast — a -0.3% weekly move is minor, and the trajectory (from -$3.6B to -$1.0B) suggests the bleed is decelerating rather than accelerating.

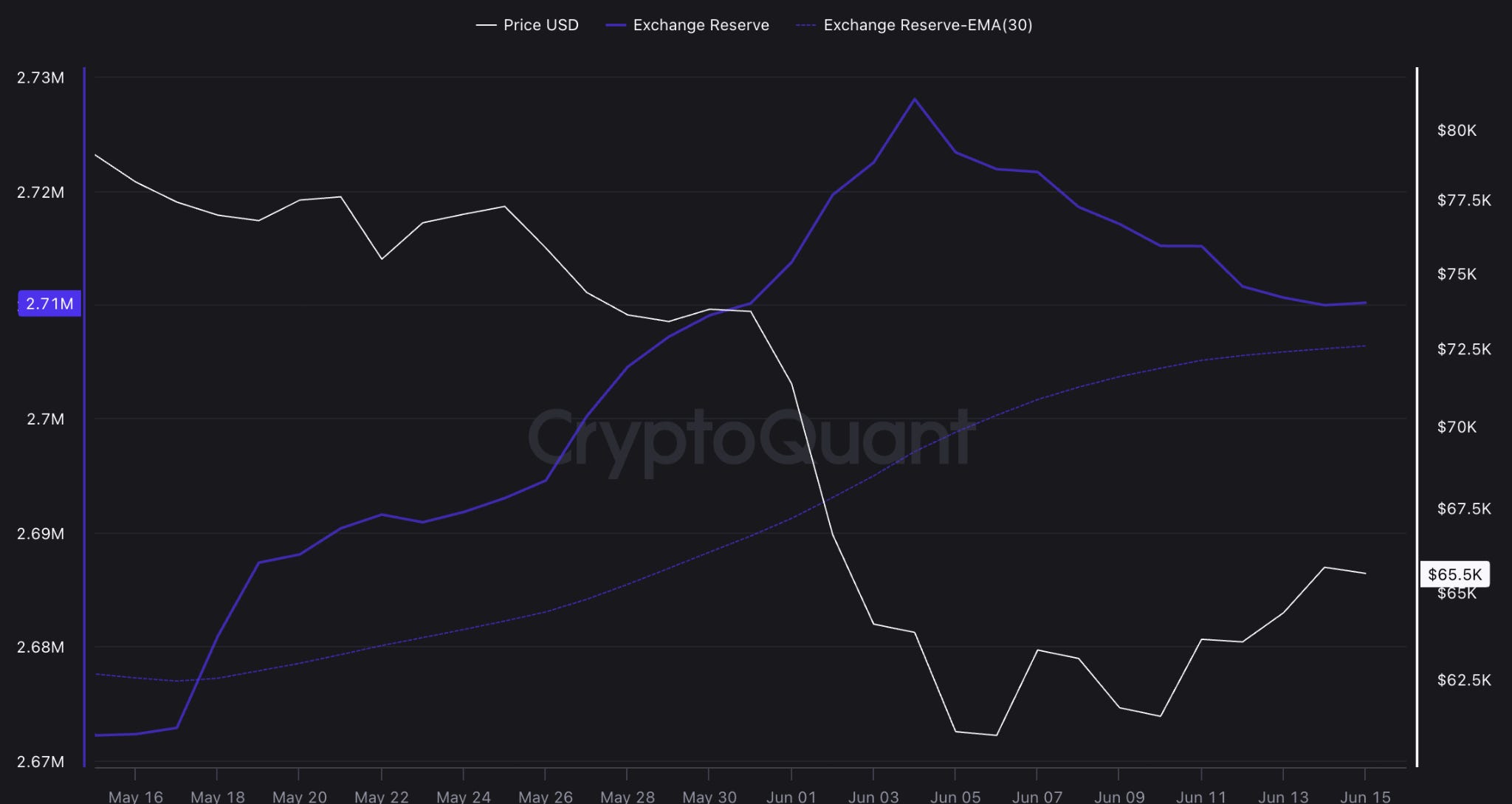

Exchange flows — Bitcoin back to accumulation.

Since the dip towards $58, more Bitcoin has been moving off exchanges than onto them - a sign of potential accumulation.

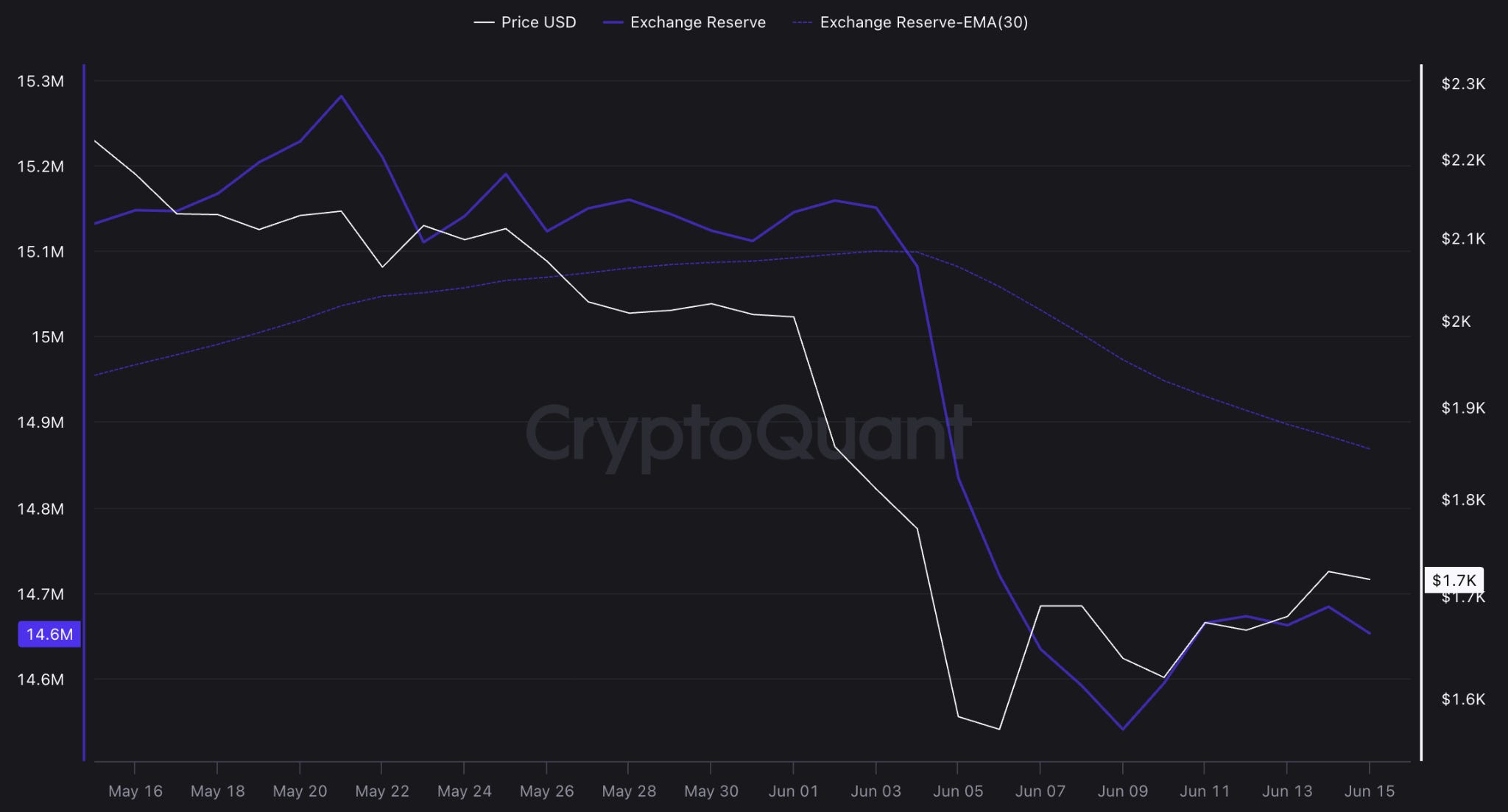

Ethereum weekly flows were opposite of Bitcoin, with coins coming onto exchanges even as the price rose. Notably, even with the inflows, Ethereum exchange reserves are near yearly lows.

