Worst ETF Outflows Since November, Stellar Leads Chain Inflows, and many more...

Subscribe for daily free DeFi news covering launches, tradable catalysts, and actionable farming opportunities.

Find and execute the 15%+ stablecoin yields in minutes

Save time without checking every protocol manually. DeFi Saver’s Discover page surfaces rates across Aave, Morpho, Spark, and more, lets you simulate leverage before committing, and handles the full loop in one click. Stop leaving yield on the table.

<Discover Yields on DeFi Saver> | Today in DeFi is Supported by DeFi Saver

Today’s News Headlines:

- Gnosis Pay exploited via Zodiac Delay Module bug

- Apyx boosts Season 2 points to 196x

- X Layer brings tokenized stocks via xStocks

- CFTC approves first U.S. perpetual contract

- Re Protocol expands reinsurance program portfolio

- Venice cuts VVV emissions toward deflation

- Radiant Capital sunsets after failed recovery

- EdgeX investigates alleged token price manipulation

- Fluid discloses an exploit on backend reward system bug

Key Takeaways:

Regime leans risk off.

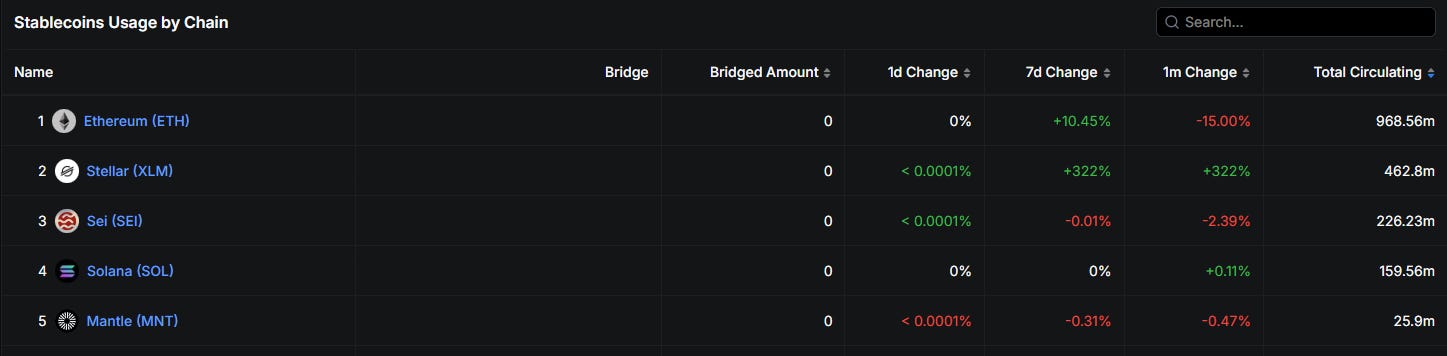

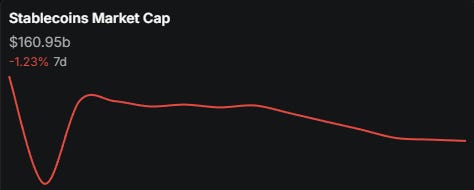

Treasuries got a bid this week, but stayed above 4%, pressing on risk. Net liquidity stalled and the BTC/NQ ratio keeps making new lows. May closed as the worst monthly BTC ETF outflow of 2026 at -$2.3B. Onchain matched it: both USDT and USDC contracted in the same week for the first time in months.

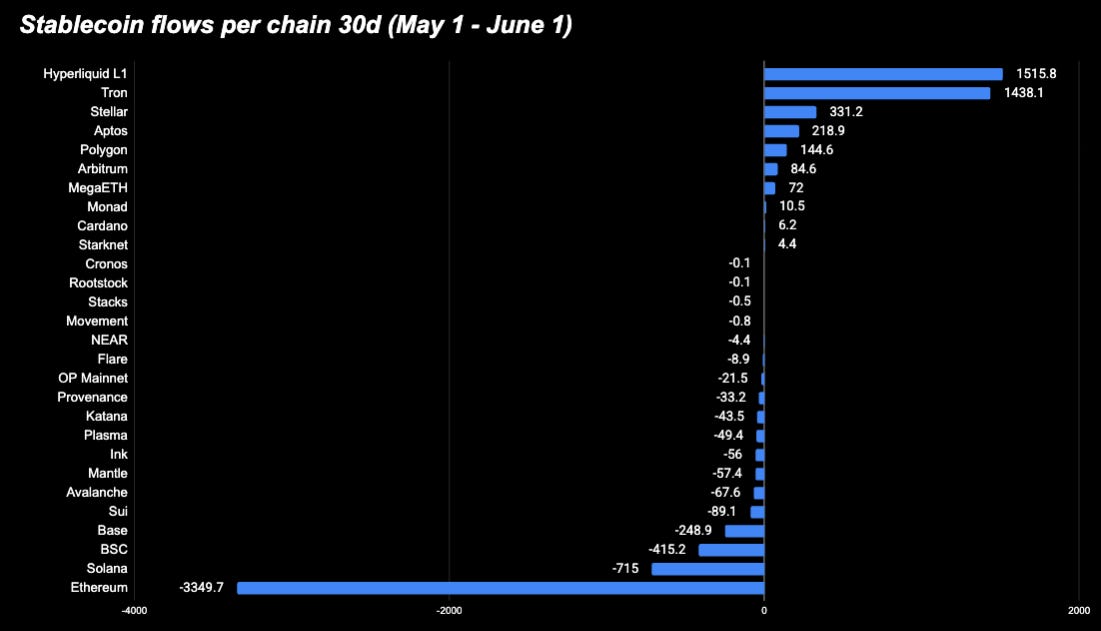

Stellar gained $319M in stablecoin inflows this week

Equivalent to an entire month of prior inflows. The driver is Ondo’s USDY, which expanded from $124M to $526M on-chain in seven days and now makes up 71% of Stellar’s stablecoin base. This sits within a broader structural build: 91% QoQ RWA growth, $2.4B in tokenized assets

Hyperliquid is still the 30d stablecoin leader (+$1.5B) even as the broad market bled. The AQAv2 USDC migration that began mid-May remains the dominant multi-week flow story, outlasting this week’s risk-off. The chain saw a small give-back on the week (-$178M), but the structural inflow trend that started with Coinbase and Circle’s USDC integration is intact.

Section 1 — Macro + Capital Backdrop

1A. Traditional Macro

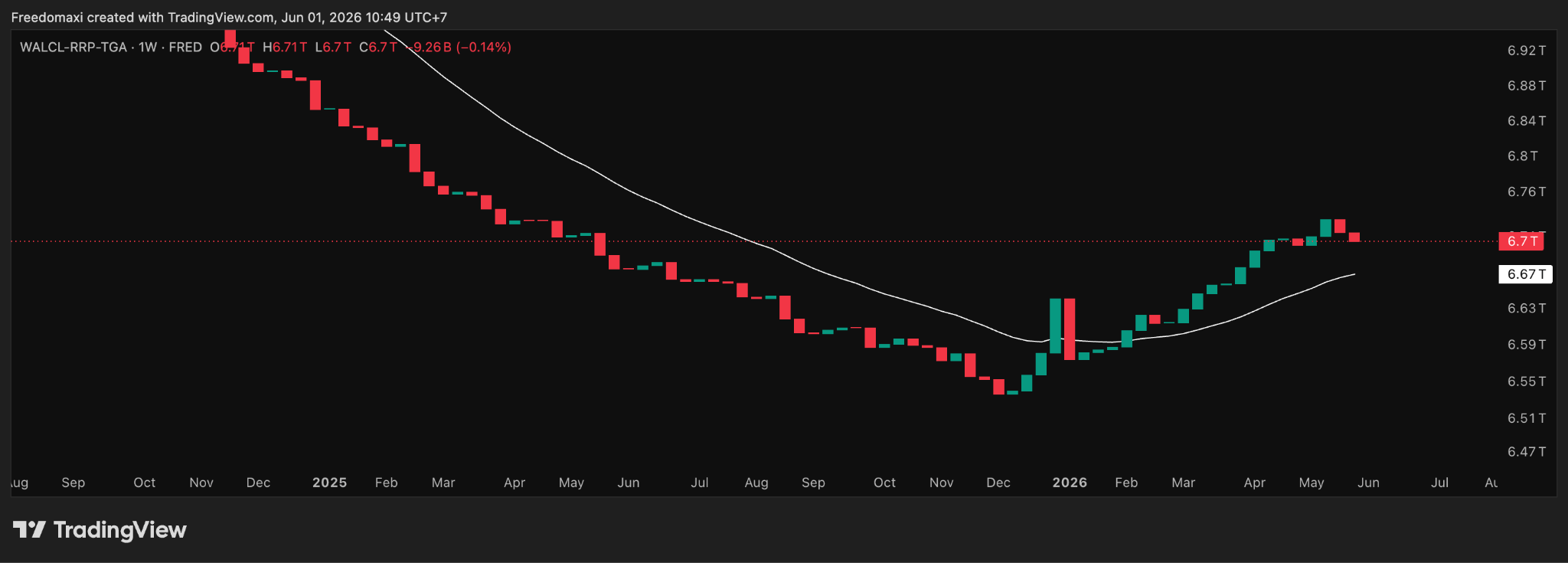

Net liquidity (WALCL-TGA-RRP)

Net liquidity (WALCL-TGA-RRP): ~$6.71T. Still above the 20W MA but contracted this week — MILD HEADWIND. The structural uptrend off the early-2026 trough remains intact, but the weekly direction turned down. Liquidity is no longer the clean tailwind it was through April.