ETF flows

ETF flows: relief in the trend. Last week still saw net outflows, but the magnitude eased after a month of week-on-week acceleration. The outflows are getting smaller — the first sign the institutional selling pressure may be exhausting.

1C. Week-Ahead Catalysts

FOMC meeting, June 16-17

Kevin Warsh’s first as Fed Chair. A near-certain hold at 3.50-3.75% (CME FedWatch ~98%). The rate decision isn’t the story — Warsh’s first press conference tone and the updated dot plot are.

Strategists expect an explicit move away from the easing bias toward a neutral stance. Warsh has signaled a preference for a leaner Fed that communicates less, so markets will be parsing the shift in style as much as the substance.

US–Iran peace deal signing (June 19)

The two sides finalized the agreement framework on June 14, with the formal signing ceremony scheduled in Switzerland on Friday.

Markets will be watching for details on ceasefire implementation, Strait of Hormuz access, and the next phase of nuclear negotiations.

Source: tradingeconomics.com

Section 2 — Onchain Risk Regime

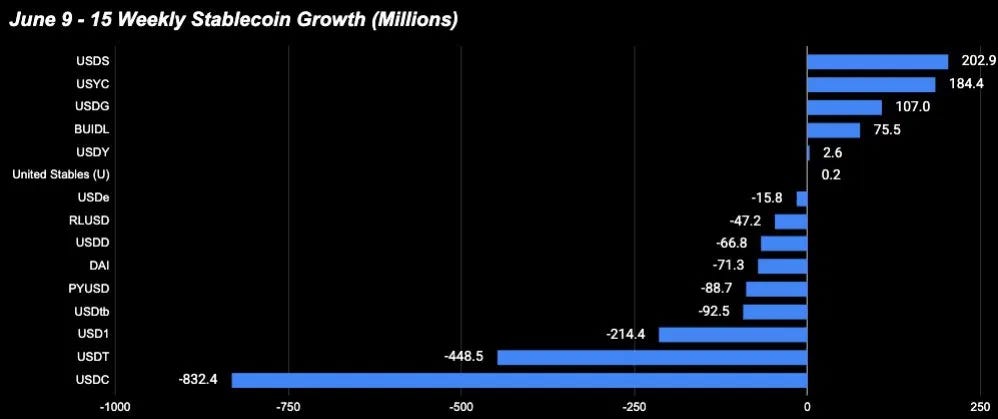

Individual Stablecoins Flows:

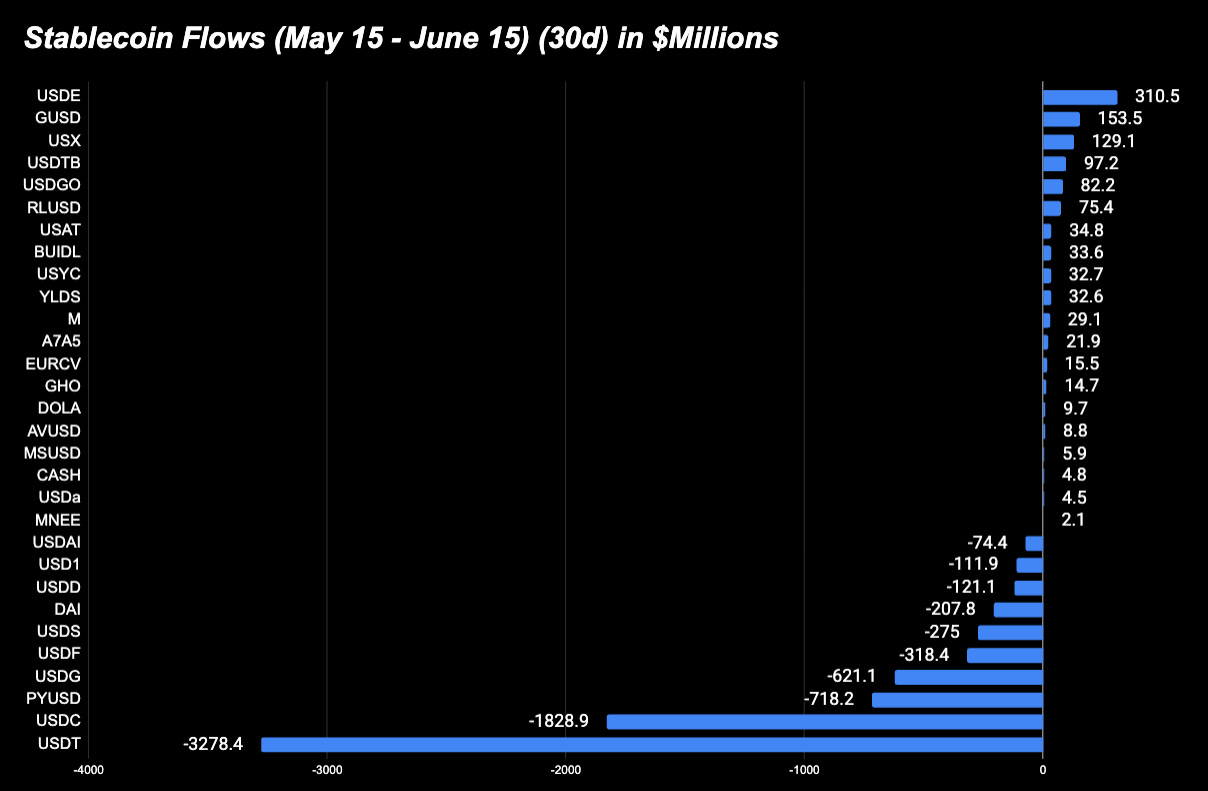

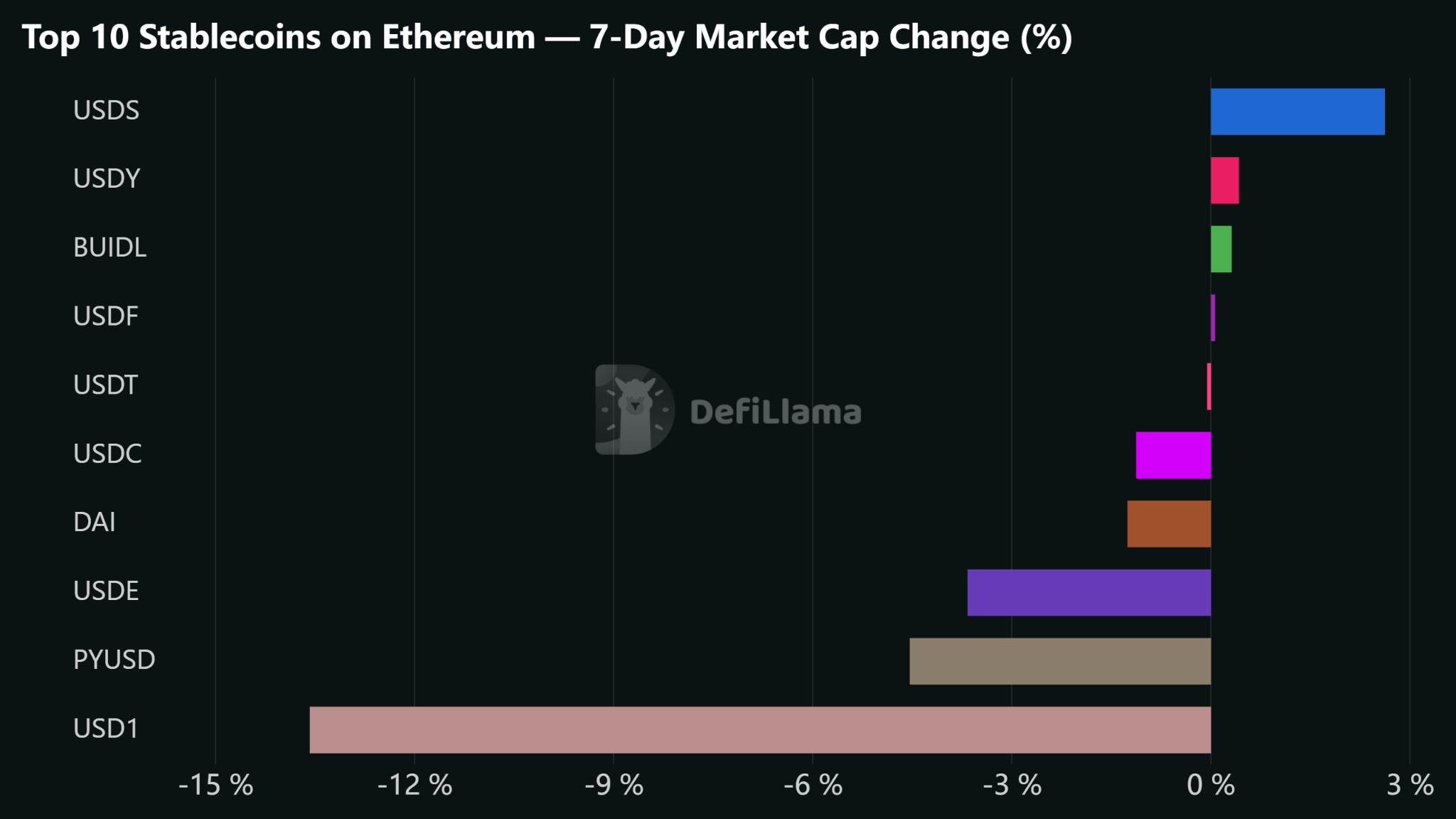

The total stablecoin supply fell -$1.0B this week, capital is continuously rotating out of transactional dollars (USDC, USDT) and into yield-bearing and tokenized Treasury dollars. This shows that capital is leaving crypto, with the retaining capital changing what kind of dollar it holds.

Every meaningful gainer is a yield or RWA product; the biggest losers are the two transactional giants USDT and USDC. The 30-day data confirms this is structural, not a one-week artifact: USDC has bled -$1.83B and USDT -$3.28B over the month, while the yield/RWA tier (USDe +$310M, USDtb +$97M, RLUSD +$75M, plus tokenized-Treasury names) consistently absorbs. The transactional dollars that sit idle for trading are shrinking; the dollars that earn yield are growing.

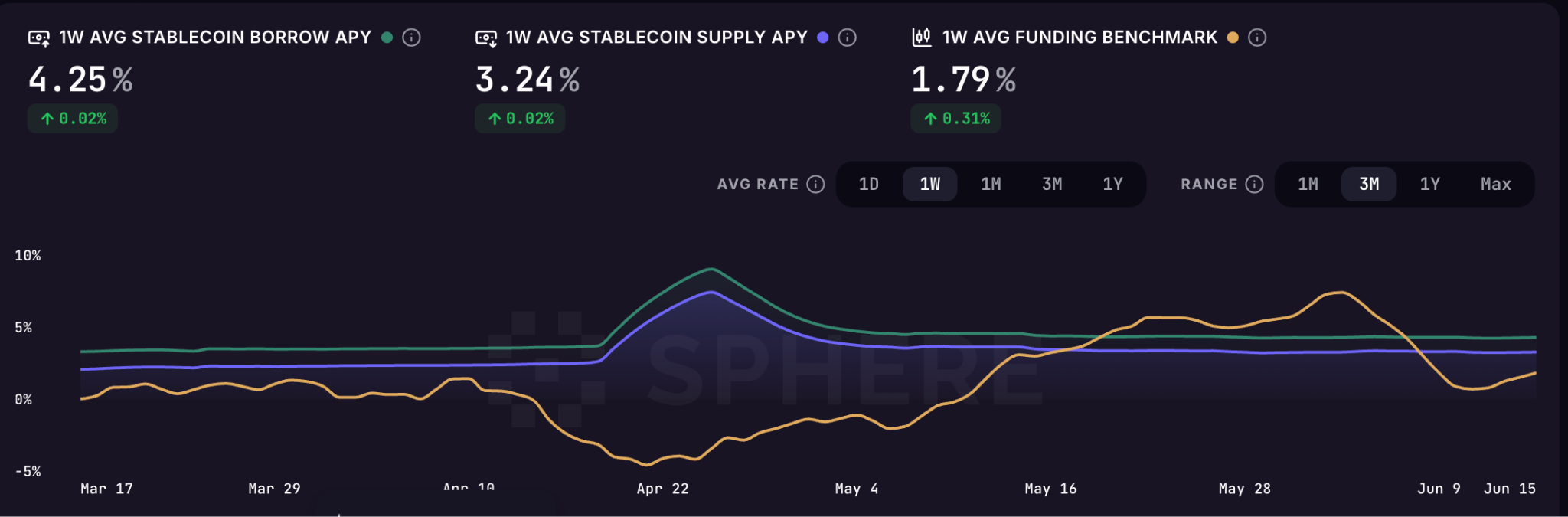

Aave / Sphere Rates

Calm, funding slightly rising.

Borrow APY 4.25% and supply APY 3.24%, both essentially flat WoW (+0.02%). The funding benchmark rose to 1.73% (+0.25%) — the biggest mover of the three — but still sits well below the 4.25% borrow rate. Funding far below borrow signals leverage demand is still subdued: perps aren’t crowded long, and there’s no greed in the system yet. Funding ticking up off the lows fits the risk-on-building macro read, but it’s early — leverage hasn’t returned. Consistent with stabilizing, not euphoric.

ETH/BTC Comparison

ETH/BTC recorded another red week. The new weekly is green, showing potential strength against BTC, although it’s too early to be confirmed.

Section 3 — Chain Comparison

3A. Stablecoin flows by chain

This week tested the stablecoin market’s maturity — and on most measures, it passed. In prior risk-off periods, stablecoin supply contracted sharply as participants converted to fiat.

That pattern did not repeat. Instead, capital bypassed exchanges, where monthly inflows fell to $2.9 billion from a peak of $5.7 billion, and rotated into on-chain yield products, tokenized assets, and institutional settlement infrastructure. The market is now deeper, more diversified, and more structurally entrenched than during previous drawdowns.