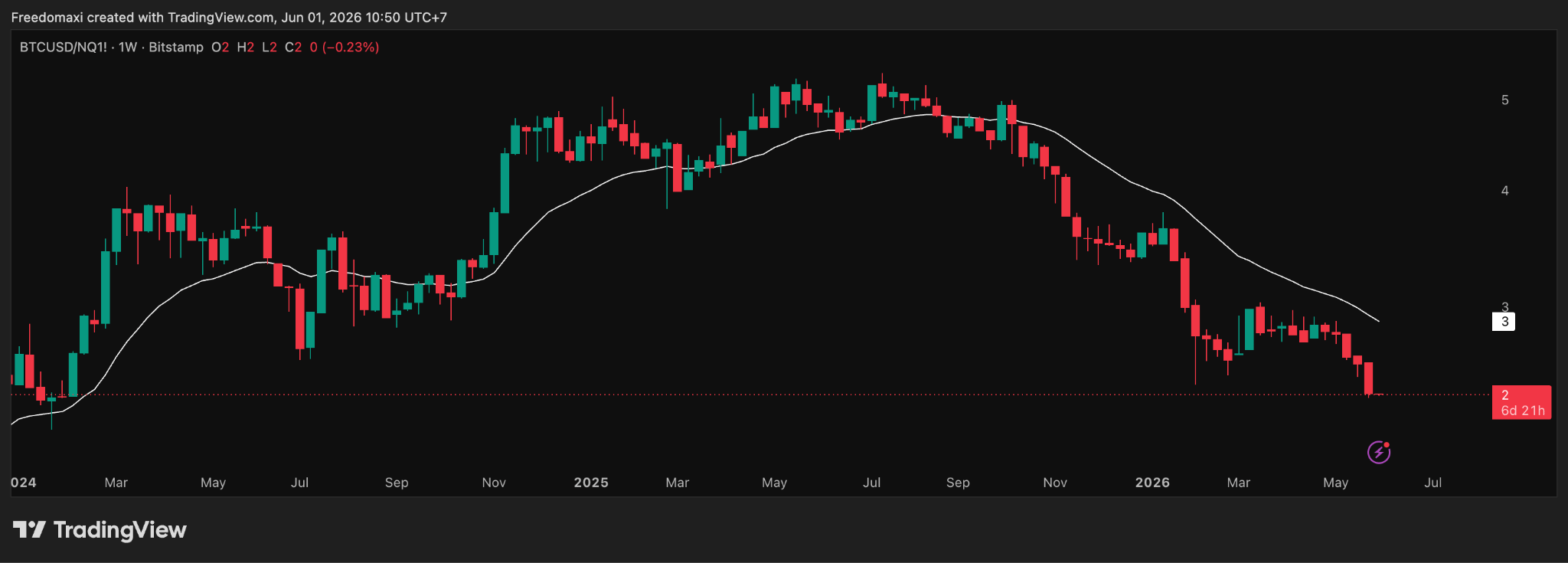

BTC/NQ ratio vs 20W MA.

BTC/NQ ratio: making new lows. Below the 20W MA and falling — HOSTILE. The ratio is at its lowest in the visible range, confirming that capital continues to favor tech equities over crypto. No sign of relief so far in the BTC-vs-equities underperformance regime that started after the October liquidation event.

The macro picture is neutral-to-hostile, not a clean hostile sweep. Treasuries got a bid this week, maybe from sight of a potential Iran war deal, but liquidity also contracted, though the long term liquidity trend seems constructive. BTC continues to underperform Equities. Macro alone isn’t actively supporting risk, and the onchain picture (Section 2) tips the combined read hostile.

1B. Crypto Capital On-Ramp

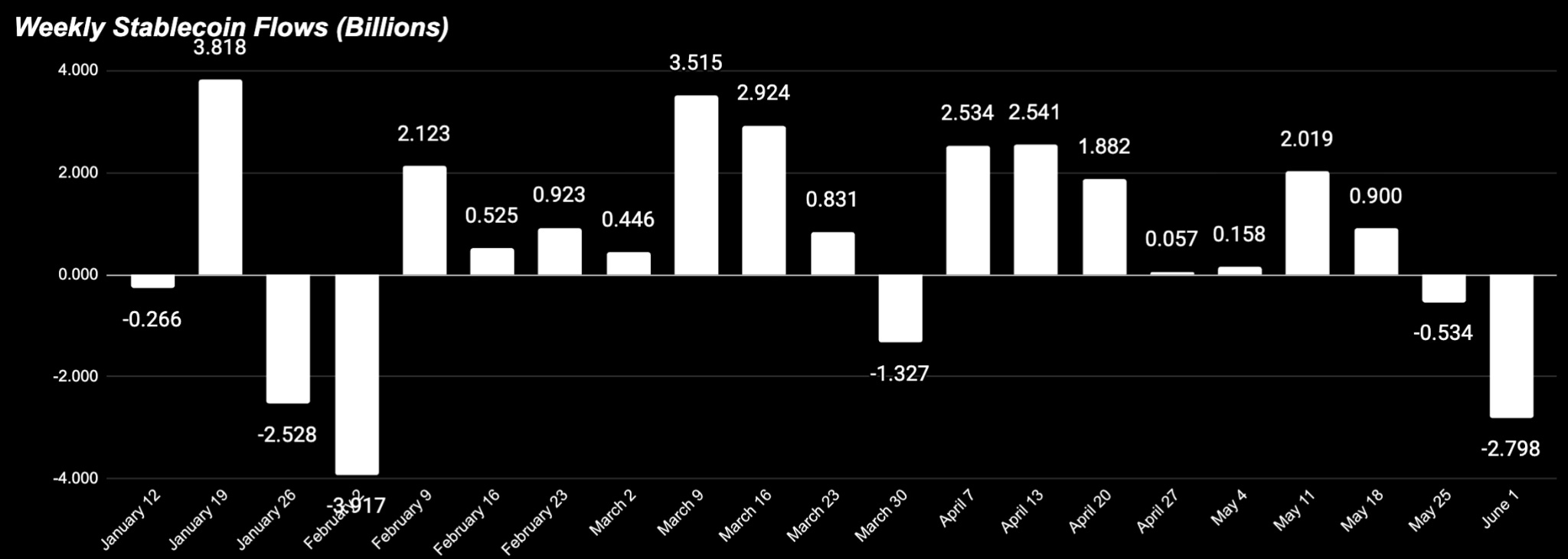

Total stablecoin supply (level + WoW)

Total stablecoin supply: -$2.798M (-0.87%). Largest weekly outflow since February. This setback is also in line with Macro liquidity (WALCL - RRP- TGA), which also contracted in the last 2 weeks.