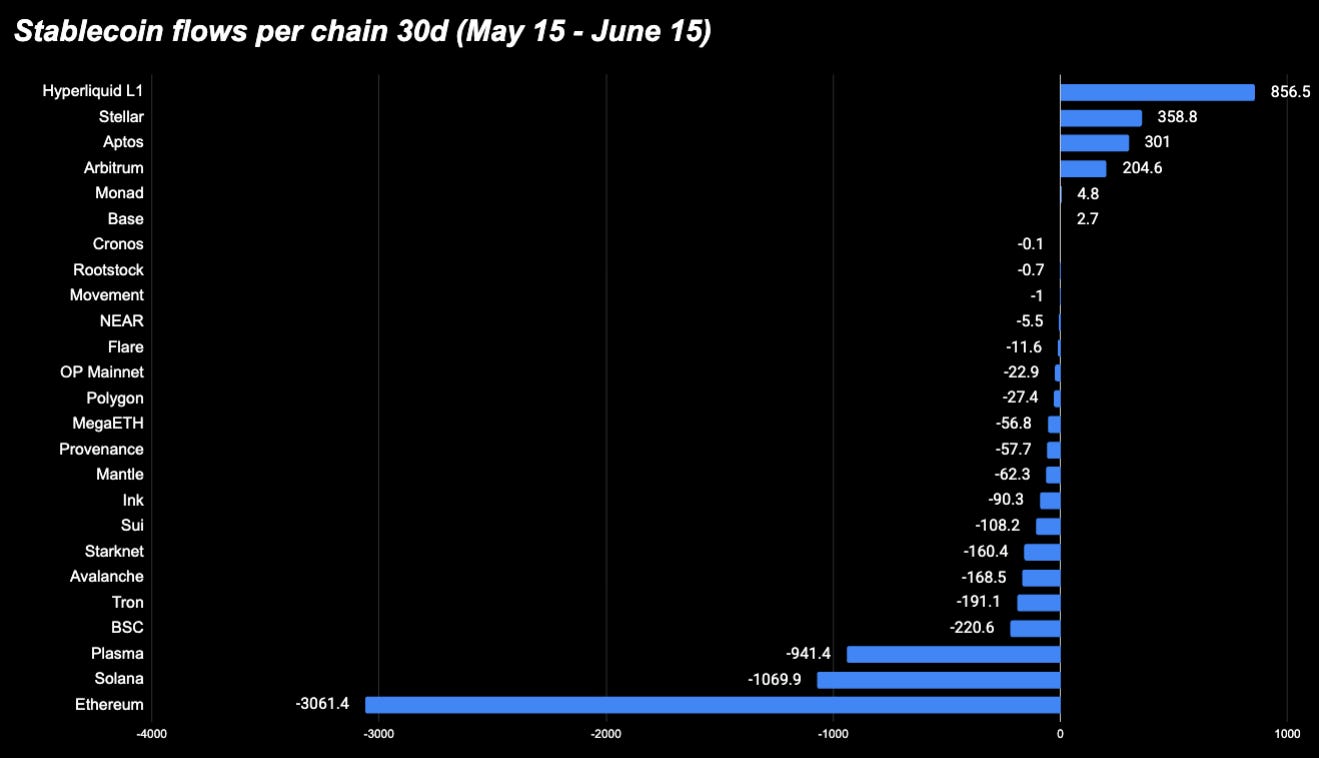

Most of the Capital Is Rotating, Not Leaving

The week’s central theme is redistribution, not contraction. Ethereum lost $1.09 billion in stablecoin supply over seven days, and Tron lost $515 million — together accounting for the bulk of all outflows.

However, most of it is redistributed to chains offering something Ethereum and Tron currently lack: yield opportunities, institutional infrastructure, or active new deployment venues.

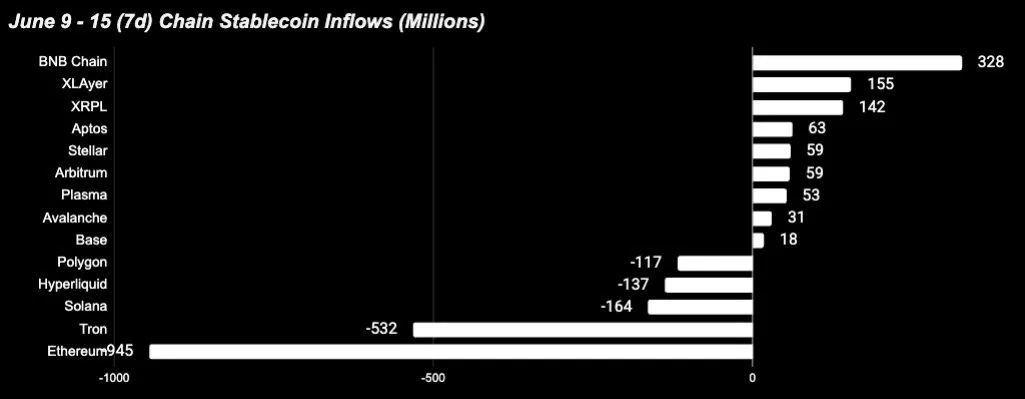

Where it went:

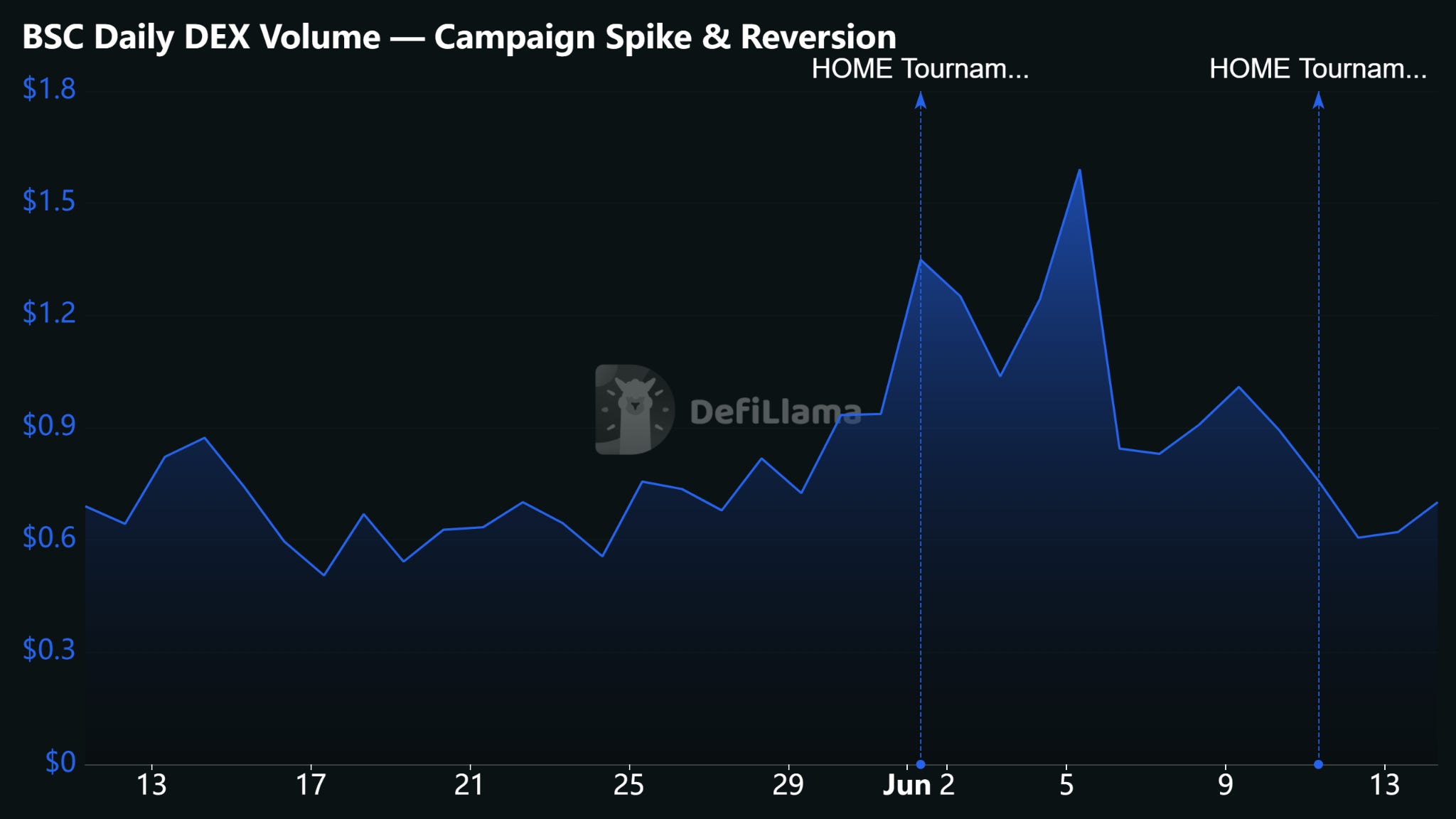

BSC took in the most in absolute terms, roughly $486M, but the composition matters more than the headline.