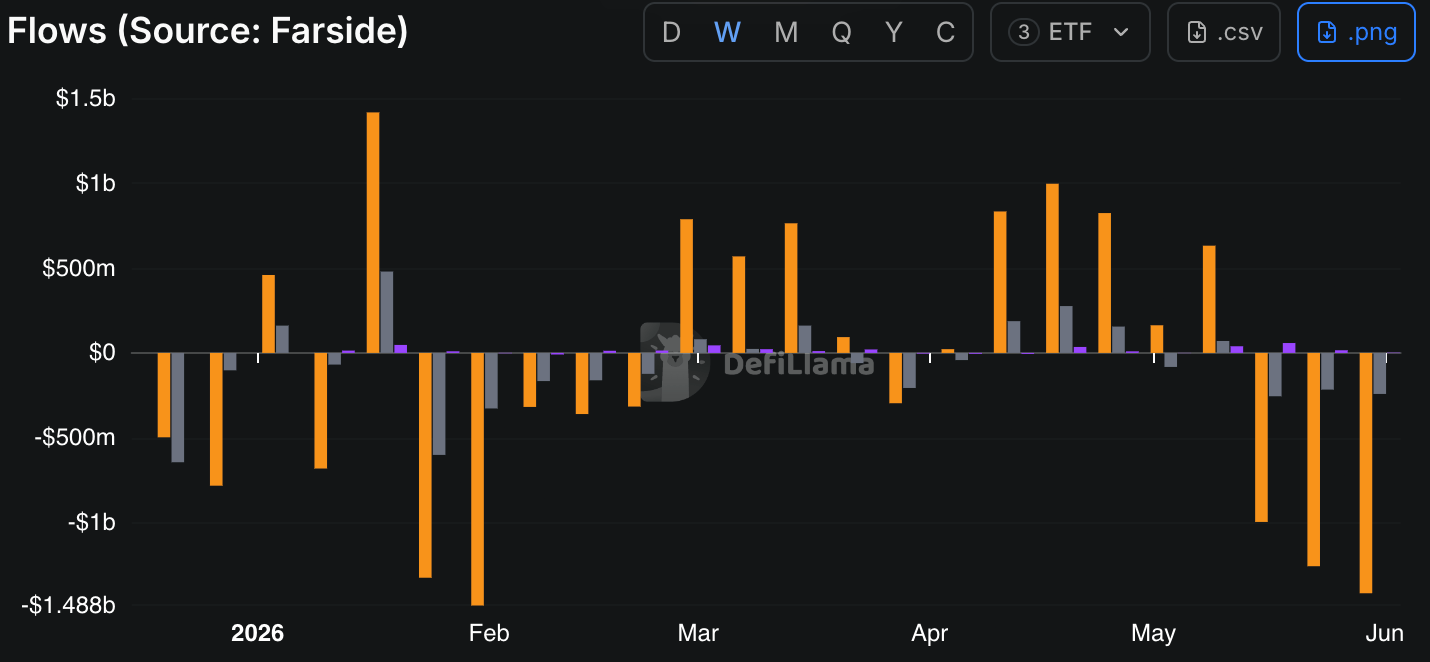

ETF flows

ETF flows: BTC -$1,416M, ETH -$241M. Third consecutive week of major institutional outflows after the May 18 PPI shock. May closed as the largest monthly Bitcoin ETF outflow of 2026 at -$2.3B — the steepest since November 2025, reversing two consecutive green months. Whales and long-term holders have also started distributing. The institutional bid that carried Q2 has clearly paused.

BTC price context: Bitcoin sits around $73,500 heading into June, pressured by the ETF outflows, geopolitical tension, and the broader risk-off in equities. As a high-beta macro asset, BTC is absorbing pressure, unlike Nasdaq which proves to be more resilient.

1C. Week-Ahead Catalysts

Source : tradingeconomics.com

Wednesday June 3 — ADP employment, ISM Services PMI

Friday June 5 — May Jobs Report (NFP), the marquee event. April surprised strongly at +115K (vs ~62K expected), unemployment held at 4.3%. Watch the unemployment rate (any move above 4.3% shifts the narrative), wage growth (hot = reignites inflation fears), and participation. This is the week’s pivot for rate expectations.

CLARITY Act — the bill cleared the Senate Banking Committee (15-9) but momentum stalled. JPMorgan’s Jamie Dimon escalated the fight on May 29, warning the banks “will not accept” stablecoin-yield provisions and that the framework could fail. A regulatory headwind to watch. Source: CoinDesk.

Verdict: Macro + capital backdrop leans hostile. While rates saw some relief and liquidity seems stabilizing, other indicators are pressing against risk this week and the institutional bid is in retreat.

Section 2 — Onchain Risk Regime

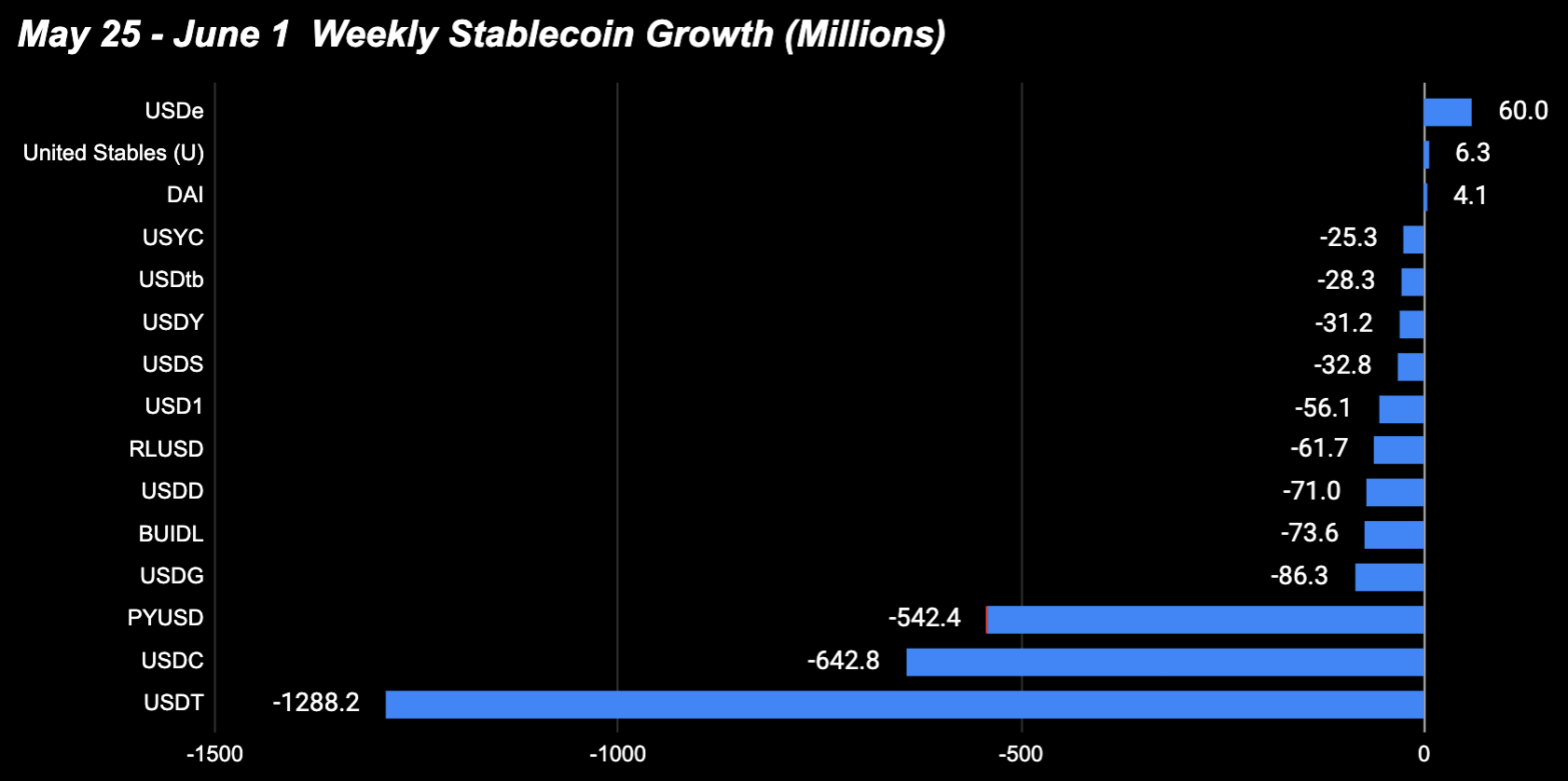

This week’s stablecoin data is the cleanest risk-off signal in months: both of the two largest stablecoins contracted hard at the same time.

Contracting (7d): USDT -$1,288M (-0.68%), USDC -$643M (-0.84%), PYUSD -$542M (-15%), USDG -$86M (-3.28%), BUIDL -$74M (-2.41%), USDD -$71M (-4.72%), RLUSD -$62M (-3.5%), USD1 -$56M (-1.17%)

Growing (7d): USDe +$60M (1.35%), United Stables +$6M, DAI +$4M

The signal: USDT (trading and parking capital) and USDC (DeFi deployment capital) leaving together is broad de-risking, not rotation. When capital rotates between venues, one of the two usually grows. Both contracting at once means money is leaving crypto, not moving within it. PYUSD’s -$542M is also unusually large for that stablecoin.

USDe was the only minor gainer +$60M (+1%) from the total supply — Ethena’s basis trade continues attracting capital even through the broad bleed, consistent with its 30d leadership (+$600M, the top stablecoin gainer over the month).

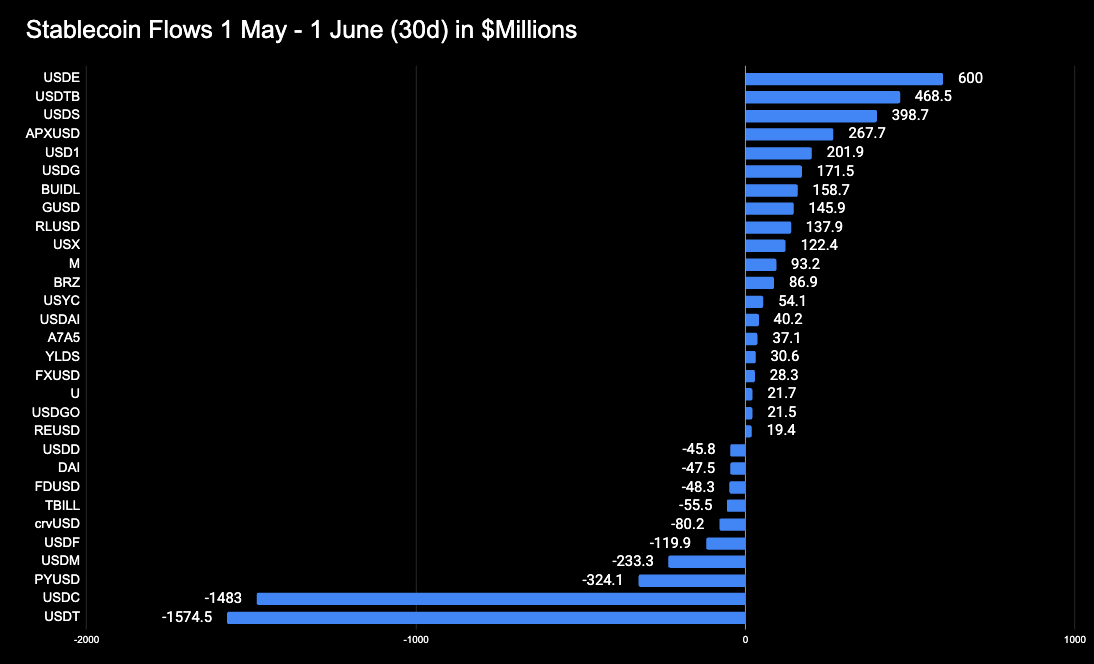

30d context confirms the weekly weakness is structural for the majors: USDT -$1,574M and USDC -$1,483M are the two biggest 30d losers. On the other side, USDe +$600M, USDtb +$468M, and USDS +$399M led — yield-bearing and RWA-backed dollars held up while transactional dollars bled.

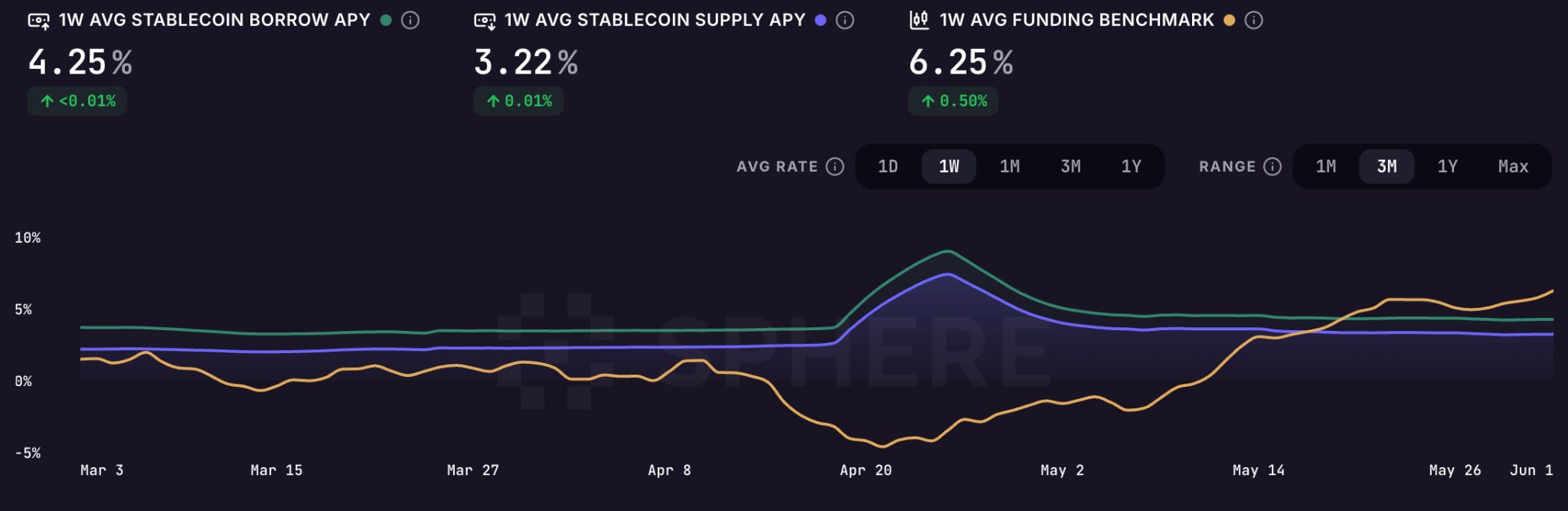

Aave / Sphere Rates — CALM, FUNDING RISING

Borrow APY 4.25% (+0.01%)

Supply APY 3.22% (+0.01%)

Funding benchmark 6.25% (+0.50%).

Lending rates flat — no forced unwind pressure in spot markets. The notable move is funding rising +0.50% to 6.25%, meaning leveraged longs are increasingly dominant. Source: Sphere.

Stablecoin borrow rates measure demand for capital, while funding rates measure trader sentiment. When funding falls far below borrow rates, traders are extremely bearish but capital demand remains strong—meaning people are still borrowing and deploying money despite the fear. That’s often a sign of a bottom and a potential buying opportunity.

Conversely, when funding rises far above borrow rates, traders are aggressively chasing long exposure and paying high carry to do so, which often signals excessive optimism and increases the risk of a market top.

Large negative spread (Funding < Borrow Rate)= fear/opportunity

Llarge positive spread (Funding > Borrow Rate) = greed/caution.