Last week’s BSC inflows were campaign-driven DEX volume, but this week, those incentives expired, and USDT went flat.

The growth came from somewhere healthier: USDC added about $300M as Circle reallocated supply to the chain, and USYC — Hashnote’s tokenized Treasury product — added $155M to become the second-largest dollar on BSC after USDT. That’s asset managers parking short-duration yield onchain, not traders staging capital.

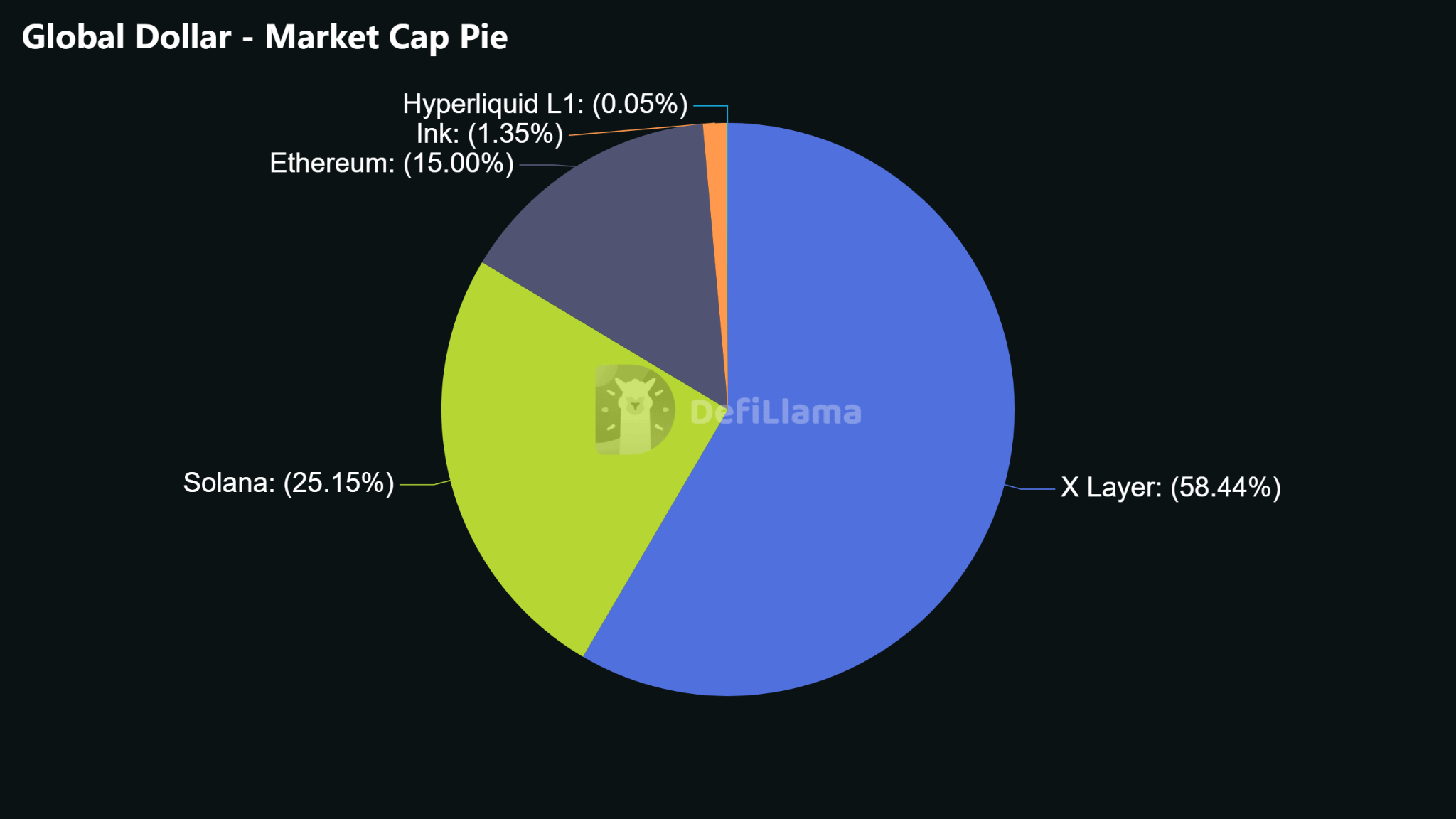

X-Layer posted the strongest percentage gain of any major chain at +10.5%.

Almost all of it traced to a single instrument: Global Dollar (USDG), up $153.7M. X-Layer now holds roughly fourteen times more USDG than USDT, which tells you what it’s becoming — an institutional settlement layer anchored by one stablecoin, reinforced by OKX’s rollout of Exchange OS and its yield-bearing OKUSD.

The flip side is concentration risk: a chain that depends this heavily on one issuer is exposed if that issuer’s supply moves elsewhere. Worth watching.

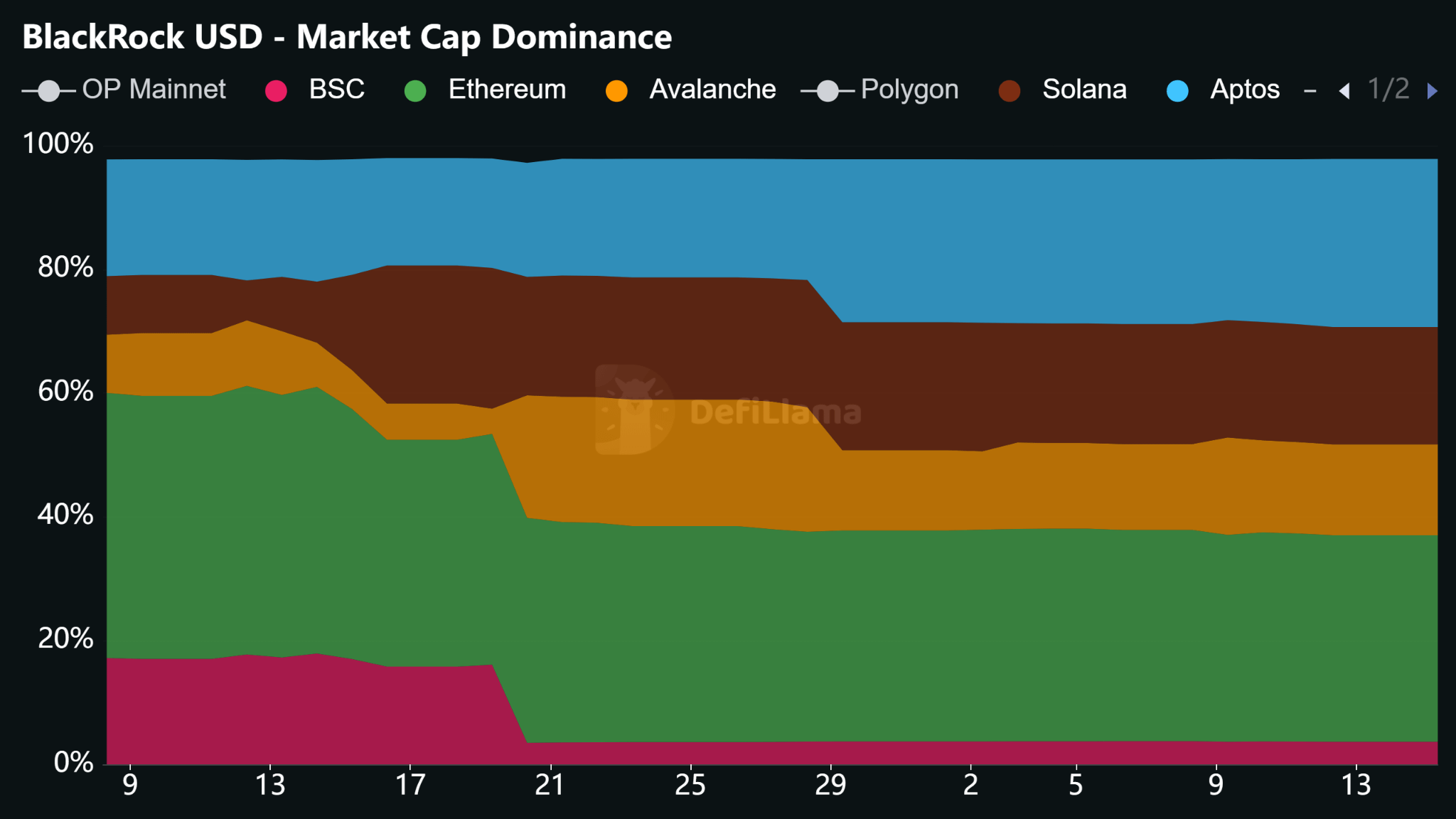

Aptos is the one we’d flag for structural quality

Growth was broad rather than tied to a single product. BlackRock’s BUIDL is up 47% over 30 days, USDC grew 27% on the week, and even USDT added supply — all at once.