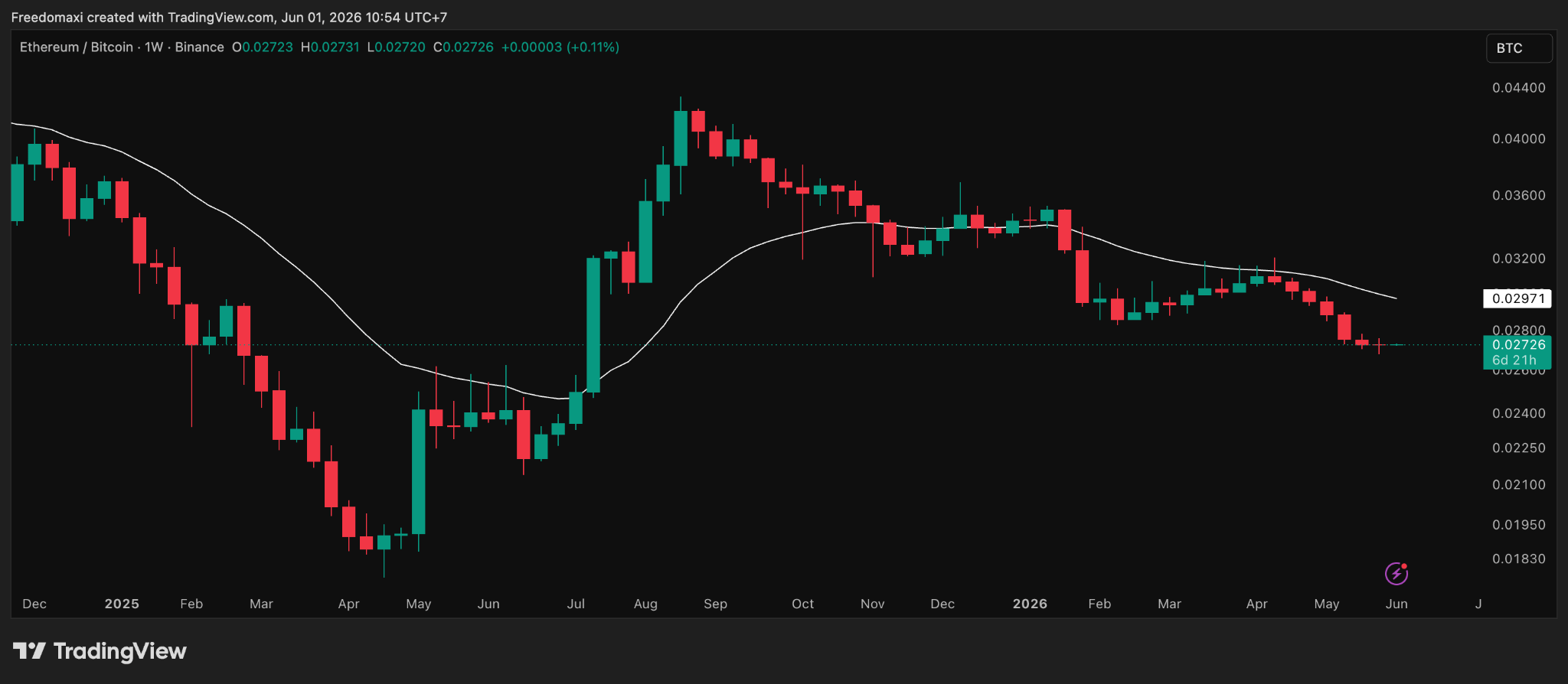

ETHBTC vs 20W MA

ETHBTC at ~0.02726, below the 20W MA (~0.02971) and showing no signs of recovery. ETH continues to underperform BTC with no reversal in sight — bad for ETH specifically and most altcoins broadly. No signal to overweight ETH within the crypto sleeve.

Verdict: Onchain regime RISK-OFF. Both major stablecoins contracting, transactional capital leaving crypto, leveraged longs building into a weakening spot market, ETH still bleeding against BTC. Capital is defensive and the leverage/spot divergence is the risk to watch.

Section 3 — Chain Comparison

Stellar — The Ondo USDY Deployment Wave

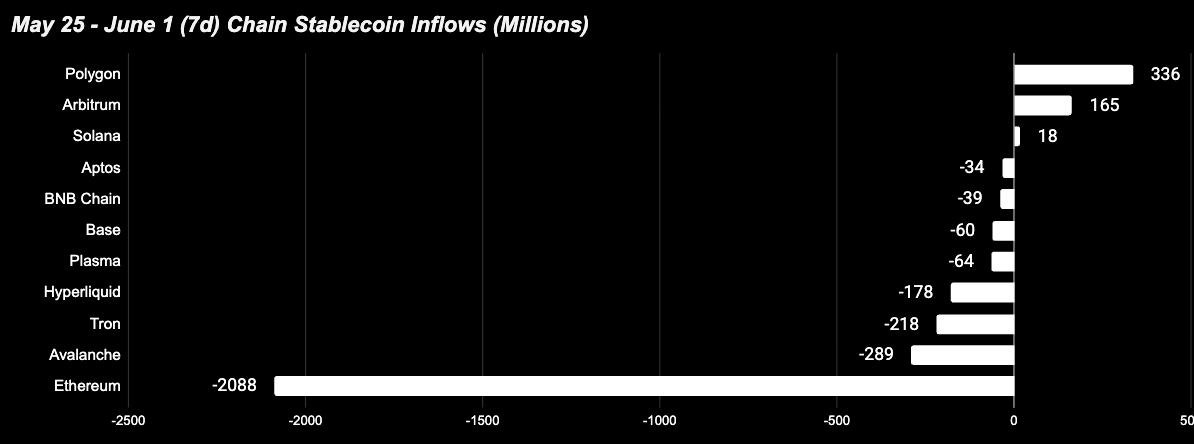

Stellar absorbed +$318.5M in stablecoin supply this week, a +75.2% gain that frames as even more significant in 30-day context: the week’s inflow of $318.5M is nearly equivalent to the entire prior month’s accumulation of $334.9M. The same volume that took four weeks to build arrived in one.

Supply composition resolves the story precisely. USDY — Ondo Finance’s tokenized short-term Treasury note — expanded from $124.1M to $525.7M, a +$401.6M inflow in seven days. Simultaneously, USDC contracted by $83.6M on Stellar over the same period. The net headline of +$318.5M therefore understates the USDY surge: USDY grew by $401.6M while USDC drained, with USDY now representing 70.8% of Stellar’s $742M stablecoin base.

This is not retail demand or DeFi incentive farming. It is a systematic institutional yield product deployment, targeting Stellar’s payment and remittance corridors for emerging market access. Ondo’s growth on Stellar reflects a broader strategic expansion of tokenized Treasury products beyond Ethereum-native DeFi venues into payment-optimized infrastructure chains.

Polygon — USDC Acceleration on Payment Rails

Polygon added +$336.2M this week (+9.9% 7d), pushing total stablecoin supply to $3.72B. The 30-day accumulation context is notable: the prior full month added $142.3M. The week’s inflow of $336.2M is 2.4× the monthly figure — this is acceleration, not steady-state growth.

The token-level composition is unambiguous. USDC drove +$360M (+21.3%) of the $336.2M net gain, bringing its balance on Polygon to $2.05B and accounting for 55% of total chain supply. USDT was effsectively flat (+$1.9M). This is a single-asset, single-use-case story: USDC on Polygon, driven by payment settlement infrastructure.

Polygon has established itself as the dominant chain for real-world USDC payments, with Visa’s global stablecoin settlement program, Revolut, Tazapay, Stripe, and Meta’s LATAM creator payment infrastructure all routing USDC through the network. The April addition of private USDC/USDT transfers with KYT compliance checks deepened enterprise adoption. The week’s acceleration above the 30d trend is consistent with institutional payment volume scaling rather than a single event catalyst.

Arbitrum — The Healthiest Composition in the Cohort

Arbitrum gained +$165.8M (+4.1% 7d), consistent with its 30-day trend of +3.0% (+$121.1M). The pace is steady, not spiking — and at $4.20B, Arbitrum holds the second-largest L2 stablecoin base.

What distinguishes this week’s Arbitrum entry is not the percentage, but the composition. Total token-level gains across the chain were $166.1M, against total outflows of just $0.3M — near-zero counterflow across all tokens. USDC led at +$134.7M (+6.0%) to $2.37B; USDT contributed +$15.4M (+1.6%). No single token dominated negatively. Every tracked stablecoin either grew or held flat. This is the cleanest accumulation profile in the entire qualifying cohort.

The demand base is maturing. Arbitrum’s stablecoin holder count is approaching ten million, up 28% in three months per network data, with $50B+ in monthly transfer volume. Recent infrastructure additions include Oobit’s integration enabling Arbitrum stablecoin spending at Visa-accepting merchants globally, and Morpho USDC vaults launching natively in the Arbitrum Portal — compounding the DeFi yield and real-world payments flywheels simultaneously.

Sui — A Network Shock Accelerates a Pre-Existing Drain

Sui shed $125.8M in stablecoin supply this week (−21.0%), but the 30-day context is essential: the chain was already down −15.8% (−$89.2M) over the prior month. The 7-day figure is an acceleration, not an initiation.

The proximate catalyst is clear. Sui suffered a 5-hour, 55-minute network outage on May 30, triggered by a consensus bug in the v1.72 software release — the second significant downtime event the chain has experienced in 2026. The on-chain impact was immediate: $1.2M in total token-level gains against $126.9M in total losses, representing near-zero countervailing inflows across all stablecoins. Capital did not wait for the post-mortem.

The outage, however, is an accelerant rather than the root cause. Sui’s stablecoin drain predates the May 30 event by weeks. A broader context applies: TVL compression from a ~$2B peak to a ~$500M current base has repriced the DeFi ecosystem’s depth, reducing the incentive for stablecoin capital to remain idle on-chain. USDsui, the chain’s native yield-bearing stablecoin, has grown to approximately $75M in circulating supply since its launch — meaningful traction — but at current share it is insufficient to offset continued USDC and USDT outflows.

Two production outages from release-level bugs in a single calendar year represent a systemic reliability pattern. Until the v1.72 post-mortem demonstrates the vulnerability class has been resolved, stablecoin reaccumulation on Sui remains conditional.

Ethereum — The Persistent Structural Donor

Ethereum shed $1.94B in stablecoin supply this week (−1.2%), extending a consistent 30-day outflow trend of −2.0% (−$3.27B). At the 30-day run rate, the chain is losing approximately $754M in stablecoin supply per week. The direction is uniform and shows no sign of reversal.

Token-level decomposition reveals $624.9M in total gains across various tokens, overwhelmed by $2.56B in total losses concentrated in the two dominant assets: USDT declined $1.14B and USDC fell $316.5M. The destinations are identifiable. Polygon continues absorbing USDC into payment settlement infrastructure. Arbitrum draws both USDC and USDT for DeFi depth. Hyperliquid’s $6.27B USDC base, built almost entirely over the past 30 days, represents one of the most significant single-chain capital migrations of the year.

At $162.3B, Ethereum’s stablecoin base provides a long runway — weekly outflows of ~$754M represent less than 0.5% of total supply. This is not a liquidity crisis. But the 30-day trajectory is one-directional, and it raises the defining structural question of the current cycle: Ethereum’s DeFi protocols continue to generate dominant application-layer revenue — the highest of any chain — while the stablecoin supply that funds that activity migrates elsewhere. The chain is transitioning from the venue where stablecoins live to the settlement layer where DeFi revenues are generated on a steadily eroding supply base.

3B. Structural Shifts

Base Flips Ethereum — With a Precise Asterisk

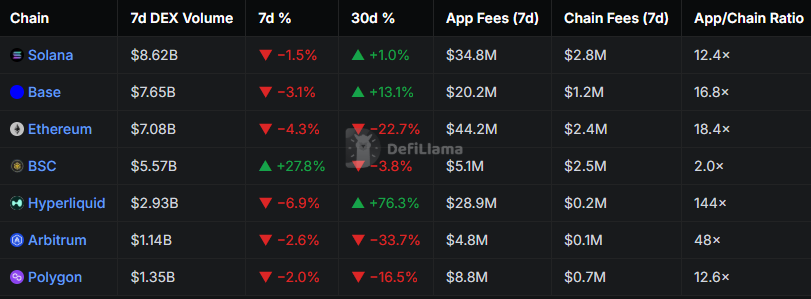

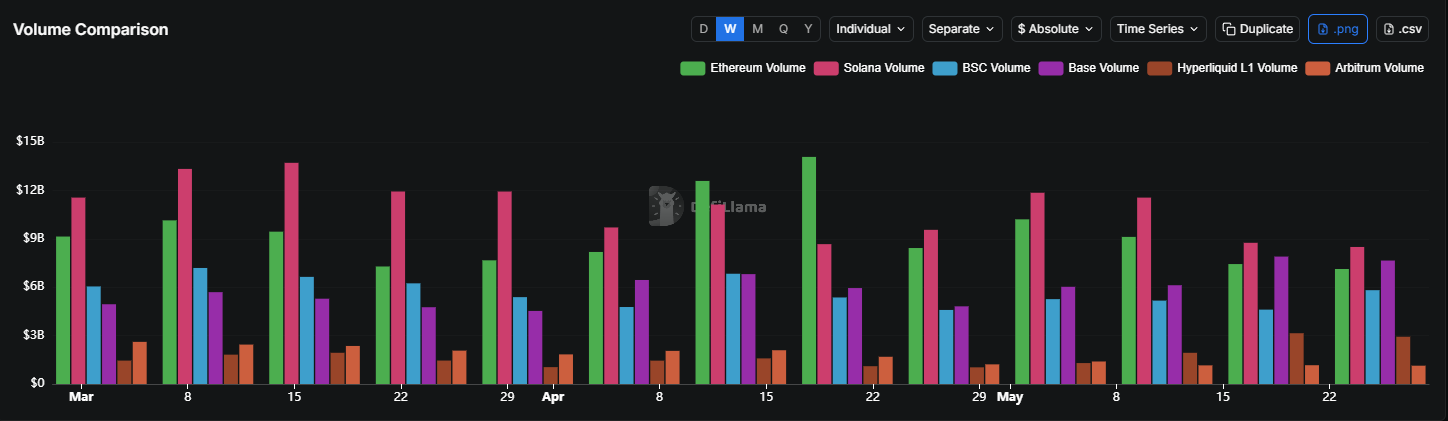

Base recorded $7.65B in 7-day DEX volume, surpassing Ethereum’s $7.08B by a $574M margin (+8.1%). Solana remains the #1 DEX chain at $8.62B — Base has taken second place for the 2 consecutive weeks. The Solana comparison is the next structural milestone, not yet achieved.

The 30-day picture still shows Ethereum ahead: $34.98B versus Base’s $28.54B, a $6.44B gap in Ethereum’s favour. What makes the weekly flip meaningful is not the absolute position but the trajectory divergence: Base’s 30-day volume grew +13.07% while Ethereum’s fell −22.69% — a 35.8 percentage-point spread over a single month. If the 30-day trajectories hold, Ethereum’s lead in the monthly figure closes within the next six to eight weeks.

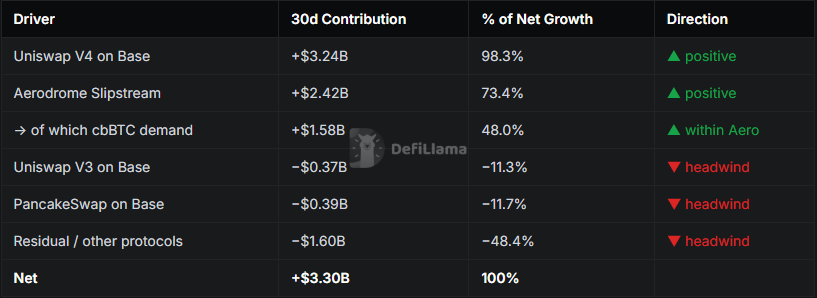

Uniswap V4 is the single largest driver of Base DEX Volume Growth. Its +$3.24B absolute 30d contribution nearly equals Base’s entire net volume growth of $3.30B. Without V4, Aerodrome’s +$2.42B gain would have been almost entirely consumed by V3 and PancakeSwap declines, leaving Base roughly flat on the month. V4 is not just the fastest-growing protocol on Base — it is structurally responsible for whether Base grows at all in the current window.