When a regulated money market fund, the leading institutional stablecoin, and the dominant permissionless dollar all expand together, that’s the chain itself being validated, not one issuer’s distribution push.

Where it came from:

On the other side, Ethereum shed about $1.09B across six different stablecoins. The scale could look alarming, but it reflects Ethereum’s role as the system’s issuance and bridging anchor — capital minted there moves downstream to wherever it gets deployed. This is secular and directional, not a sign of stress.

Tron lost $515M, almost entirely USDT, as new Tether issuance increasingly lands on Solana and BSC instead. Slow erosion, not a break.

This week’s fastest-growing dollars weren’t USDC or USDT at all; they were tokenized-yield instruments like USYC and BUIDL, now clearly their own institutional growth category.

Three Signals Worth Watching

Institutional yield stablecoins are now a distinct growth category. This week’s highest-growth instruments weren’t USDC or USDT — they were tokenized yield products. USYC and BUIDL together added over $230 million across BSC, Aptos, and Avalanche during a risk-off week in which speculative assets declined. Backed by U.S. Treasury yield, these instruments are structurally preferable to idle USDC for institutions without immediate deployment needs.

Their growth is driven by yield demand rather than risk appetite — a durable, structural dynamic.

USDG’s concentration on X-Layer warrants monitoring. X-Layer holds $1.51 billion in USDG against just $107 million in USDT — a 14:1 ratio that makes X-Layer’s stablecoin ecosystem almost entirely dependent on a single issuer.

If this reflects a strategic partnership, it’s a feature. But if USDG redistributes elsewhere, the concentration creates meaningful supply-event risk for the chain’s liquidity depth.