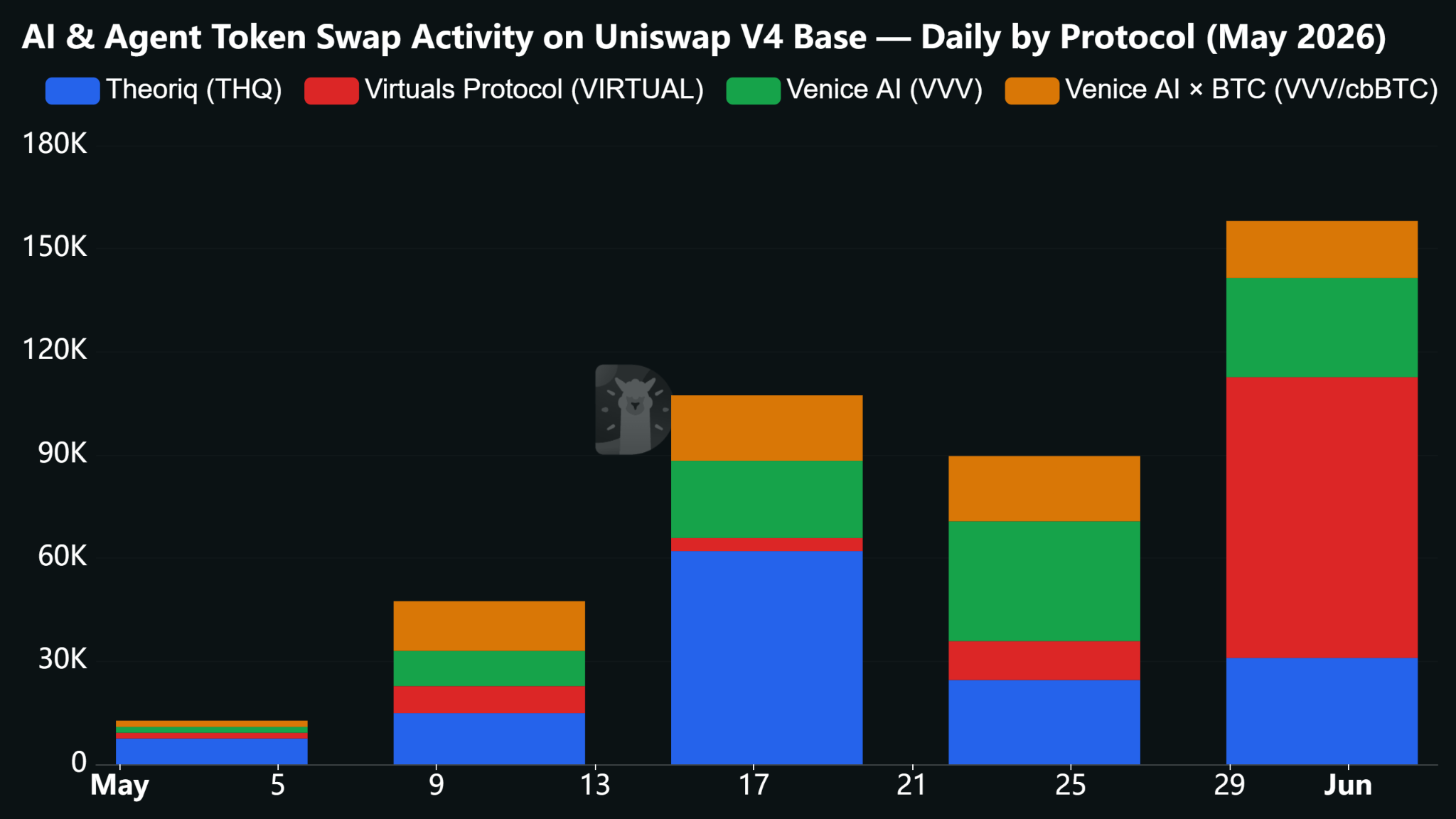

On Uniswap V4, AI and agent tokens are the real driver. VIRTUAL, VVV, THQ, and VVV/cbBTC together generate a significant volume out of total V4 activity. These projects made a deliberate choice to deploy on V4 rather than Aerodrome. The reason is visible in the data: ETH/VIRTUAL uses V4 hooks, meaning the Virtuals Protocol has embedded custom pool logic into its liquidity design. This is impossible on Aerodrome’s ve(3,3) AMM or Uniswap V3’s static pool model. V4 is attracting the most technically sophisticated new projects on Base precisely because hooks let them build trading mechanics that don’t exist elsewhere.

Aerodrome Slipstream is the volume floor, not the growth engine. At +$2.42B, it contributes strongly to growth in absolute terms but its +18.98% 30d growth rate is a large-base, steady-compounding story rather than an acceleration. cbBTC demand (~65.3% of Aerodrome Slipstream’s swap count, implying ~$1.58B of Aerodrome’s growth) is the activity catalyst inside the Slipstream infrastructure — but it expresses through Aerodrome rather than driving independent incremental volume.

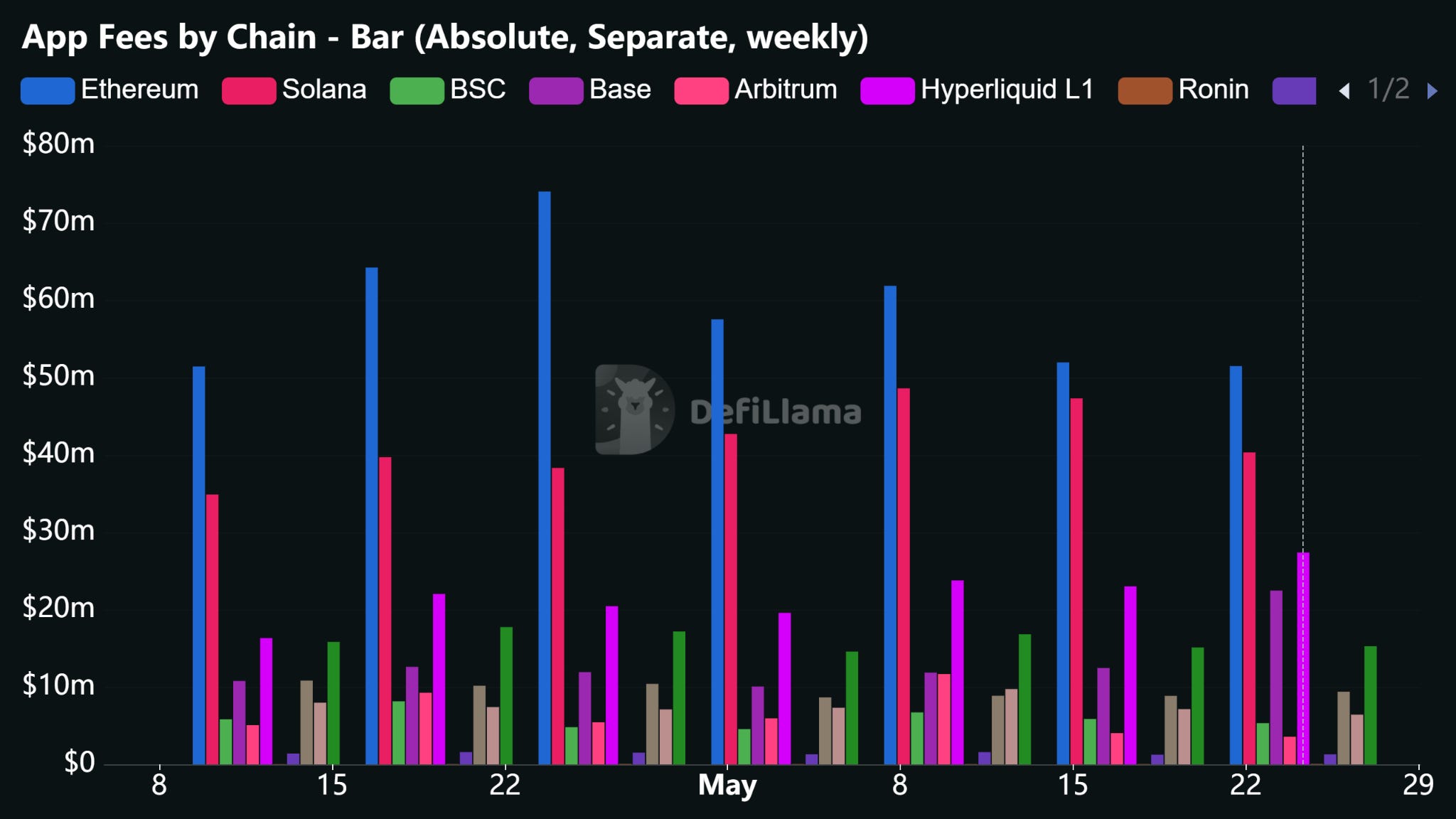

The fee economics adds a second dimension. Base generates $20.2M in application-layer fees on $7.65B of volume — a fee yield of $2.64 per $1,000 transacted. Ethereum generates $44.2M on $7.08B — $6.24 per $1,000. Ethereum still monetises its DEX volume at 2.4× the rate of Base. This reflects a structural mix difference: Ethereum’s remaining DEX activity is skewed toward larger, less price-sensitive trades where Uniswap V4’s higher fee tiers dominate; Base’s volume is skewed toward higher-frequency, lower-margin flows through Aerodrome’s aggressive fee competition.

BSC — Five Products in Seven Days

BSC’s +27.75% 7-day volume spike to $5.57B is the week’s most straightforward catalyst story once the Binance activity calendar is mapped to the daily volume data. The 30-day figure of −3.79% is the essential context: BSC was in a negative trend before this week. This is a campaign-driven intervention, not an organic reversal.

May 27: Binance Wallet DeFi Platform launches — a unified interface embedding 40+ protocols and 1,000+ yield pools for earn products, lending, and LP positions natively inside the Binance app

May 28: Binance DeFi Earn Week begins — a 60-day campaign through July 27 distributing $1.1M in rewards across USDT, USDS, and USD1 in featured BSC protocols; Venus Flux integrates directly into Binance Wallet on the same day

PancakeSwap Infinity’s CLMM pools become accessible via Maestro Telegram bots, reported to have driven $250M+ in daily BNB Chain volume

Average daily volume May 2–24: $681.1M. Average daily volume May 25–31: $795.6M — a +16.8% step-up that held through the week’s final days at $933M and $936M respectively. The acceleration is real and corroborated by application fees (+9.88% 7d).

Hyperliquid — The Fee-Efficient Outlier

Hyperliquid generated $2.93B in 7-day DEX volume (−6.9% 7d, +76.3% 30d) and $28.9M in application-layer fees — a 144× application-to-chain-fee ratio. It is the defining structural characteristic of Hyperliquid’s CLOB architecture. The $0.2M in L1 chain fees is near-zero by design; all economic value is captured at the application layer and distributed to HYPE stakers and the protocol’s assistance fund.