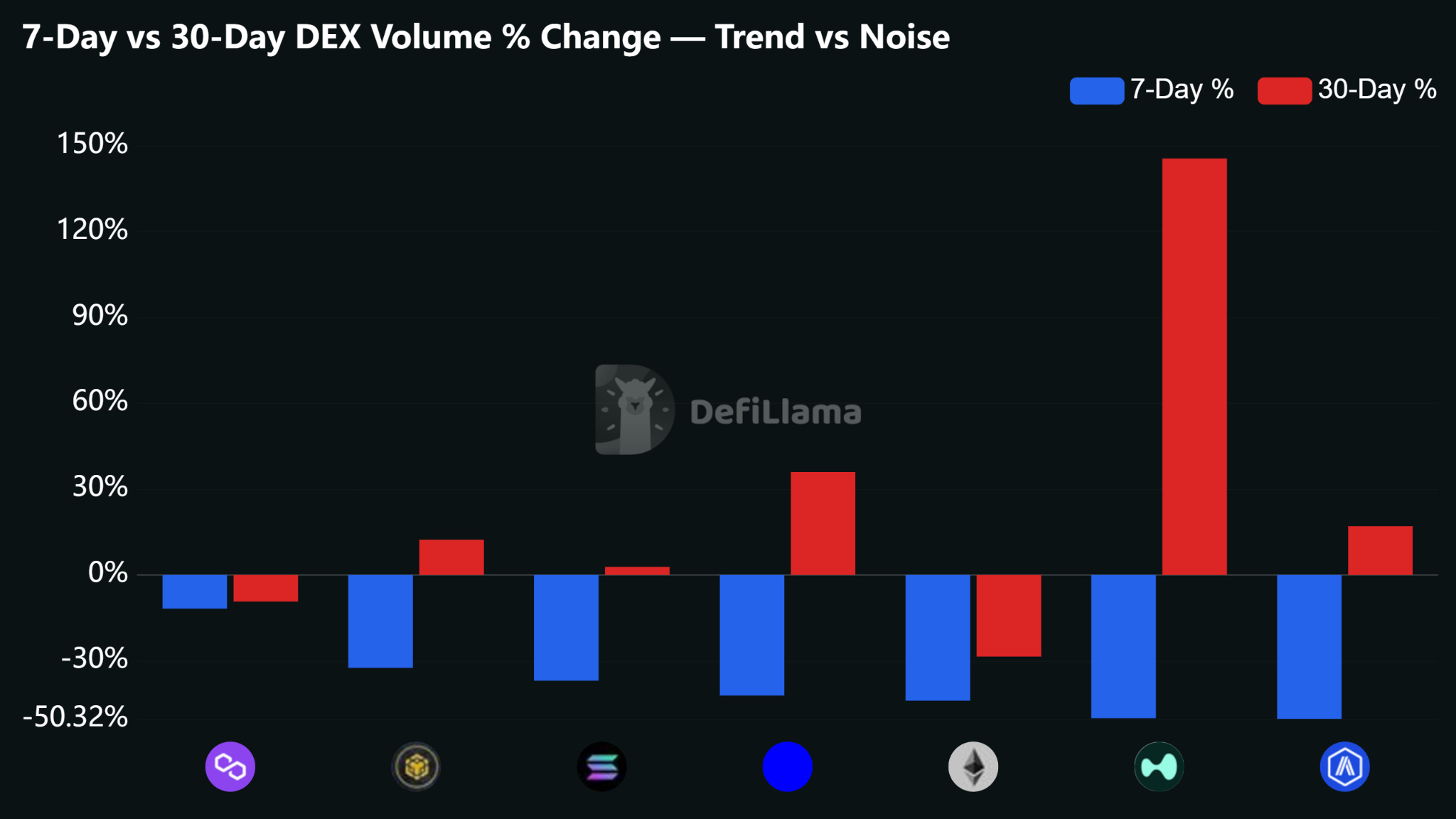

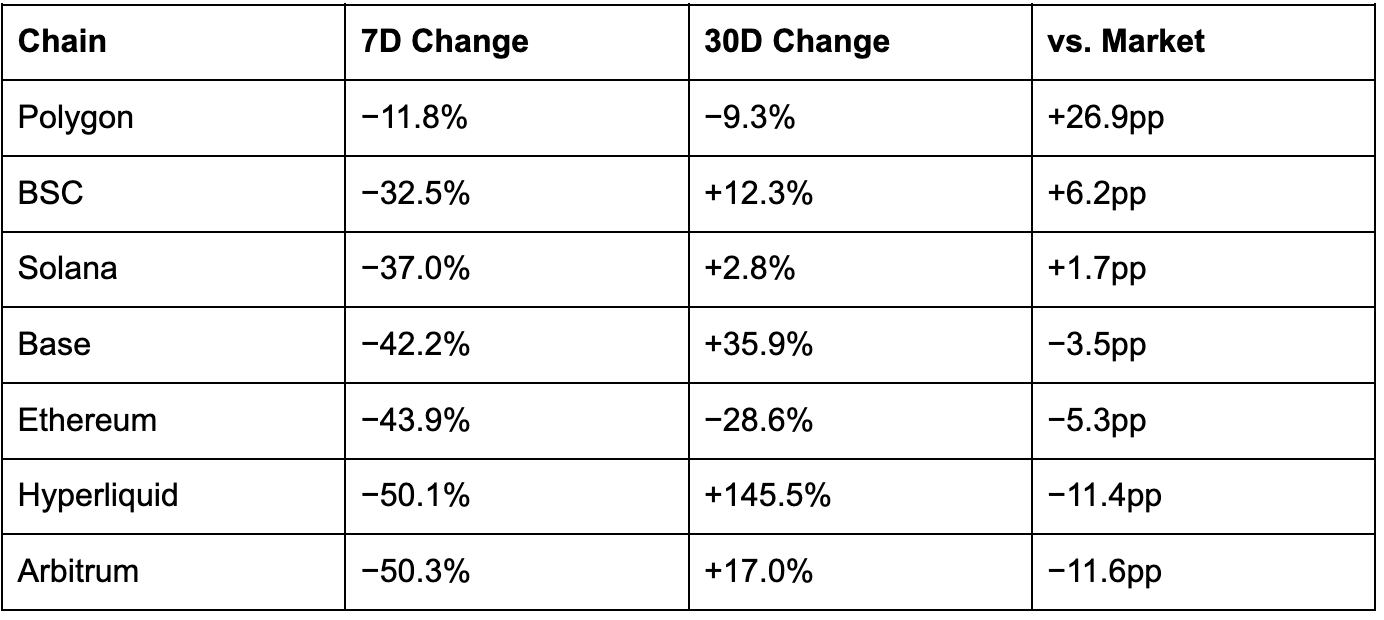

3B. Structural Shifts Based on DEX Volume

This was a broad pullback — every onchain DEX chain contracted week-over-week — but the gap between the best and worst performer was nearly 38 percentage points. Read down the 30-day column, and the chains separate cleanly into ones building durable volume and ones still riding speculation. The spread is about what each chain is becoming, not its architecture.

Solana quietly turning into the home for tokenized real-world assets

Its weekly drop tracked the market, but that masks a rotation happening underneath: the memecoin-driven volume that long defined the chain is deflating, while two higher-quality layers grow into the gap. One is institutional stablecoin settlement, where Manifest expanded 19% over 30 days straight through the downturn.

The other is tokenized real-world assets — and here Solana is genuinely ahead of every other chain. A tokenized S&P 500 product (SPYX) is the second-largest pair on Orca at ~23% of its volume, and a tokenized SpaceX pre-IPO token trades on Meteora.

No other chain in the dataset has a single tokenized equity in its top pairs. Solana is slowly trading speculative volume for settlement and RWA volume — lower-octane, but far more durable.

BSC held up better than the market on 30 days

Because it runs on two layers: a blue-chip, BNB-centric routing floor that barely moves with sentiment, sitting under a speculative launch layer that resets with each Binance product cycle. This week the speculative layer cooled as campaigns expired, but the floor held — which is why BSC compressed less than chains that are all speculation.

Section 4 — Project & Protocol Discovery

4A. Token Price Movers - Observations, not trade ideas.

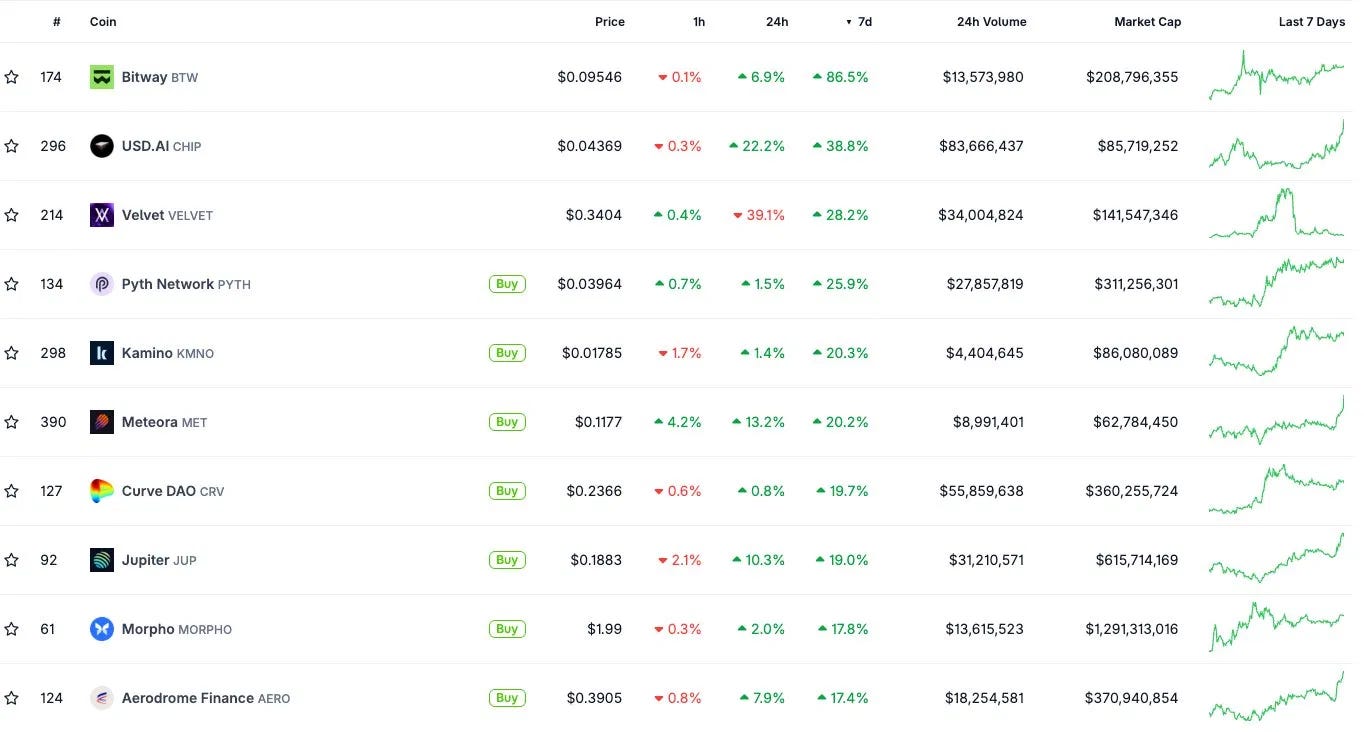

USD.AI — CHIP, +38.8% (7d). Published its 2026 YTD report, Lighthouse: $44.6M protocol ARR, a $13B borrower pipeline, $205M closed and funded, and 7.0% average sUSDai yield YTD. The protocol underwrites GPU-backed loans. report

Pyth Network — PYTH, +25.9% (7d). Launched Pyth Indices — 24/7 indices across U.S. equities, oil, metals, and thematic baskets, co-developed with MarketVector (a VanEck company). Already live on Coinbase, Kraken, dYdX, and Nado.

Kamino — KMNO, +20.3% (7d). Listed tokenized SpaceX shares ($SPCX, issued by Backpack Securities, redeemable 1:1) for 24/7 trading on Kamino Swap following SpaceX’s Nasdaq debut. Also placed #9 in DeFi on Fortune’s Crypto 100.

Curve DAO — CRV, +19.7% (7d). Announced Llamalend v2: lending markets open beyond crvUSD, Curve LP tokens usable as collateral, isolated per-market risk, range-based liquidations via LLAMMA. Launching first on Optimism. post

Morpho — MORPHO, +17.8% (7d). Raised $175M co-led by Paradigm, a16z crypto, and Ribbit Capital — the largest raise in DeFi history — with participation from Apollo, VanEck, and Circle Ventures.