The fee yield differential makes Hyperliquid’s competitive position explicit. At $28.9M in fees on $2.93B of volume, Hyperliquid generates $9.86 per $1,000 transacted — 1.58× Ethereum’s $6.24 per $1,000 and 3.74× Base’s $2.64 per $1,000. Hyperliquid is the highest fee-yield DEX ecosystem in the qualifying cohort by a substantial margin. The structural explanation is that perpetual futures — Hyperliquid’s core product — carry a materially higher fee yield than spot DEX trades: taker fees, funding rate accrual, and liquidation proceeds all compound on notional exposure in ways that spot AMM swaps do not.

The +76.3% 30-day volume growth is partly a function of the AQAv2 USDC capital deepening — a larger, deeper USDC collateral base structurally supports higher open interest and therefore higher notional volume — and partly a reflection of genuine perp market share migration from centralised exchanges.

Arbitrum — The Stablecoin-Volume Divergence

Arbitrum’s 30-day DEX volume decline of −33.7% is the deepest in the cohort — and it sits in direct structural tension with Arbitrum’s stablecoin supply growth of +4.1% (7d) and +3.0% (30d) documented in Section 3A. Capital is accumulating in stablecoin form while trading activity compresses.

It’s likely due to use-case bifurcation: the capital accumulating on Arbitrum is in yield-bearing or payments-oriented positions — Morpho USDC vaults, Oobit payment rails — that do not generate DEX swap events. Under this reading, Arbitrum is absorbing stablecoin depth that enters productive DeFi positions rather than active trading liquidity.

Arbitrum’s application fees grew +36.3% 7d — the strongest 7-day fee growth of any chain in the cohort — despite volumes declining. A smaller number of higher-value transactions generating more revenue per swap is precisely what remains when high-frequency retail flow migrates out and institutional or protocol-level activity stays. The implication for Arbitrum’s medium-term positioning: it is becoming a yield and payments settlement layer rather than a high-frequency trading chain, which may be a rational specialisation in an ecosystem where Base has captured the retail DEX mandate.

Section 4 — Project & Protocol Discovery

4A. Token Price Movers - Observations, not trade ideas.

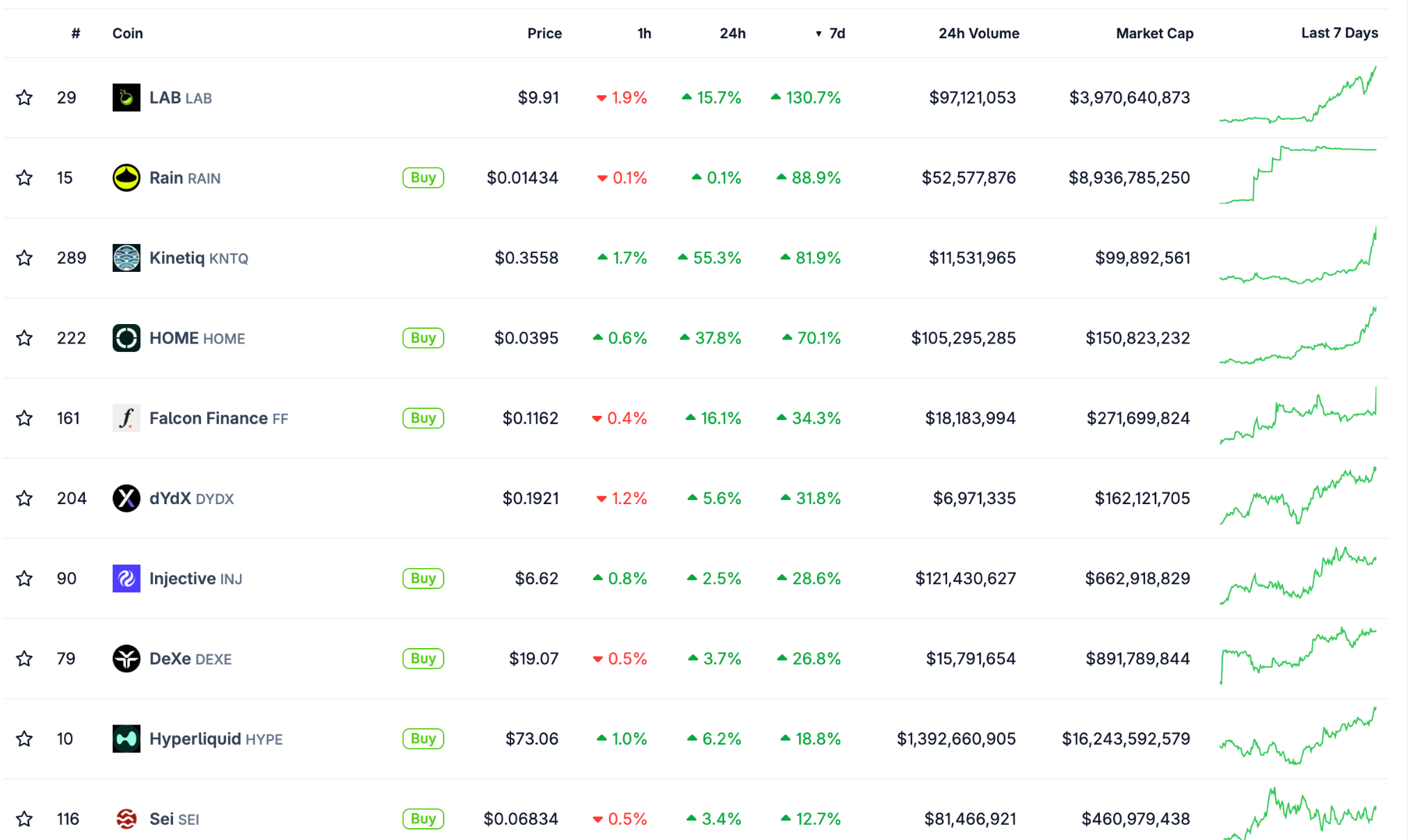

$KNTQ (Kinetiq) — the standout catalyst stack on Hyperliquid this week. Kinetiq is the leading liquid staking protocol on Hyperliquid (kHYPE), and it flipped Binance Staked SOL to become the 5th-largest liquid staking protocol overall per DefiLlama. Three reinforcing catalysts: a Kraken listing announcement for KNTQ (May 22), the launch of Treehouse’s tHYPE (fixed-income infrastructure powered by Kinetiq), and the broader Hyperliquid ecosystem tailwind including HIP-4 CPI outcome markets approaching mainnet and the 2026 FIFA World Cup coming to Hyperliquid. KNTQ’s tokenomics (burns and buybacks) tie protocol growth to token value. Sources: Kinetiq X, Kraken X.

$FF (Falcon Finance) — Falcon launched fUSD on May 27, a GENIUS-ready stablecoin with a rewards structure. The pitch addresses a real structural gap: ~$320B of stablecoins are in circulation, the reserves backing them earn billions in yield each year, but most of that income flows to issuers rather than holders. fUSD targets ~3%/yr rewards for qualifying institutional holders, with Anchorage as the federally regulated issuer (built for the GENIUS framework) and Falcon committing its own balance sheet from day one. A direct play on the post-GENIUS regulated-stablecoin landscape. Source: Falcon Finance X.

$SEI (Sei) — Sei published the Giga Roadmap on May 28, its first public roadmap of the milestones leading to the Giga Upgrade. The upgrade is a major performance overhaul for the network. The roadmap gives the market a concrete timeline to track, which is the kind of forward visibility that tends to support sentiment in a quiet tape. Source: Sei X.

On Hyperliquid (HYPE):

The CEO of Intercontinental Exchange (ICE) — the company behind the New York Stock Exchange — publicly called Hyperliquid “bigger than Nasdaq” at a Bernstein conference last week, citing its daily trading volume rather than market cap. ICE confirmed it has met with Hyperliquid’s founders multiple times, a signal that legacy financial institutions are taking the platform seriously rather than dismissing it as a fringe crypto project.

JPMorgan analysts have separately flagged Hyperliquid’s growing use by non-crypto traders for off-hours oil exposure, particularly on weekends when traditional energy markets are closed.

Both institutions arriving at the same observation independently adds credibility to the platform’s real-world traction.

No specific new catalyst this week — the rally is the continuation of sentiment from the prior two weeks’ stack (BHYP ETF, AQAv2, a16z accumulation).

4B. TVL Gainers ($50M+ filter) — Ranked by absolute $ inflow.

Keep reading with a 7-day free trial

Subscribe to Today in DeFi to keep reading this post and get 7 days of free access to the full post archives.