Aerodrome — AERO, +17.4% (7d). Will launch Predictive Allocation in July, shifting incentive allocation from past performance to rewarding participants who correctly anticipate where liquidity demand goes next. source

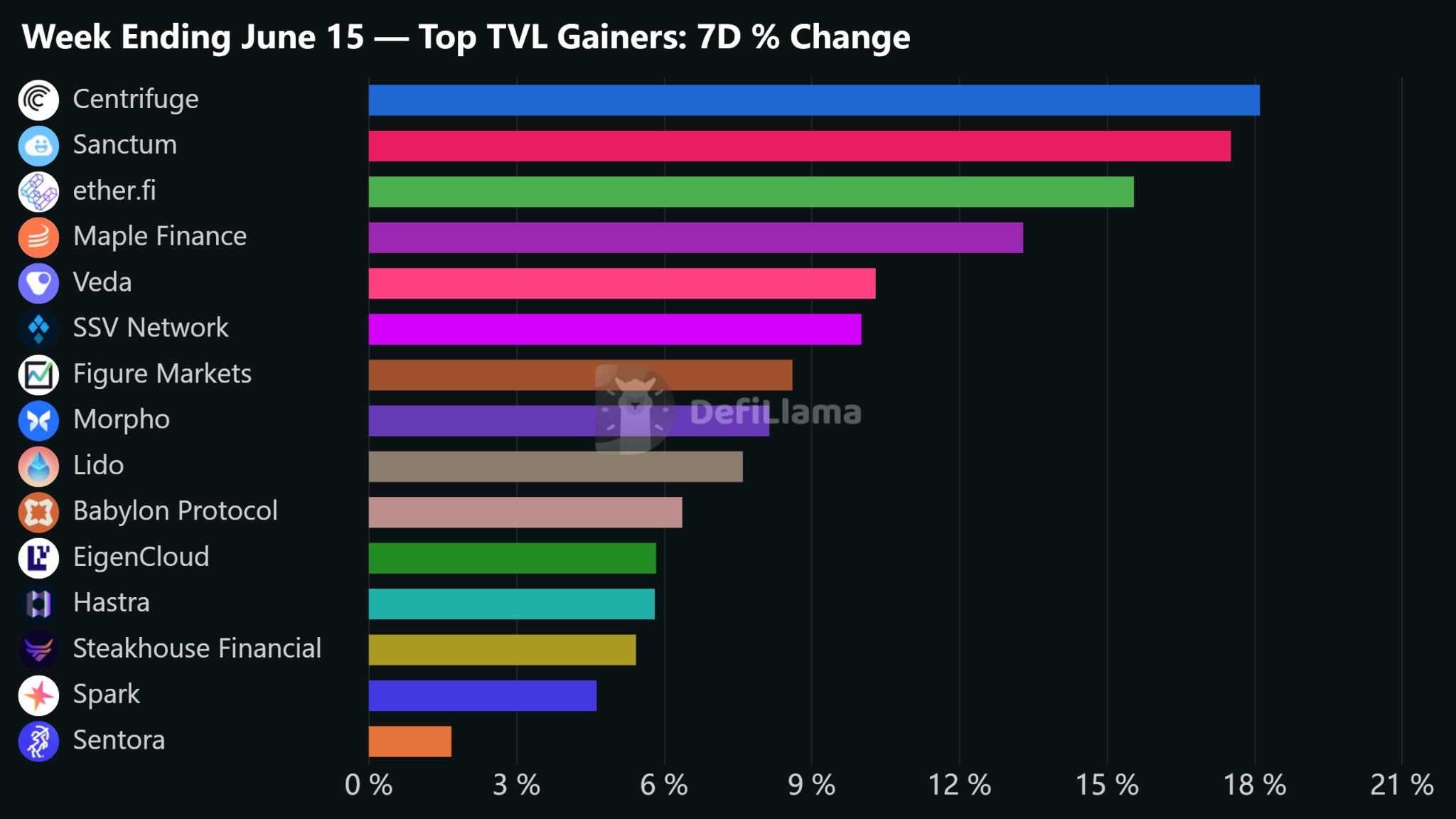

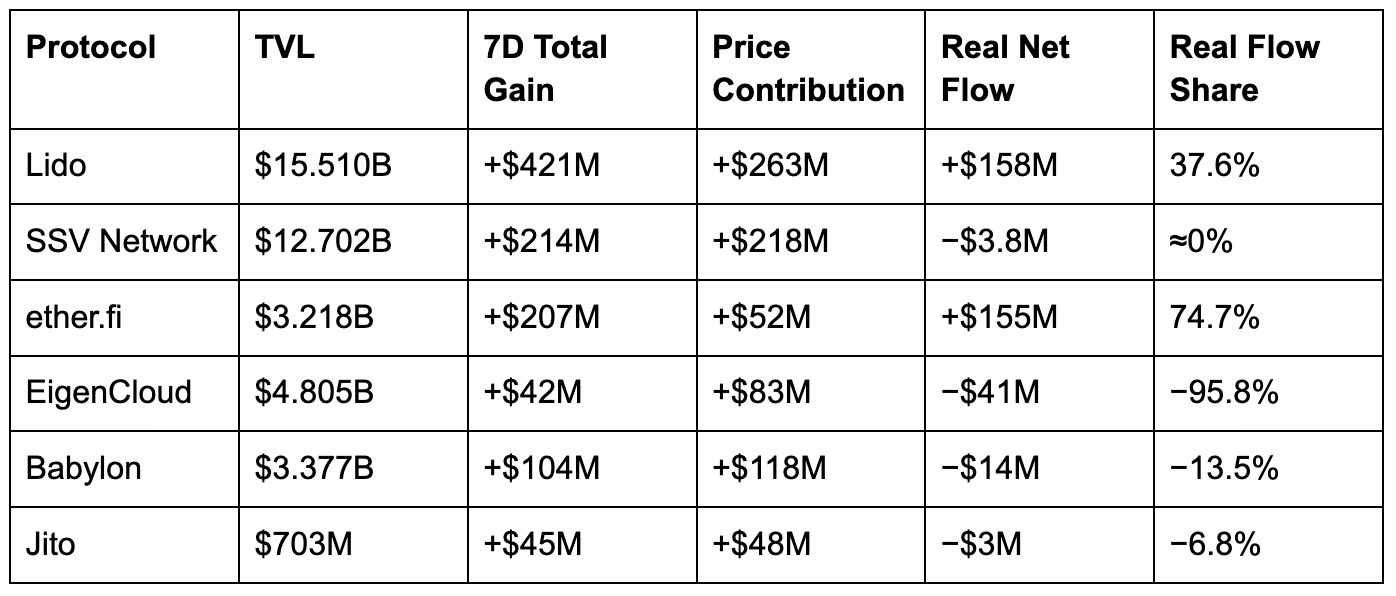

4B. TVL Gainers ($50M+ filter) — Ranked by absolute $ inflow.

1. ETH Staking & Restaking Cohort — Price Attribution Deep-Dive

This cohort’s headline story was price, not flow. ETH closed the 7-day window at $1,716, up from $1,687 — a +1.74% move. Applied to the combined $50B+ of ETH-denominated staking TVL, that modest appreciation was mechanically sufficient to generate billion-dollar nominal “gains” for Lido (+$1.056B) and SSV Network (+$1.153B), neither of which reflects real-world capital inflow.

Ether.fi — The Standout Real-Flow Story

ether.fi is the clean outlier in this cohort. Of its +$207M 7-day gain, $155M (74.7%) represents genuine new capital arriving on-chain, against just $52M attributable to ETH price appreciation. ether.fi deployed a roughly $100M RWA liquid vault in partnership with Plume Network and Midas, combining exposure to a BlackRock iShares AAA CLO ETF, a Fidelity Total Bond ETF, and a FalconX credit pool. This positions Ether.fi as a yield-bearing gateway into tokenized fixed income alongside its restaking core — a genuine product expansion that adds a non-correlated yield layer and draws institutional allocators who wouldn’t otherwise touch the restaking stack.

2. RWA Infrastructure — The Week’s Dominant Growth Theme

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.